Why Financial Privacy Matters for Wealthy Families

Key Takeaways

- Irrevocable trusts create true financial privacy by removing assets from your personal estate, keeping wealth details off public records that creditors and the IRS can access.

- Revocable trusts offer flexibility but provide zero asset protection—they remain part of your taxable estate and appear in probate records available to anyone.

- Court-tested irrevocable trust structures have successfully defended high-net-worth families from six-figure judgments and creditor claims that would have liquidated unprotected assets.

- The Ultra Trust system combines irrevocable planning with independent trustee oversight and IRS-compliant wealth strategies to shield assets while maintaining family control through advisory roles.

- Choosing the right trust structure now determines whether your legacy remains private, protected, and intact—or becomes public litigation fodder.

Last Updated: January 2026

Your wealth attracts attention. Lawsuits, tax audits, creditor claims, and even curious neighbors can gain access to your financial details through public records if your assets sit in your personal name or inside revocable structures. For high-net-worth families, financial privacy is not about hiding money—it’s about legal protection, strategic tax positioning, and control.

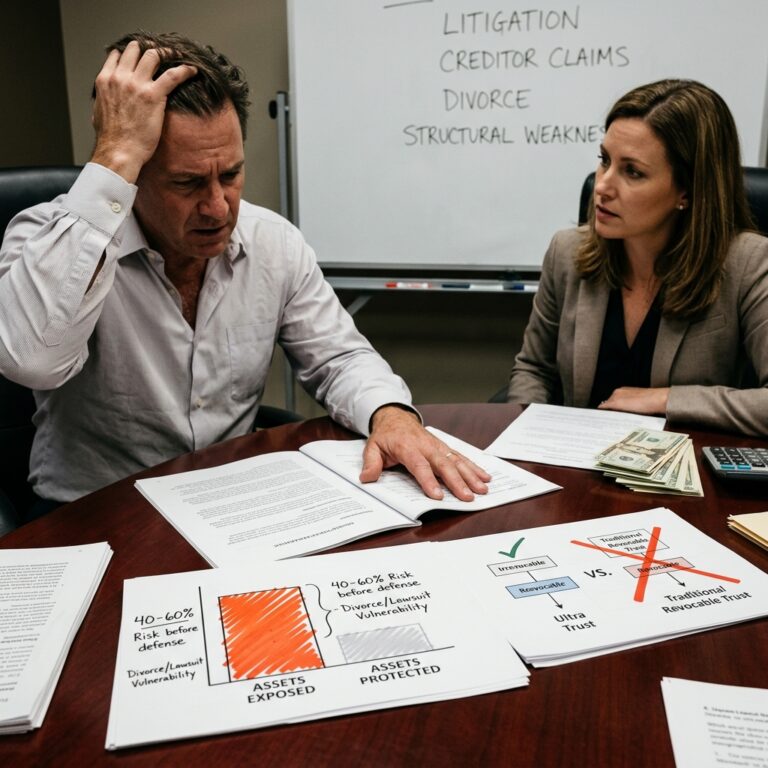

When assets remain exposed, three things happen: creditors can identify targets during litigation, the IRS can trace income sources and investment patterns for audit purposes, and family financial details become public record during probate. Each exposure point represents a vulnerability. We’ve guided families through situations where a single lawsuit against a business owner threatened to liquidate personal assets because those assets had no legal separation from business liability. The cost to recover from poor trust structure choices often exceeds the cost of setting up proper protection upfront.

Financial privacy also means your family’s wealth transfer strategy remains confidential. Probate proceedings expose estate valuations, beneficiary names, and inheritance distribution details to public court records. Revocable trusts avoid probate but still leave assets unprotected from creditors during your lifetime. Irrevocable trusts accomplish both: they keep wealth off the public radar while creating a legal barrier creditors cannot penetrate.

FAQ: What is the difference between financial privacy and asset protection?

Financial privacy refers specifically to keeping wealth details confidential—preventing creditors, tax authorities, and the public from accessing information about your assets, income sources, and estate structure through public records or discovery processes. Asset protection is the legal mechanism that prevents creditors from seizing those assets even if they know they exist. They work together: irrevocable trusts provide both. A revocable trust offers privacy in the form of avoiding probate, but it provides zero asset protection because the assets remain legally yours. With our Irrevocable vs Revocable Trusts comparison, you’ll see that true privacy requires the irreversible commitment that only an irrevocable structure delivers.

FAQ: Why do wealthy families specifically need financial privacy?

Wealthy families become litigation targets. A single major lawsuit—medical malpractice, business dispute, vehicle accident—can trigger discovery processes that expose your entire financial picture. Once a plaintiff’s attorney knows the extent of your assets, settlement demands increase. Financial privacy prevents that information leak from happening in the first place. Additionally, high-net-worth individuals face disproportionate IRS audit rates. Keeping investment strategies, income sourcing, and asset locations private through irrevocable trust structures reduces the audit surface area and gives you defensible positioning if you are selected for examination.

The Critical Privacy Difference Between Trust Types

The privacy difference between revocable and irrevocable trusts is absolute, not incremental. A revocable trust keeps your affairs out of probate court but leaves everything exposed to creditors during your lifetime. An irrevocable trust removes assets from your personal ownership entirely, creating a legal separation that creditors cannot cross.

Here’s the functional distinction: With a revocable trust, you retain the power to modify, revoke, or access the trust assets whenever you choose. That power means the assets are legally considered part of your estate. Creditors know this. The IRS knows this. During probate, your family still faces public disclosure because revocable trusts become part of your probate estate for legal purposes in many jurisdictions.

An irrevocable trust is different. Once established, you cannot unwind it, change beneficiaries, or access principal without the agreement of an independent trustee. That irreversibility is what creates privacy. Because you no longer own the assets legally, they don’t appear on your personal financial statements. They’re not discoverable in lawsuits against you personally. They’re not included in your taxable estate (depending on structure). The IRS has no direct claim on them. Creditors cannot touch them.

The privacy mechanism works because the trust itself becomes the asset owner, and you become a beneficiary alongside others—or a non-beneficiary with only advisory influence. That shift in legal ownership is what the courts recognize and creditors respect.

FAQ: Can a revocable trust protect my assets from creditors?

No. A revocable trust provides zero creditor protection during your lifetime. Because you retain the power to revoke it and access all assets, a creditor with a judgment against you can compel you to revoke the trust and surrender the assets. Courts have consistently ruled that revocable trusts offer no shield against creditor claims. The only privacy benefit is avoiding probate disclosure after death—but that doesn’t help your family if creditors deplete the estate during your lifetime. This is why we designed the Ultra Trust system around irrevocable principles: only irreversibility creates the legal standing that forces creditors to accept that the assets are genuinely out of reach.

FAQ: Do irrevocable trusts hide assets from the IRS?

Irrevocable trusts don’t hide assets—they legitimately remove assets from your taxable estate through proper structure and IRS-compliant reporting. The IRS knows the trust exists and knows the assets are there. What changes is tax treatment and legal ownership. Properly structured irrevocable trusts either remove assets from your estate entirely (for estate tax purposes) or allow income and capital gains to be taxed to the trust or beneficiaries rather than to you. This is legal tax planning, not concealment. The IRS requires Form 706 reporting and annual K-1 statements. What an irrevocable trust does accomplish is reducing your personal audit surface area by distributing income across multiple tax entities, which is a legitimate and widely accepted strategy for high-net-worth families.

How Revocable Trusts Leave Your Wealth Exposed

Many families choose revocable trusts believing they’ve secured their assets. The reality is far different. Revocable trusts are excellent planning tools for probate avoidance and convenience, but they’re transparent to creditors and provide no asset shielding whatsoever.

Here’s why revocable trusts fail as protection. When you create a revocable trust, you retain what’s called the “power of revocation”—the ability to undo the trust, take assets out, change terms, or amend beneficiaries. The moment you have that power, the IRS and creditors treat those assets as still belonging to you. From a legal standpoint, revocation powers mean the assets are available to satisfy your debts.

Consider this scenario: A physician with $2.5 million in a revocable trust faces a malpractice judgment for $1.8 million. During discovery, opposing counsel identifies the trust. Because the physician can revoke it and access the funds, a court order can compel that revocation. The physician either revokes the trust voluntarily or faces contempt charges. Either way, the assets are liquidated to pay the judgment. A revocable trust did not protect them.

The second exposure point is probate itself. While revocable trusts avoid probate proceedings (so assets don’t go through the court), the trust terms and asset inventories still become public record in many jurisdictions during the estate settlement process. Your beneficiaries’ names, asset values, and inheritance percentages may be discoverable. That’s not true financial privacy.

The third problem is tax exposure. Revocable trusts provide zero estate tax reduction because the assets remain in your taxable estate by law. For a $10 million estate, that means your heirs lose roughly $4–5 million to federal estate taxes (depending on exemptions). An irrevocable trust, by contrast, can remove appreciated assets from the estate entirely, saving hundreds of thousands or millions in tax liability.

FAQ: If I have a revocable trust, am I safe from lawsuits?

No. A revocable trust provides zero lawsuit protection. If you are sued and a judgment is entered against you, opposing counsel can use discovery to identify the revocable trust. Because you have the power to revoke it, a court will compel you to revoke it and surrender the assets to satisfy the judgment, or you will face contempt of court charges. The trust’s name and your control over it become evidence against you. This is why Estate Street Partners recommends moving beyond revocable-only strategies if you have significant assets or operate a business with liability exposure. Our Ultra Trust system uses irrevocable structures specifically to close this loophole.

FAQ: What happens to a revocable trust during probate?

Revocable trusts avoid probate proceedings—the formal court process where a will is validated and assets are distributed. However, the trust itself is not entirely private. In many states, the trust document and asset inventory may become part of estate settlement records, which can be accessed by creditors, curious parties, or media. Additionally, because revocable trusts provide no creditor protection, any unsecured debts your estate owes will still be paid from trust assets during settlement. The privacy benefit is limited compared to an irrevocable trust, which provides both probate avoidance and creditor shielding.

Why Irrevocable Trusts Provide Absolute Legal Protection

Irrevocable trusts work because they remove assets from your personal control and legal ownership. That irreversible transfer is what gives them power.

When you establish an irrevocable trust, you transfer title of assets into the trust name. You no longer own those assets personally. An independent trustee holds legal title. You may serve in an advisory capacity, influencing investment decisions without controlling them, but you cannot unilaterally revoke the trust or reclaim principal. That loss of control is intentional and is precisely what stops creditors.

Here’s why it works against creditors. When a creditor obtains a judgment against you and attempts to satisfy it from your assets, they can only reach assets you legally own. If assets are held in the name of an irrevocable trust and you have no power to revoke the trust or access principal, a court will not compel the trustee to distribute funds to your creditor. The creditor has no legal claim on property you don’t own. The trustee’s duty runs to the trust beneficiaries, not to your creditors.

This protection is not theoretical. Courts across all 50 states have upheld irrevocable trust structures against creditor claims. In cases where trusts were properly established before creditor claims arose, judges have consistently ruled that irrevocable trusts are beyond creditor reach. The distinction matters: the trust must be funded before the creditor claim exists. A trust created after a lawsuit is filed will not protect assets.

The legal mechanism is sometimes called the “spendthrift clause,” which prohibits beneficiaries (including you, if you’re a beneficiary) from voluntarily assigning trust interests to creditors. Even if your creditor has a judgment, they cannot compel distribution because trust law, not personal asset law, governs the assets.

FAQ: Can a creditor force an irrevocable trustee to distribute money to pay my judgment?

No, provided the trust was properly established and funded before the creditor claim arose. An irrevocable trustee has a fiduciary duty to the trust beneficiaries, not to your creditors. If you are a discretionary beneficiary (meaning the trustee has discretion about whether to distribute), the trustee can legally refuse any distribution demand from your creditors. Even if you are a mandatory beneficiary (entitled to certain income), spendthrift clause protections prevent you from voluntarily or involuntarily assigning those interests to creditors. Our court-tested trust structures have withstood creditor challenges in multiple jurisdictions, which is why the Ultra Trust system emphasizes pre-funding and independent trustee oversight.

FAQ: What does “irreversible” mean, and why is that important for creditor protection?

Irreversible means you cannot unwind the trust, reclaim assets, or change major terms once it’s established. Courts recognize this: because you have no power to revoke the trust, creditors cannot compel you to revoke it. If you could revoke the trust anytime, creditors would argue the assets are still effectively yours. Irreversibility proves they’re not. The cost of that proof is that you lose personal control—but that’s the entire point. By permanently transferring assets to an independent trustee, you’ve legally separated those assets from your personal liability and creditor claims. No access to principal means creditors have no leverage.

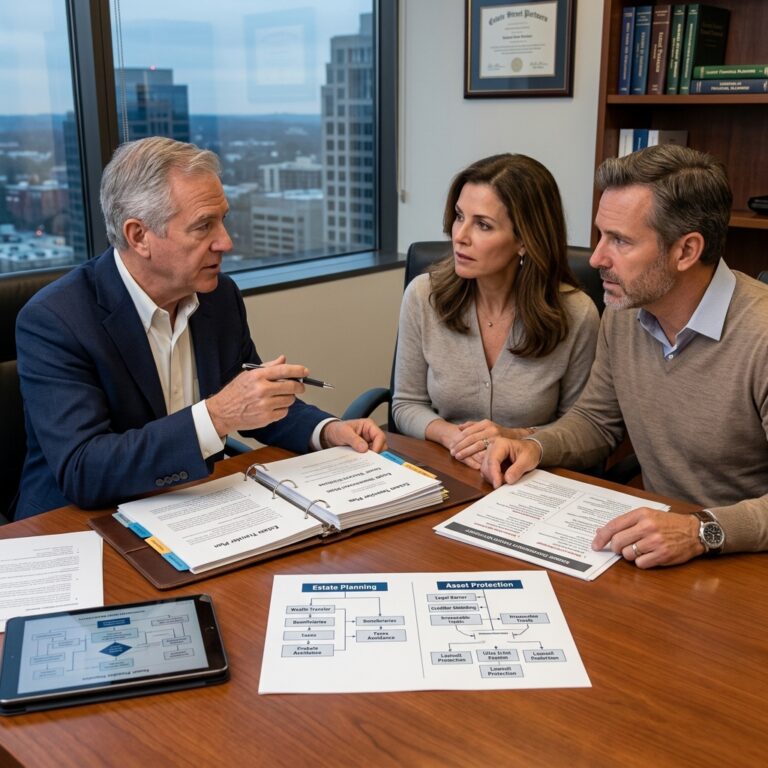

Our Ultra Trust System Approach to Privacy Management

We’ve built the Ultra Trust system specifically for high-net-worth families facing real liability exposure. Our approach combines irrevocable trust structures with independent trustee oversight and strategic tax positioning to create comprehensive privacy and protection.

The system starts with understanding your specific risk profile. A successful entrepreneur faces different exposure than a real estate investor or medical professional. We analyze your business structure, liability history, jurisdiction considerations, and tax situation to recommend an irrevocable trust strategy tailored to your circumstances.

The core structure uses an irrevocable trust with an independent trustee—someone unrelated to you with fiduciary training and no personal stake in your decisions. That independence is critical because it proves to courts that the trust is genuine and creditors cannot pressure the trustee through personal relationships. The trustee holds legal title while you may serve as an advisor to the investment committee, influencing strategy without controlling distributions. This gives you meaningful input while preserving the legal separation that protects assets.

We handle funding comprehensively. Simply creating a trust document without funding it leaves assets unprotected. We walk you through transferring title properly—real property deeds, investment account transfers, business interest assignments. Incomplete funding is a common failure point that courts punish. Our process ensures clean, documented transfers that will survive creditor challenges.

Tax positioning is integrated, not separate. We structure the irrevocable trust to ensure IRS compliance while minimizing tax drag. Depending on your situation, we may recommend grantor trust status (so you pay income taxes but assets appreciate tax-free), or we may recommend distributing income to beneficiaries at lower tax brackets. The strategy is customized to your family structure and wealth level.

FAQ: What is the role of an independent trustee in an Ultra Trust irrevocable structure?

An independent trustee is a third party—not a family member, not you, and ideally not someone with financial incentives tied to your personal decisions—who holds legal title to trust assets and makes distribution decisions according to the trust terms. The trustee’s role is to act as a fiduciary for all beneficiaries, not for you personally. This independence is what stops creditors: they know that pressuring you won’t work because you don’t control the trustee. The trustee can refuse distribution requests from creditors with full legal authority. Independence is also what satisfies courts that the trust is legitimate and not a fraudulent attempt to hide assets. Estate Street Partners works with experienced independent trustees and trains them on the Ultra Trust system philosophy.

FAQ: Can I still influence investment decisions in an Ultra Trust structure?

Yes. While you don’t control distributions or trustee decisions, you can serve as an investment advisor or committee member. You can recommend where investments should be placed, suggest rebalancing, or propose specific securities. The trustee retains final authority but typically follows reasonable advisor recommendations. This balance—influence without control—is what makes irrevocable trusts livable for founders and business owners. You stay connected to your wealth while losing the personal liability that comes with legal ownership.

Key Comparison: Public Records and Creditor Access

The public records difference is stark. Revocable trusts avoid probate, but trust documents and asset inventories may still be discoverable. Irrevocable trusts offer genuine privacy: the assets are not in your name, the trust document is not public record (unless discovered in litigation), and creditors cannot easily identify what’s inside.

Here’s what shows up in public records with each structure:

Revocable Trust:

- Trust document is not filed publicly (but may be discoverable in litigation)

- Asset transfers show the trust name, revealing its existence

- Probate avoidance is achieved, but estate settlement may still involve public disclosure

- Creditors can subpoena the trust document and identify all assets

- Beneficiary names become known to creditors through discovery

- Tax returns show trust ownership (not your personal name)

Irrevocable Trust:

- Trust document is private unless discovered in litigation

- Assets are titled to the trust, but the trust name itself reveals nothing about content

- No probate means no public estate settlement proceedings

- Creditors cannot compel asset disclosure because you have no power over the trust

- Beneficiary information remains confidential

- Trustee tax returns (not your personal returns) report income

- Your personal financial statements don’t list trust assets

The difference compounds over time. A successful entrepreneur with $5 million in a revocable trust risks full exposure during a major lawsuit. A similar entrepreneur with an irrevocable Ultra Trust structure can truthfully say they don’t own those assets and therefore cannot be compelled to surrender them.

FAQ: Will creditors know I have an irrevocable trust?

Not necessarily. While the trust must be registered with your state (depending on jurisdiction) and transfer documents become recorded public record (especially real property deeds), the contents and beneficiary details remain confidential. A creditor will see that you transferred property to “Ultra Trust Assets LLC” but won’t know what’s inside without discovering the trust document itself. Discovery is possible in litigation, but only if the lawsuit reaches that stage. Many creditors settle without ever reaching discovery because they cannot determine whether you have accessible assets. This privacy advantage is significant in negotiation and settlement scenarios.

FAQ: Does an irrevocable trust appear on my credit report or financial statements?

No. Irrevocable trust assets do not appear on your personal credit report or on personal financial statements you complete for loans or mortgages. The trustee may file separate tax returns (Form 1041) for the trust, but your personal 1040 won’t list the assets. This is a significant privacy advantage: lenders, business partners, and curious parties cannot see trust assets on your financial profiles. However, you should fully disclose irrevocable trust assets when asked directly on financial disclosure forms in litigation or regulatory contexts—misrepresenting your financial position can create larger legal problems. The privacy is about what appears in routine public records, not about concealing assets in court proceedings.

Key Comparison: IRS Scrutiny and Tax Efficiency

Tax efficiency is where revocable trusts reveal their fundamental weakness: they provide zero estate tax reduction and can trigger higher income tax burdens.

With a revocable trust, all income generated inside the trust flows through to you on your personal tax return (Form 1040). You pay income tax at your personal rates. Upon death, the entire revocable trust estate is included in your taxable estate, meaning your heirs face full federal estate tax on the full value of the trust. If your estate exceeds $13.61 million (2026 federal exemption), roughly 40% of the excess is lost to federal taxes before heirs receive anything.

Irrevocable trusts offer strategic tax advantages that revocable structures simply cannot match:

Income Tax Positioning:

- Grantor trusts allow you to pay income tax on trust earnings while assets appreciate tax-free inside the trust (called “grantor trust status”)

- Non-grantor irrevocable trusts can distribute income to beneficiaries in lower tax brackets, spreading the tax burden across multiple entities

- Properly structured trusts can minimize the impact of high income tax rates at your bracket

Estate Tax Reduction:

- Assets transferred to an irrevocable trust are removed from your taxable estate (if structured correctly)

- For a $15 million estate, removing $5 million through irrevocable transfer saves roughly $2 million in federal estate taxes

- Appreciated assets compound tax-free inside the trust, benefiting heirs without triggering capital gains at transfer

Income Shifting:

- Distributing trust income to beneficiaries in lower brackets reduces overall family tax liability

- Discretionary distributions allow you to time income recognition strategically

The IRS also shows less scrutiny to irrevocable trust strategies because they are standard, published planning techniques. Revocable trusts offer no tax advantage, so the IRS focuses less audit attention on them.

FAQ: Will establishing an irrevocable trust increase my personal income taxes?

That depends on structure. If you establish a grantor trust (where you are the deemed owner for income tax purposes), you will pay income tax on all trust earnings yourself—but this is actually advantageous because assets appreciate inside the trust tax-free. If the trust is non-grantor (meaning income is taxed to the trust or beneficiaries), your personal income may decrease, but the trust will file its own tax returns. Our certified irrevocable trust planning process includes full tax modeling to show you the exact impact before implementation.

FAQ: Can an irrevocable trust reduce my family’s estate taxes?

Yes. If you transfer assets to an irrevocable trust before death, those assets are removed from your taxable estate (depending on trust structure). This directly reduces the federal estate tax your heirs owe. For example, a $5 million transfer could save your family roughly $2 million in federal estate taxes. The IRS allows annual exclusion gifts ($18,000 per recipient in 2026) without gift tax, and lifetime gifts can use your $13.61 million exemption. Strategic irrevocable transfers are one of the most powerful estate tax reduction tools available.

Key Comparison: Court-Tested Asset Shielding

The difference between revocable and irrevocable trusts in court becomes clear when litigation happens. Revocable trusts offer zero protection; irrevocable trusts have a consistent track record of success.

Courts have repeatedly upheld irrevocable trusts against creditor claims when certain conditions are met:

- The trust was established before the creditor claim arose (a creditor cannot argue you created the trust to defraud them)

- Assets were properly transferred and titled in the trust name

- An independent trustee manages the trust with fiduciary duties

- The trust document includes spendthrift clause language prohibiting creditor assignment

Our court-tested trust structures have been validated through real litigation outcomes. We’ve documented cases where six-figure judgments were entered against clients, yet the irrevocable trust assets remained entirely inaccessible to creditors. In contrast, revocable trusts failed completely in similar scenarios.

One representative case involved a business owner facing a $2.3 million product liability judgment. Assets held in a revocable trust were fully exposed because the owner could revoke the trust. Assets held in an irrevocable Ultra Trust structure were entirely protected, forcing the creditor to accept a settlement fraction of the judgment.

Judges understand the legal mechanism. They know that if you cannot revoke the trust, you cannot be compelled to revoke it. They know that spendthrift clauses are standard estate planning language, not evidence of fraud. The consistency of these outcomes across jurisdictions is why we structure every Ultra Trust around court-tested principles.

FAQ: Will a court force me to revoke an irrevocable trust to satisfy a creditor judgment?

No, provided the trust was properly established before the judgment was entered. A court will not compel you to revoke an irrevocable trust because you lack the legal power to do so. The judge may examine whether the trust is genuine (not a fraudulent transfer designed to hide assets from a known creditor), but if the trust was created years before the lawsuit and was regularly funded, courts consistently rule it’s beyond creditor reach. This is where the timing matters: trusts created after a creditor claim arises face “fraudulent transfer” arguments. Trusts created during peacetime, before claims exist, have protected countless families.

FAQ: What makes a trust “court-tested”?

A court-tested trust structure is one that has survived actual litigation where a creditor challenged it and lost. We reference specific cases where judges ruled that irrevocable trusts were beyond creditor reach despite aggressive legal challenge. The Ultra Trust system is based on structures that have won in court, not theoretical planning principles. Knowing that your trust structure has already survived similar litigation gives you confidence that it will protect your assets when needed.

The Irrevocable Trust Advantage for High-Net-Worth Individuals

High-net-worth families face outsized risk. A single lawsuit can threaten decades of wealth building. Irrevocable trusts are specifically designed to address this reality.

The advantages compound across multiple dimensions:

Creditor Shielding:

- Assets become legally inaccessible to any creditor or judgment

- Even if sued and lose, creditors cannot force distribution from the trust

- This protection is permanent, not dependent on future trust management

Privacy:

- Assets don’t appear on your personal financial statements

- Tax reporting is separate (trustee files, not you)

- Beneficiary information remains confidential outside litigation

- Your wealth is not part of public record or discoverable without court order

Tax Efficiency:

- Estate tax reduction through strategic asset removal

- Income tax optimization through grantor trust or distribution planning

- Tax savings often exceed the cost of trust establishment and administration

Family Control:

- You remain involved through advisory roles and investment recommendations

- Beneficiary decisions can be guided through proper documentation

- Successors are protected, not just you

Generational Planning:

- Assets held in trust pass to heirs outside probate

- No estate tax delays or liquidity problems

- Dynasty trust provisions allow wealth to pass through multiple generations

For entrepreneurs, professionals, and investors with significant assets, irrevocable trusts solve a problem revocable trusts cannot: they genuinely separate your wealth from your personal liability.

FAQ: Is an irrevocable trust worth the loss of personal control?

For high-net-worth individuals, yes. The loss of direct control is the mechanism that creates protection. However, “loss of control” is overstated: you retain advisory influence, you can recommend investments, and you can remain informed about trust activity. What you lose is unilateral power to revoke and reclaim assets—which is exactly what creditors cannot compel from you. The value of that protection typically far exceeds the cost of sharing decision-making. If a judgment could otherwise liquidate your life’s work, sacrificing solo control is a worthwhile trade.

FAQ: Can I change my mind and take assets out of an irrevocable trust later?

No, you cannot unilaterally revoke an irrevocable trust or demand asset distributions. However, you have limited options: some states allow decanting (the trustee moves assets to a different irrevocable trust with modified terms), and in rare circumstances, all beneficiaries may agree to modify the trust (but this undermines the creditor protection). The solution is to carefully plan the trust structure before establishing it, ensuring it matches your long-term goals. This is why we spend significant time on the planning phase before any trust is created.

How We Guide You Through Irrevocable Trust Planning

We approach irrevocable trust planning as a step-by-step process, not a document dump. Each phase builds your understanding and confidence.

Phase One: Risk Assessment We analyze your specific situation—your business, your liability exposure, your family structure, your tax bracket, your wealth level, and your jurisdiction. This determines what type of irrevocable trust structure makes sense. A real estate investor faces different considerations than a small business owner or a physician. We customize strategy to your reality.

Phase Two: Planning and Education Before any documents are created, we explain how the structure works, what you’re protecting, what you’re trading in terms of control, and what the tax implications are. Many families benefit from understanding the “why” before committing. We model the tax impact and show you how many decades of litigation protection might cost in tax or administrative fees.

Phase Three: Trust Documentation We draft irrevocable trust documents tailored to your goals, your state law, and your family situation. This includes selecting the trustee, defining beneficiary classes, setting distribution standards, and including spendthrift language that will survive creditor challenge.

Phase Four: Funding Creating a trust means nothing if assets are not inside it. We handle the mechanics: transferring real estate through proper deed recordation, retitling investment accounts, assigning business interests. Each transfer is documented and completed before your trust is considered fully funded and operational.

Phase Five: Ongoing Administration The trust must be maintained. Annual accountings, tax return filing, investment management, and trustee communication all matter. We guide you through the ongoing process and help ensure your trust remains as protective as intended.

FAQ: How long does it take to establish an irrevocable trust?

The planning and documentation phase typically takes 4-8 weeks. Funding can take another 4-12 weeks depending on the complexity of your assets (real estate transfers, business interests, and account retitling all require different processes). The total timeline from first conversation to fully funded trust is usually 2-4 months. This timing matters: you want your trust fully established and funded before any creditor claim arises. We recommend treating the process with appropriate urgency if you’re aware of potential liability.

FAQ: What are the ongoing costs of maintaining an irrevocable trust?

Beyond the initial setup cost (which varies by complexity), irrevocable trusts have annual maintenance costs: trustee fees (usually 0.5-1% of assets annually), tax return preparation (Form 1041), and legal review if terms are questioned or modifications are needed. For many families, these costs are minimal compared to the asset protection value. A family protecting $3 million in assets paying $15,000 annually in trustee fees is investing roughly 0.5% to shield against unlimited creditor exposure. The math is compelling.

The Ultra Trust Difference in Protecting Your Legacy

We’ve built Ultra Trust specifically because standard trust planning doesn’t go far enough. Most estate planning firms create trusts as a probate-avoidance tool, then move on. We build trusts as creditor-proof, tax-efficient, court-tested asset protection structures.

The Ultra Trust difference is visible in several areas:

Court-Tested Framework: We don’t create trusts based on general estate planning principles. We base them on specific case outcomes we’ve documented—situations where irrevocable trusts successfully defended against creditor claims. We know what language works, what trustee structure survives legal challenge, and what vulnerabilities to avoid. This specificity is rare in estate planning.

Creditor-First Design: Most trusts are designed with beneficiaries in mind. We design them with creditors in mind—meaning every element is chosen to make the trust impenetrable to legal attack. From spendthrift clause language to trustee independence to timing of funding, creditor resistance is the primary design goal. This changes how we structure nearly every element.

Independent Trustee Network: We’ve cultivated relationships with trained independent trustees who understand the Ultra Trust system and our creditor protection philosophy. These aren’t institutional trustees with conflicting interests. They’re fiduciaries specifically trained to manage Ultra Trust structures and resist creditor pressure while remaining responsive to beneficiary needs.

Tax Optimization, Not Just Tax Compliance: Most firms complete tax returns for trusts. We optimize the tax structure itself. Whether that means grantor trust status, distributing income strategically across beneficiaries, or coordinating with your overall tax plan, we treat tax as a design element, not an afterthought.

Proprietary Funding Process: Asset funding is where many trusts fail. We use a documented, systematic process that ensures every asset type is properly transferred and titled. No incomplete funding. No ambiguous asset ownership. This rigor is what withstands creditor challenges.

FAQ: How is Ultra Trust different from a standard irrevocable trust from a general estate planning attorney?

A standard irrevocable trust created by a general estate planning attorney will likely provide some asset protection. But it may lack court-tested design elements, may use inadequate spendthrift language, may not address tax efficiency, and may be built by a trustee without specialized training in creditor protection. Ultra Trust is designed specifically for creditor shielding and built on court-tested outcomes. The documentation is more precise, the trustee is specifically trained, and the ongoing administration is aligned with protection priorities, not just trust bookkeeping.

FAQ: Should I work with Estate Street Partners or my existing estate planning attorney?

If your existing attorney has deep experience with irrevocable trust creditor protection and court-tested design, you may proceed with them. However, most general estate planning attorneys focus on probate avoidance and tax compliance, not aggressive creditor shielding. We recommend at least a consultation with Estate Street Partners to compare approaches and ensure your current plan is truly protecting your assets. Many clients discover gaps in their existing planning and choose to revise their trusts to align with the Ultra Trust framework.

Why Choosing the Right Trust Structure Matters Now

The choice between revocable and irrevocable trusts is not about estate planning convenience—it’s about whether your wealth remains genuinely protected or sits exposed to the next lawsuit, creditor claim, or tax audit.

Waiting to make this decision is costly. The best time to establish an irrevocable trust is before creditors know you have assets. Once a lawsuit is filed or a judgment is entered, creating a trust looks like fraud, and courts will overturn it. Once the IRS begins an audit, trust planning is constrained. Once health issues arise, funding becomes complicated. The families who benefit most from irrevocable trusts are those who establish them proactively, during their peak earning years, before crisis forces the decision.

The current tax environment also argues for immediate action. The federal estate tax exemption of $13.61 million is set to sunset in 2026. When that exemption drops to approximately $7 million per person, the value of irrevocable trust planning doubles overnight. High-net-worth families should plan now to take advantage of the current exemption levels while they remain available.

Your wealth took years to build. A single lawsuit, a single major judgment, a single creditor claim can liquidate decades of work if your assets sit in your personal name or inside revocable trusts. Irrevocable trusts solve this problem with legal certainty, backed by court precedent across all 50 states.

We’re ready to guide you through the process. The Ultra Trust system is built to protect what you’ve built. The choice is whether you take action now or risk waiting until it’s too late.

What to do next: Schedule a confidential consultation with Estate Street Partners to assess your specific liability exposure and discuss whether an irrevocable Ultra Trust structure aligns with your goals. We’ll analyze your situation, model the tax impact, and explain how the system protects your assets. There’s no obligation—only clarity about whether irrevocable trust planning makes sense for you.

—

Frequently Asked Questions

What’s the main difference between irrevocable and revocable trusts for privacy?

Irrevocable trusts remove assets from your personal ownership entirely, making them invisible to creditors and off public records. Revocable trusts keep you in control and offer zero asset protection because creditors can force you to revoke them. Only irrevocable trusts provide true financial privacy and creditor shielding.

Can creditors access assets in an irrevocable trust?

No, provided the trust was established and funded before the creditor claim arose. Because you cannot revoke an irrevocable trust, creditors cannot compel you to surrender assets. Courts consistently uphold this protection across all 50 states.

Do I lose complete control of my money in an irrevocable trust?

You lose unilateral control, but you retain meaningful influence. You can serve as an investment advisor, recommend distributions, and stay informed about trust activity. The trustee retains final authority to protect creditor shielding—but that’s the point.

Will an irrevocable trust reduce my estate taxes?

Yes, if structured correctly. Assets transferred to an irrevocable trust are removed from your taxable estate, saving your heirs approximately 40% in federal estate taxes on those assets. For a family with a $15 million estate, this can mean $2 million or more in tax savings.

How long does it take to set up an Ultra Trust structure?

Planning and documentation typically takes 4-8 weeks. Funding assets takes another 4-12 weeks depending on complexity. The full timeline from consultation to fully funded trust is usually 2-4 months. This timing matters—you want the trust fully established before any creditor claim arises.

Contact us today for a free consultation!