Why Most Wealthy Families Face Critical Planning Gaps

Key Takeaways

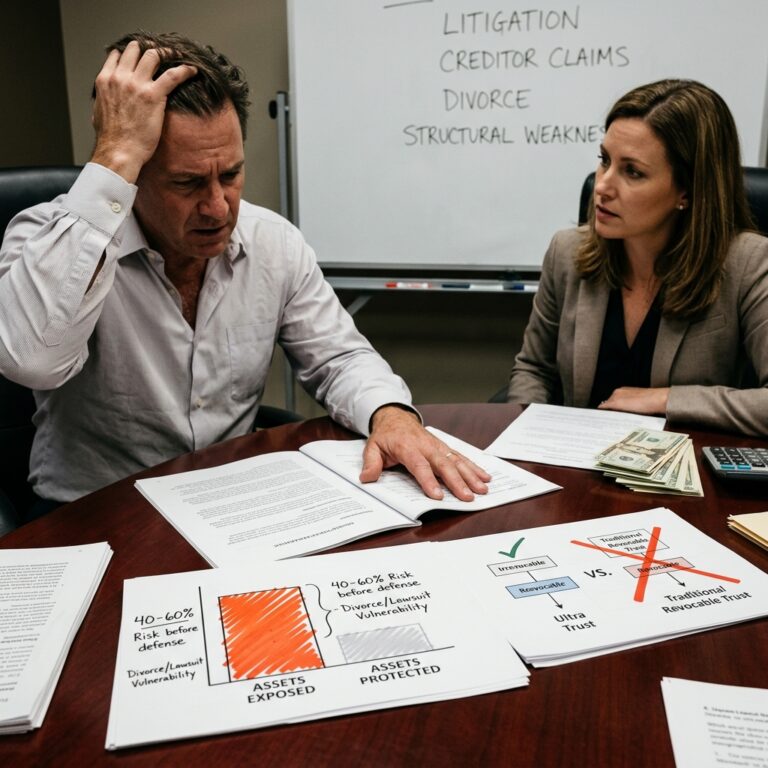

- Estate planning and asset protection serve different purposes: estate planning transfers wealth efficiently after death, while asset protection shields assets from creditors and lawsuits during your lifetime.

- Most wealthy families use only estate planning, leaving themselves exposed to lawsuits, IRS claims, and creditor judgments that can wipe out unprotected assets.

- Irrevocable trusts provide both tax efficiency and creditor protection by permanently removing assets from your estate and placing them beyond the reach of future claimants.

- Our Ultra Trust system integrates both strategies into a court-tested framework that ensures your wealth survives legal threats while minimizing tax liability.

- IRS compliance and proper trust structuring are non-negotiable; mistakes in either area can collapse both your estate plan and asset protection simultaneously.

—

The gap between what wealthy families think they’re protected against and what they actually are protected against is enormous. Most high-net-worth individuals focus exclusively on estate planning, ensuring their heirs inherit smoothly and taxes are minimized at death. What they overlook is that death is only one threat to wealth. Lawsuits, creditor claims, divorce proceedings, and IRS disputes can strike during your lifetime, when your assets are most vulnerable and when you’re still responsible for defending them.

We’ve worked with entrepreneurs who had meticulously planned their estates but had zero legal shields against a malpractice suit, a business partner’s bankruptcy claim against shared assets, or an unexpected tax audit. By the time they called us, the damage was already beginning. The problem isn’t that their estate plan was poorly designed. It’s that an estate plan alone doesn’t stop a judgment creditor from seizing bank accounts, investment portfolios, or business interests while you’re alive.

Most advisors stop at wills and revocable trusts. Those tools handle probate avoidance and tax deferral, but they provide almost no creditor protection. A revocable trust is fully available to creditors because the grantor retains control and access. The result is a false sense of security: families believe they’re protected when they’re actually exposed.

FAQ: What’s the difference between revocable and irrevocable trusts in terms of creditor protection?

A revocable trust gives you full control but zero creditor protection, while an irrevocable trust removes assets from your control but places them beyond the reach of future creditors. With a revocable trust, you maintain the right to modify, amend, or revoke the document at any time, and you retain access to the income and principal. This flexibility means creditors see the trust assets as effectively yours and can pursue them. With an irrevocable trust, once you transfer assets in, you surrender the power to change the terms or reclaim the property. That surrender of control is precisely what makes creditors legally unable to touch the assets. The IRS and courts have consistently upheld this distinction. Our Irrevocable trust guide explains how this transfer actually strengthens your protection posture while still allowing your family to benefit.

FAQ: Can I lose access to my money if I put it in an irrevocable trust?

Yes, you lose direct access to principal, but that’s the trade-off for creditor immunity. However, our Ultra Trust system is designed so that an independent trustee can distribute income and principal to you for legitimate living expenses, education, healthcare, and other named purposes. You don’t control the distributions, but a neutral third party does, which is exactly what makes the protection valid. Many families structure irrevocable trusts so they retain some access through distributions while the asset base itself remains protected from lawsuits and creditors.

—

The Fundamental Difference Between Estate Planning and Asset Protection

Estate planning answers one question: how do I transfer my wealth efficiently when I die? Asset protection answers a different question: how do I prevent creditors and litigants from taking my wealth while I’m alive? These are not the same goal, and they require different legal tools.

Estate planning focuses on probate avoidance, tax efficiency at death, and clear instructions for who inherits what. It typically uses wills, revocable trusts, and beneficiary designations. The goal is orderly, tax-smart transfer of assets to your chosen heirs. It’s about legacy and intent.

Asset protection focuses on structuring assets so creditors cannot reach them if you’re sued, face a judgment, or encounter an IRS claim. It uses ownership structures that separate you from the assets or restrict creditors’ legal rights to access them. The goal is preservation and insulation.

A typical scenario: You own a business worth $8 million and have properly planned your estate so your children inherit it with minimal estate tax through a revocable trust. But during your lifetime, a customer sues over an alleged defect and wins a $2.5 million judgment. If your business assets are held in an unprotected structure, that judgment creditor can seize and liquidate them to satisfy the debt. Your beautiful estate plan means nothing if there’s nothing left to pass on.

Conversely, asset protection without estate planning creates a different problem. You shield assets from creditors, but when you pass away, those assets may be trapped in irrevocable structures that create confusion, tax inefficiency, or delayed distributions to your heirs.

FAQ: Why can’t a single trust document handle both estate planning and asset protection?

A single revocable trust cannot because creditor protection requires you to surrender control, which contradicts the flexibility you need in an estate plan. An irrevocable trust can provide both, but the structure must be carefully designed so that you receive the asset protection benefit without triggering unintended tax consequences or losing the ability to modify distributions to heirs. Our estate planning trusts resource walks through how to structure a dual-purpose trust that satisfies both objectives.

FAQ: If I have asset protection in place, do I still need to update my estate plan?

Yes. Asset protection and estate planning operate on different timelines and trigger different legal consequences. Your estate plan must be reviewed after major life events (marriage, divorce, children, changes in net worth), tax law changes, and changes in state residency. Your asset protection strategy should also be reviewed if you face new liability exposure, state law changes, or if your business structure changes. These reviews are separate processes that sometimes inform each other.

—

How Estate Planning Alone Leaves Your Wealth Vulnerable

Without asset protection, your estate plan is like a beautifully locked front door on a house with an open back window. You’ve solved one problem (avoiding probate) but you’ve ignored the bigger threat (creditors walking through the unguarded entrance).

Consider a real scenario: A physician in her 50s has an estate plan that minimizes taxes and ensures her three children inherit the $6 million investment portfolio. But she maintains a medical practice. A patient outcome goes badly, and despite insurance, a judgment for $4 million is entered against her personally. Even though her investment portfolio is technically in a revocable trust (which avoids probate), creditors can still reach it because she retained control over those assets. The trust provided zero protection.

The same vulnerability exists with business owners. Your estate plan might ensure your company passes to your children, but if you hold business interests in your personal name or in a standard revocable trust, a single lawsuit during your working years can force a liquidation. Your children inherit nothing because the business was sold to satisfy a judgment.

Estate planning trusts also create a false sense of security because people confuse “avoiding probate” with “protecting from creditors.” These are entirely different legal outcomes. A trust that avoids probate may still be fully exposed to creditor claims.

Additionally, many estate plans include detailed provisions for your heirs that become irrelevant if the underlying assets have been seized. You’ve detailed who gets what, but there’s nothing left to distribute. The emotional and financial impact on your family extends beyond lost dollars. It includes the family conflict, liquidation costs, and legal fees that arise when an unprotected estate must defend against aggressive creditor collection.

FAQ: If my estate is in a trust, won’t the trust protect me from lawsuits?

Not unless the trust is irrevocable and was established with the specific intention to provide asset protection. A revocable trust is a probate avoidance tool, not a creditor protection tool. Because you retain full control and can modify or revoke the trust at any time, courts treat the assets as your own for creditor purposes. An irrevocable trust works differently because you’ve permanently transferred the assets out of your estate, which changes the legal relationship between you and those assets.

FAQ: What happens to my estate plan if I get sued before I die?

If a judgment creditor wins a claim against you, they will attempt to levy your assets, including those in a revocable trust. This can force liquidation, delay distributions to your heirs, and create conflict among family members who are waiting for their inheritances while legal proceedings drag on. An asset protection strategy in place before litigation occurs can prevent this scenario entirely.

—

The Hidden Creditor Risks That Estate Planning Cannot Prevent

Creditor risk comes from many directions, and estate planning addresses none of them. Most high-net-worth families assume their greatest exposure is from a catastrophic lawsuit. While that’s certainly a risk, the reality is broader and more subtle.

Judgment creditors are one threat, but there are others: IRS liens for unpaid taxes can attach to all your property. Divorce proceedings can create claims against assets you thought were protected. Bankruptcy of a business partner or co-owner can force the sale of jointly held assets. Even a personal guarantee on a business loan can expose your individual assets if the business fails. A malpractice claim, a motor vehicle accident, a slip-and-fall incident on your property, or a contractual dispute can all generate creditor claims that no estate plan will defend against.

We once worked with a construction company owner whose estate plan was flawless. But he’d personally guaranteed a line of credit for his company. When a market downturn hit, the company couldn’t repay the loan, and the lender came after his personal assets. His revocable trust provided zero protection. Because he hadn’t separated his business assets from his personal wealth, the creditor was able to reach his investment portfolio, real estate holdings, and retirement accounts (some of which had limited protections depending on state law and account type).

Another client, a consultant, was hit with an unexpected tax assessment from the IRS following an audit. The amount owed was $1.2 million, and the IRS immediately filed a federal tax lien against all his property. His estate plan didn’t contemplate this scenario because it wasn’t about death or probate. It was about a creditor claim during his lifetime.

The most insidious risk is the one you don’t see coming. Doctors, engineers, contractors, and business owners carry professional liability that extends far beyond traditional insurance limits. A single catastrophic error can generate a claim that exceeds your malpractice coverage. If your personal assets are unprotected, you’re on the hook for the difference.

FAQ: Does homestead exemption or retirement account protection cover all my assets?

No. While some states offer homestead protections (limits on equity a creditor can seize) and federal law protects certain retirement accounts like 401(k)s and IRAs up to certain limits, these are narrow shields. They don’t protect investment accounts, business interests, rental properties, or second homes. And homestead protections vary dramatically by state. If you move states, your protection may disappear. Our asset protection for business owners guide covers which assets receive statutory protection and which require additional structuring.

FAQ: Can I use multiple trusts to protect different assets?

Yes, and that’s often part of a comprehensive strategy. You might use one irrevocable trust for real estate, another for a business interest, and another for investments. However, each trust requires proper funding, independent trustee administration, and IRS compliance. The more trusts you use, the more important it is to have a coordinated strategy so they work together rather than create gaps or contradictions.

—

Asset Protection: The Missing Piece in Your Wealth Strategy

Asset protection is the deliberate structuring of your wealth so that creditors cannot legally reach it. It’s not about hiding money or evading lawful obligations. It’s about using legal mechanisms that the courts have validated and the law permits. When done correctly, it’s entirely transparent and defensible.

The core principle is separation: you remove assets from personal ownership and place them in structures where creditors have no legal claim. An irrevocable trust is one powerful example. Once you transfer assets into an irrevocable trust, they’re no longer yours for creditor purposes. A future creditor cannot force the trustee to give them the money because the trustee’s obligation is to your beneficiaries, not to satisfy your creditors.

This is not theoretical. Courts have upheld irrevocable trusts against creditor claims for decades. The Restatement of Trusts and state-by-state case law consistently hold that an irrevocable trust grantor cannot be forced to undo the trust or compel the trustee to distribute to a judgment creditor. The assets are simply out of reach.

Asset protection also involves understanding which assets you should keep in which structures. Some assets (like business interests) may be housed in an entity that limits liability. Others (like investment portfolios) might go into irrevocable trusts. The strategy depends on your specific exposure, your state of residence, and your family circumstances.

Many wealthy families delay asset protection because they think they don’t need it until they’re sued. That’s backwards. The time to protect your wealth is now, before any creditor claim exists. Courts have the authority to reverse fraudulent transfers made after a claim arises. But if you transfer assets into protection before any creditor is on the horizon, the transfer is legally sound and beyond challenge.

FAQ: Isn’t asset protection expensive and complicated?

It requires expert structuring, yes, but the cost is typically a fraction of what a single lawsuit or tax judgment could cost. If you own significant assets and face any professional liability, a comprehensive asset protection plan is among the highest-ROI financial decisions you can make. Initial setup costs are usually between $5,000 and $25,000 depending on complexity. The cost of losing a $2 million judgment because you had no protection far exceeds that initial investment.

FAQ: Is asset protection legal, or is it a gray area?

Asset protection is completely legal. Courts have upheld properly structured irrevocable trusts, business entities, and other protection mechanisms for over a century. The key distinction is timing: transfers made before any creditor claim exists are presumptively valid. Transfers made after a creditor threatens legal action can be challenged as fraudulent. Work with qualified advisors, document your business rationale (which should be legitimate wealth planning, not creditor evasion), and establish your plan before you need it.

—

How Our Ultra Trust System Integrates Both Protections

We built the Ultra Trust system specifically to solve the problem we’ve described: most families get estate planning or asset protection in isolation, not both in a coordinated way. Our approach integrates irrevocable trust planning with the tax and legacy considerations that matter to high-net-worth families.

Here’s how it works. We start by understanding your full financial picture: your business interests, investments, real estate, and the specific liability exposures you face in your profession or industry. Then we structure an irrevocable trust framework that:

- Removes assets from your personal estate, which shields them from creditors while you’re alive

- Ensures the assets are distributed to your heirs according to your wishes after you pass away

- Minimizes estate taxes through proper valuation and gifting strategies

- Maintains sufficient access to income and distributions so you don’t feel you’ve lost control

- Complies fully with IRS requirements so the tax benefits are real and defensible

The Ultra Trust system is court-tested. We’ve documented cases where families protected through our methodology faced major litigation, and the assets in their irrevocable trusts remained untouched while unprotected assets of other parties in the same disputes were liquidated. That real-world evidence is why we’re confident in the approach.

We also provide step-by-step guidance because the strategy only works if it’s properly funded and maintained. You can have a perfect trust document, but if assets aren’t transferred into it correctly, the protection fails. Our process includes funding checklists, beneficiary documentation, and annual reviews to ensure the structure stays intact and effective.

One more element: we integrate your asset protection strategy with your business structure. If you own a company, we examine whether your business entity itself provides adequate liability shielding, or whether additional protection is needed. Sometimes the business entity is enough; other times, the business interests themselves need to be housed in protective structures.

FAQ: How is the Ultra Trust system different from what I could get from a standard estate planning attorney?

Most estate planning attorneys focus on probate avoidance and tax efficiency at death. They understand estate planning deeply but may not have specialized experience in irrevocable trust creditor protection or the intersection of asset protection and estate tax strategy. The Ultra Trust system is built from the ground up to integrate both functions, and we’ve tested the approach across multiple states and litigation scenarios. We also provide ongoing guidance and documentation support that standard estate plans don’t include.

FAQ: Can I set up the Ultra Trust system myself using online legal services?

You should not attempt this alone. Irrevocable trusts are extraordinarily difficult to unwind if they’re structured incorrectly, and mistakes in IRS compliance can trigger unexpected tax bills. Additionally, the trust must be properly funded, beneficiary documents must be correct, and the trustee must understand their obligations. This is an area where professional guidance is not a luxury but a necessity.

—

The Tax Efficiency Advantage of Irrevocable Trust Planning

Irrevocable trusts offer a tax advantage that revocable trusts cannot match: they remove assets from your taxable estate. When you pass away, your estate is subject to federal estate tax if it exceeds the exemption amount. Anything in your taxable estate is subject to tax at rates up to 40% (as of 2026, though rates may change).

An irrevocable trust works differently. Once you transfer assets into the trust, those assets are no longer part of your taxable estate. If you die five years later, and the trust assets have grown to twice their original value, that growth is outside your estate and avoids estate tax. The difference can be millions of dollars for a large portfolio.

This is not a trick or a loophole. It’s how the tax code is structured. The cost of this tax benefit is that you surrender control over the assets. But many families gladly make that trade: give up control now, shield assets from creditors in the present, and reduce estate taxes in the future.

We often work with families where the patriarch or matriarch has built significant wealth but is concerned about both creditor exposure and tax efficiency. A properly structured irrevocable trust solves both problems simultaneously. The assets are protected during their lifetime and the tax burden on their heirs is reduced.

Additionally, if the irrevocable trust is structured correctly, it can also provide income tax flexibility. Some irrevocable trusts are taxed as separate entities, which means the income generated by trust assets is taxed at the trust level rather than at your personal tax rate. If the trust income is retained in the trust and not distributed to you, the trust pays the tax. This can be advantageous depending on the trust’s income level and tax bracket.

FAQ: Will putting assets in an irrevocable trust reduce my income tax burden?

Not necessarily. You will still owe income tax on the income generated by the trust’s assets, but the tax may be paid by the trust itself rather than by you personally. This depends on how the trust is structured and whether income is distributed to beneficiaries or retained in the trust. Some irrevocable trusts can be structured to shift income taxation to lower-bracket beneficiaries, creating overall tax savings. However, this is a complex area and requires careful planning with a tax professional.

FAQ: If I put assets in an irrevocable trust now, can I access the money if I need it for an emergency?

You cannot directly access the money because you no longer own it. However, if the trust document includes a provision allowing the independent trustee to distribute funds to you for health, education, maintenance, and support, the trustee can provide access in genuine emergencies. This is why the trustee and trust terms must be carefully chosen. You’re relying on the trustee’s judgment and fiduciary obligation to treat you fairly.

—

Lawsuit Protection for Your Legacy: Beyond Basic Estate Plans

A basic estate plan ensures your assets pass to your heirs efficiently. But it does nothing to stop a lawsuit from destroying your family’s wealth before your death. Lawsuit protection requires a different mindset and a different set of tools.

The stark reality is this: you’re more likely to face a major lawsuit during your working years than you are to die. If you’re a business owner, a professional, or someone with significant assets, your liability exposure is continuous. A judgment against you can be entered quickly, and once a judgment exists, a creditor can begin executing against your assets.

We worked with a CPA who had built a $7 million portfolio through decades of careful investing. Her estate plan was exemplary. But during an audit, a client alleged she’d provided negligent tax advice. The client won a $3.2 million judgment. Because her assets were in revocable trusts and investment accounts, they were fully exposed. Even though she had malpractice insurance, the insurance limits were only $1 million. She faced personal liability for the remaining $2.2 million. The judgment creditor began seizing her accounts and placing liens on her property. Had she implemented an irrevocable trust strategy beforehand, those assets would have been beyond reach, and her family’s legacy would have been preserved.

Lawsuit protection also means understanding your specific risks. A surgeon faces different exposure than a consultant. A business owner with employees faces different exposure than a solo entrepreneur. Part of our process is identifying those risks and structuring accordingly.

Additionally, proper lawsuit protection includes choosing the right independent trustee. The trustee is your advocate within the trust structure. Their obligation is to manage the trust assets for the beneficiaries’ benefit, not to satisfy your creditors. Choosing someone who understands this role and who will stand firm if a creditor tries to pressure them into unauthorized distributions is critical.

FAQ: What happens if a creditor learns about my irrevocable trust and tries to take the assets anyway?

A creditor can file a claim or attempt to garnish the trust, but if the trust is properly structured, the trustee’s obligation is to the beneficiaries, not to satisfy the creditor. The trustee should refuse any distribution that isn’t authorized by the trust document or court order. Creditors can challenge the trust in court, but courts have consistently upheld validly established irrevocable trusts against creditor claims. This is why proper documentation and proof that the trust was established for legitimate planning reasons (not in anticipation of the specific creditor claim) matters.

FAQ: If I’m named as a beneficiary of my own irrevocable trust, does that undermine the creditor protection?

Not if the trust is properly structured. You can be a beneficiary, and the trustee can distribute income to you for authorized purposes. However, you cannot be the trustee, and you cannot have the power to force distributions. The key is that distributions are discretionary with the independent trustee, not your right. This distinction is what makes the assets creditor-proof.

—

Why IRS Compliance Matters in Dual-Strategy Wealth Protection

Protecting your wealth means nothing if the IRS audits your trust structure and asserts that it was improperly formed or that your claimed tax benefits are invalid. Many families have learned this lesson the hard way, discovering that an irrevocable trust they established years ago is not recognized by the IRS for the tax benefits they claimed.

IRS compliance has several components. First, the trust must be properly drafted according to IRS guidelines. There are specific language requirements and structural considerations that determine whether the IRS recognizes the trust as valid for tax purposes. Miss one element, and your claimed benefits may be disallowed.

Second, the transfer of assets into the trust must be properly documented. If you transfer a business interest, rental property, or investment account into the trust, you need a deed, assignment, or other documentation that shows the transfer was completed. Claiming the asset is in the trust but failing to actually transfer ownership is a common mistake that collapses both creditor protection and tax benefits.

Third, the trustee must maintain proper records. The trustee should file a Form 1041 (fiduciary income tax return) if the trust generates income. The trustee should maintain documentation of all distributions and retain accounting records. The IRS can challenge a trust if records are incomplete or inconsistent.

Fourth, if the trust is an irrevocable trust with you as a potential beneficiary, the IRS applies specific rules (Grantor Trust Rules) that determine whether the trust’s income is taxed to you or to the trust. If these rules are violated or misapplied, you could face unexpected tax liability.

This is not theoretical. We’ve encountered situations where families had irrevocable trusts that were not properly funded, or where the trustee failed to file required tax returns, or where the trust was structured in a way that the IRS challenges as a sham. The result was denied tax benefits, penalties, and interest. In some cases, the creditor protection benefit was also questioned because the trust lacked the formality that courts require.

The Ultra Trust system is designed to ensure IRS compliance from day one. We work with tax professionals as part of our process, and we document everything according to IRS requirements.

FAQ: What IRS forms and filings does an irrevocable trust require?

If an irrevocable trust is properly structured, the trustee must typically file a Form 1041 (U.S. Income Tax Return for Estates and Trusts) each year if the trust generates income above a threshold. Additionally, if the trust holds certain types of assets (like a business or rental property), additional filings may be required. The trustee must also provide Schedule K-1 forms to beneficiaries if distributions are made. State-level filings may be required depending on your location. Failure to file these forms can trigger IRS notices and penalties.

FAQ: Can I amend an irrevocable trust if I discover an IRS compliance problem?

Generally, no. An irrevocable trust cannot be amended by you. However, in some states, trustee-directed decanting or judicial reformation may allow a trustee to restructure the trust to fix compliance issues. These are complex procedures that require court involvement or careful drafting of the original trust document to permit decanting. This is another reason why getting the structure right initially is critical.

—

Common Mistakes That Undermine Both Strategies

We see the same mistakes over and over. Some families have gone to the trouble of establishing an irrevocable trust only to undermine it through poor administration. Others have implemented asset protection without coordinating it with their estate plan, creating tax inefficiencies or family confusion at death.

Mistake 1: Failing to Fund the Trust

A trust document is just paper. The actual protection comes from the assets inside the trust. Many families establish a beautiful irrevocable trust document and then never transfer assets into it. Their portfolio remains in individual names or in revocable trusts. The irrevocable trust is empty and provides no protection whatsoever. Every asset that should be in the trust must be formally transferred through a deed (for real estate), assignment (for business interests), or retitling (for investments).

Mistake 2: Mixing Control and Protection

Some families try to have it both ways: they want an irrevocable trust (which requires surrendering control) but they want to maintain the ability to direct distributions or change how the trustee manages the assets. This defeats the purpose. If you retain the power to control the trust, courts and creditors see the assets as yours, and the protection disappears.

Mistake 3: Not Choosing an Independent Trustee

The trustee is critical. If you name yourself, your spouse, or your adult child as trustee, creditors will argue that you effectively control the assets and therefore they’re not protected. An independent trustee, someone with no relationship to you and a fiduciary obligation to the beneficiaries, is what makes the structure legally defensible.

Mistake 4: Ignoring Tax Consequences

Some families establish irrevocable trusts without understanding the income tax implications. They may end up with an unexpected tax bill or discover that the trust’s income tax treatment doesn’t match their expectations.

Mistake 5: Creating Confusion for Heirs

An irrevocable trust that protects assets during your lifetime may create confusion after your death if the trust terms and the overall estate plan don’t align. Heirs may not understand how assets will be distributed, which can create family conflict.

FAQ: If I’ve already made mistakes in my asset protection structure, can I fix them?

Some mistakes can be corrected through reformation, decanting, or other trust modifications, depending on the error and your state law. However, the longer you wait, the fewer options you have. If you’re concerned about a mistake you’ve made, consult with an expert immediately. In some cases, you may need to establish a new, corrected structure. This is another reason why getting the initial structure right is critical.

FAQ: How often should I review my estate and asset protection plan?

At minimum, annually. However, you should also conduct a comprehensive review after any major life change: marriage, divorce, birth of a child, significant change in net worth, change of state residency, changes in your business, or changes in tax law. Tax law changes frequently, and what was an optimal structure in 2024 may need modification in 2026 or later.

—

How We Guide You Through Court-Tested Wealth Preservation

Our approach differs from standard legal services because we treat wealth preservation as a coordinated system, not as separate documents. Here’s how we guide you through the process.

Step 1: Comprehensive Discovery

We begin with a detailed conversation about your assets, your family structure, your business interests, your professional exposure, and your goals. We ask about any ongoing litigation or potential disputes. We learn about your previous planning and identify gaps. This discovery phase ensures we understand the full picture before recommending any structure.

Step 2: Risk Assessment

Based on your situation, we identify your specific creditor risks. A business owner with employees faces different exposure than a real estate investor. A physician faces different exposure than a consultant. We outline the liability scenarios you should protect against and explain which assets are most vulnerable.

Step 3: Structure Design

We recommend a specific irrevocable trust structure tailored to your situation. We explain how it will protect your assets, how it will function during your lifetime, and how it will distribute to your heirs. We discuss trustee options and beneficiary structures. We explain the tax implications.

Step 4: Document Preparation

We prepare all necessary documents: the irrevocable trust agreement, deed or assignment documents for transferring assets, beneficiary documentation, and trustee guidance. Every document is drafted with IRS compliance and creditor protection in mind.

Step 5: Implementation and Funding

We provide step-by-step guidance for executing and funding the trust. This includes assisting with deed preparation for real estate, retitling investment accounts, and documenting the transfer of business interests. We ensure nothing is left undone.

Step 6: Trustee Support

We provide the independent trustee with guidance on their obligations and best practices for administration. This includes documentation of trust authority, beneficiary communication, and annual tax filing support.

Step 7: Annual Review and Adjustment

We conduct annual reviews to ensure the structure is functioning correctly, that tax filings are completed, and that any changes in your circumstances or the law are addressed. We also review whether additional assets should be added to the trust or whether the structure needs modification.

This comprehensive approach is why families choose us. A document is just the beginning; the strategy lives in the implementation and maintenance.

FAQ: How involved will I need to be in the process, and how long does it take?

The discovery and planning phase typically takes 2-4 weeks. Once we’ve designed the structure, implementation can take another 2-4 weeks depending on how many assets need to be transferred. The overall timeline from initial consultation to fully funded and operational trust is usually 6-12 weeks. You’ll need to invest time in meetings and in gathering financial documents, but we handle the legal and administrative heavy lifting.

FAQ: What if my situation changes after we implement the plan?

That’s why we conduct annual reviews. If your circumstances change significantly (major life event, significant change in net worth, business sale, change in tax law), we schedule a planning review to assess whether the structure needs modification. Some changes can be addressed within the existing trust through trustee discretion. Other changes may require an amendment or a supplemental strategy. The key is staying in communication and addressing changes promptly.

—

Taking Action: Your Step-by-Step Path to Complete Protection

If you recognize that your current estate plan leaves you vulnerable to lawsuits, creditors, or tax inefficiency, now is the time to act. The longer you wait, the greater the risk that a creditor claim will arise and make asset protection impossible or legally questionable.

Here’s your action plan:

Week 1: Acknowledge the Gap

Recognize that estate planning and asset protection are separate and that you need both. Most families face this gap. You’re not alone, and there are proven solutions.

Week 2-3: Assess Your Exposure

Think about your professional risks, your business structure, your litigation history, and any lawsuits you might face. Be honest about your liability exposure.

Week 4: Consult with a Specialist

Don’t rely on a general estate planning attorney or a CPA alone. Consult with someone who specializes in asset protection and irrevocable trust planning for high-net-worth families. This conversation should be free or low-cost, and it should clarify whether you need comprehensive asset protection.

Week 5: Design Your Strategy

Work with your advisor to design a specific irrevocable trust structure tailored to your situation. Ensure it integrates with your existing estate plan and addresses your specific risks.

Week 6-10: Implement the Plan

Execute the trust documents, fund the trust with your assets, and ensure all paperwork is completed. Do not skip this step. An unfunded trust provides no protection.

Ongoing: Maintain the Structure

Conduct annual reviews with your advisor. Ensure tax filings are completed and the trust remains in good standing. Update the plan as your circumstances change.

The cost of inaction is clear: a single lawsuit, judgment, or creditor claim can wipe out decades of wealth building. The cost of action is modest compared to the protection you’ll gain.

We’re here to guide you through this process. Our Ultra Trust system has been tested in courts across the country, and we’ve documented the real-world outcomes. Families who implement our approach protect their wealth, minimize taxes, and preserve their legacy.

Your next step is simple: schedule a consultation to discuss your specific situation. We’ll assess your exposure, explain your options, and outline a clear path to complete protection.

—

Last Updated: January 2026

Contact us today for a free consultation!