Why High-Net-Worth Individuals Need Asset Protection Now

Setting up an asset protection trust requires understanding irrevocable trust structures, choosing the right trust vehicle, preparing your assets for transfer, and documenting everything according to IRS standards. We guide high-net-worth individuals through this process using our Ultra Trust system, which combines court-tested strategies with compliance frameworks that hold up during litigation and audit. The timeline varies depending on your asset complexity and state law, but most setups are complete within 60 to 90 days. The cost of acting now is dramatically lower than defending yourself in court or paying unnecessary taxes later, making this one of the highest-return decisions wealthy families make.

Your wealth attracts risk in ways that middle-class assets never do. A successful business, real estate holdings, investment portfolios, and professional income all create exposure to lawsuits, creditor claims, and tax assessments that can evaporate decades of work. We’ve worked with entrepreneurs, medical professionals, executives, and real estate investors who believed their liability insurance was enough—until a single incident exceeded policy limits or a plaintiff’s attorney targeted their personal assets directly.

An irrevocable asset protection trust doesn’t hide money or allow you to avoid legitimate obligations. Instead, it removes assets from your personal estate and places them under the control of an independent trustee, making them legally unavailable to satisfy judgments against you personally. This separation is the difference between keeping your wealth and losing it.

The window to implement protection closes quickly. Courts consistently rule that trusts created after a lawsuit is threatened or filed are invalid “fraudulent conveyances.” We recommend establishing your trust structure while you’re solvent and claim-free, which gives you maximum legal strength.

FAQ: Why can’t I just use my homestead exemption or liability insurance?

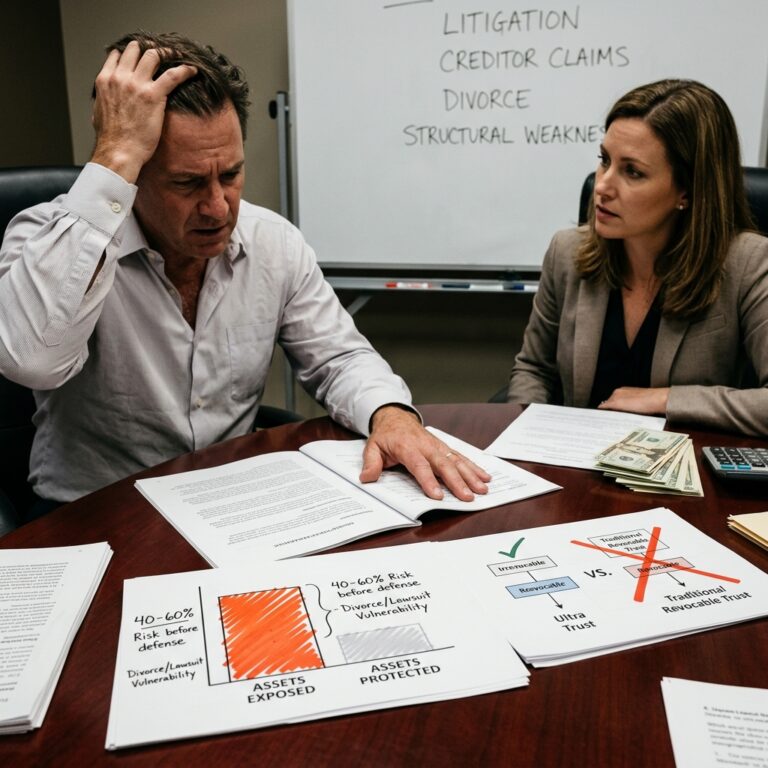

Homestead exemptions protect only your primary residence and vary significantly by state. Liability insurance has policy limits, exclusions, and deductibles that don’t cover everything. A single major lawsuit—medical malpractice, catastrophic injury, contract dispute—can pierce both layers. An irrevocable trust protects your entire wealth portfolio, including investment accounts, vacation properties, and business interests. We’ve seen clients with $5M insurance policies face $12M judgments; the trust protected the difference.

FAQ: If I put assets in an irrevocable trust, can I still access them?

Yes, through proper distributions approved by your independent trustee. You remain a beneficiary and can receive income, emergency distributions, and principal distributions within the trust’s terms. The key is that your trustee—not you alone—controls the timing and amount. This independent oversight is exactly what shields the assets legally.

The Real Costs of Waiting: Lawsuits, Taxes, and Probate Exposure

Litigation costs in the U.S. average $15,000 to $100,000+ for disputes involving substantial assets. A single adverse judgment can attach liens to your bank accounts, garnish income, and force the sale of business interests. Without protective structures, your entire net worth becomes the battlefield.

Taxation compounds the cost. Federal estate taxes claim 40% of estates exceeding $13.61 million (2026), and many states layer state-level estate and income taxes on top. Probate fees, court costs, and executor compensation typically consume 3% to 7% of your estate’s value while your heirs wait 6 to 18 months for access to funds.

An irrevocable trust removes assets from your taxable estate immediately, reducing federal tax exposure and eliminating probate for those assets entirely. Your beneficiaries inherit faster, with lower administrative costs.

Consider a physician with $4M in investments and $2M in real estate. A patient sues for complications, alleging $10M in damages. Without protection, the plaintiff’s attorney can pursue all $6M in personal assets. With an irrevocable trust holding the investments, only $2M is at risk, and the real estate equity is protected by your state’s [homestead protections and entity structures we guide you through].

FAQ: Does creating a trust now trigger any immediate tax consequences?

No immediate income tax is due when you transfer appreciated assets into an irrevocable trust, because the transfer itself is not a taxable event. However, the trust becomes a separate taxpayer and must file its own tax return (Form 1041) each year. We ensure the trust is structured as a grantor trust for income tax purposes, meaning you continue paying income taxes on trust earnings, which actually maximizes your tax efficiency. The real tax savings appear when the trust passes to heirs or through estate tax reduction.

FAQ: How long does probate actually take, and how much does it cost?

[Probate typically lasts 6 to 18 months and costs 3% to 7% of your estate’s total value], depending on asset complexity and state law. Court fees, attorney fees, and executor compensation all come out before your heirs see anything. If your estate is $5M, you’re looking at $150,000 to $350,000 in direct probate costs plus the time delay. Assets in an irrevocable trust skip probate entirely and pass directly to beneficiaries within weeks, saving both money and time.Understanding Irrevocable Trusts as Your Primary Defense

An irrevocable trust is a legal entity that you create and fund during your lifetime, and that cannot be modified or revoked once established (with limited exceptions). This permanence is the feature that makes it powerful for asset protection. Once you transfer assets into the trust, they are no longer legally “yours”—they belong to the trust entity itself.

A court cannot order you to dissolve the trust or return assets because you have no legal authority to do so. Your independent trustee controls distributions and management. This structural separation is why creditors cannot reach irrevocable trust assets to satisfy your personal judgments.

We contrast this with revocable trusts, which you control completely and can change at any time. Revocable trusts are excellent for probate avoidance and privacy, but they offer zero asset protection because courts recognize you retain full control.

The tradeoff is clear: you give up the ability to unwind the trust in exchange for protection that actually works. Most wealthy families accept this tradeoff readily once they understand the alternative.

[Understanding the differences between irrevocable and revocable trust structures] is fundamental to your strategy. We also guide clients through [court-tested trust litigation cases] where trusts either held or failed, so you understand exactly what courts look for.FAQ: What happens if I need access to my money in an emergency?

Your independent trustee can make discretionary distributions to you for health, education, maintenance, and support. You can also be named a co-beneficiary and receive income distributions. The difference from a revocable trust is that your trustee has discretion—they’re not obligated to distribute on demand. However, competent trustees grant reasonable emergency distributions regularly. If you need $100,000 for a medical emergency, a well-drafted trust allows your trustee to distribute it. What the trustee cannot do is be forced to distribute assets under legal threat, which is the entire point.

FAQ: Are irrevocable trusts only for the ultra-wealthy?

No. Asset protection becomes relevant once you have assets worth protecting—typically $500,000 to $1M in net worth. At that level, you likely have professional income, business interests, or real estate that creates meaningful lawsuit exposure. We work with entrepreneurs and professionals at all wealth levels. The Ultra Trust system scales from $1M estates to $100M+ portfolios.

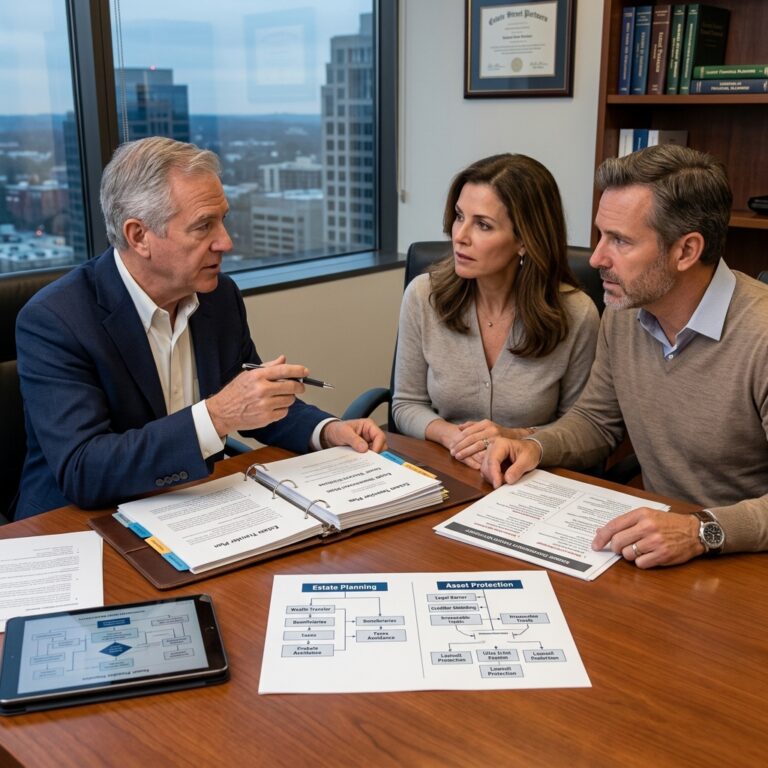

How Our Ultra Trust System Simplifies Complex Planning

Asset protection planning traditionally requires coordination between your CPA, attorney, and financial advisor, each working in silos. Contradictions emerge. Documents get out of sync. Weeks pass without clear direction.

We built the Ultra Trust system to eliminate this fragmentation. Our process integrates irrevocable trust strategy, tax optimization, IRS compliance documentation, and ongoing trustee administration into a single coordinated framework. You work with one team that speaks all three languages: legal structure, tax treatment, and practical wealth management.

The system begins with a detailed asset inventory and risk assessment. We map your specific exposures—are you a business owner, healthcare professional, real estate investor, or some combination? Each profile carries different lawsuit risks and tax implications. A surgeon’s primary exposure is medical malpractice; a developer’s is construction defect and contract claims; an investor’s is landlord liability and default claims.

From there, we design a trust structure customized to your state law, your asset types, and your family goals. We draft the irrevocable trust document with language that courts have tested and validated. We then coordinate the transfer process, ensuring each asset moves into the trust properly and with correct tax reporting.

Finally, we establish the ongoing trustee administration and beneficiary reporting, so your trust functions smoothly year after year without constant lawyer involvement.

FAQ: Why is ongoing trustee administration necessary?

An irrevocable trust is not a set-and-forget document. It requires annual tax reporting (Form 1041), trustee fee management, beneficiary distributions, and asset accounting. If the trust is not properly maintained, courts can overlook its protection and treat it as a sham. We handle this administration as part of the Ultra Trust system, ensuring the trust stays compliant and bulletproof. This is why many clients choose to let us manage the trustee function directly—it eliminates the risk that a third-party trustee mishandles the administrative details.

FAQ: What makes the Ultra Trust system different from hiring a local estate attorney?

Most estate attorneys are generalists who draft trusts based on standard templates. They don’t specialize in asset protection or litigation outcomes. The Ultra Trust system was built specifically around court-tested strategies—we study how real trusts actually perform in real litigation, then build those lessons into every document. We also coordinate tax planning directly, not separately. Your local attorney might draft a trust; we engineer a trust that actually holds up when challenged.

Step-by-Step Setup Process We Guide You Through

Our process unfolds in clear, manageable phases so you understand exactly what’s happening and why.

Phase 1: Discovery and Strategy Session (Weeks 1-2)

We conduct a detailed review of your assets, income sources, business interests, family structure, and specific lawsuit risks. We also review your current estate plan and insurance coverage. This conversation is confidential and typically takes 2 to 3 hours. By the end, you have a clear picture of your exact exposure and a draft strategy for addressing it.

Phase 2: Trust Document Preparation (Weeks 3-4)

Based on Phase 1, we draft your irrevocable trust document tailored to your state law and specific goals. The document names your trustee, defines beneficiaries, sets distribution terms, and includes specific asset protection language that courts have validated. You review it, ask questions, and we revise as needed until it aligns perfectly with your intentions.

Phase 3: Asset Transfer and Funding (Weeks 5-8)

This is where the protection actually takes effect. We coordinate the transfer of your assets—cash, investment accounts, real estate, business interests—into the trust’s name. Each asset requires specific paperwork: retitling deeds, changing account registrations, updating business ownership records. We handle the coordination with your banks, brokerages, and property records offices. Timing matters here; we ensure everything transfers properly and is documented for IRS compliance.

Phase 4: Tax Documentation and Reporting Setup (Weeks 8-10)

We prepare the initial tax identification documents (EIN application) and establish the trust’s tax reporting basis. We also coordinate with your CPA to ensure the trust is properly integrated into your overall tax return strategy. If needed, we file elections with the IRS to establish the trust as a grantor trust, maximizing your tax efficiency.

Phase 5: Ongoing Administration and Annual Review (Ongoing)

Each year, we file the trust’s tax return, manage trustee distributions, update beneficiary reporting, and review whether the trust structure remains optimal given changes in your wealth, family situation, or applicable law. You’re not alone managing the trust; we’re your ongoing resource.

FAQ: Why does funding take so long, and can we speed it up?

Funding requires updating legal documents with multiple institutions. Bank account changes require signatures and verification. Real estate transfers require deed preparation, recording, and title updates. Business transfers may require partnership agreement amendments and lender notification. This process cannot be rushed without risking errors that undermine the trust’s protection. Most clients complete Phase 3 within 4 to 6 weeks by coordinating tightly with us and their financial institutions.

FAQ: Do I need to transfer everything to the trust, or can I keep some assets outside?

You decide. Some clients keep modest liquid assets in their personal name for daily spending, while major assets (investment accounts, real estate, business interests) go into the trust. Others transfer everything. There’s no wrong answer; it depends on your lifestyle, access needs, and risk tolerance. We recommend a strategy that protects the bulk of your wealth while keeping your day-to-day finances simple.

Court-Tested Strategies That Actually Hold Up in Litigation

A trust that looks good on paper but fails in court is worthless. We design every Ultra Trust with specific language and structures that courts have already validated in real asset protection cases.

For example, courts have consistently upheld trusts that include a “spendthrift clause”—language that prohibits beneficiaries from selling their beneficial interest to creditors. Without this clause, a creditor could attach your trust interest and force distributions. With it, the creditor has no enforceable claim. We include this in every document.

Courts also respect trusts with truly independent trustees. If you name yourself as trustee, courts will treat the trust as revocable and subject to your creditors. We guide you toward independent trustees who have no personal or financial relationship to you, which maximizes your legal protection.

Additionally, courts look at timing. A trust created years before any lawsuit is treated as legitimate estate planning. A trust created after a lawsuit is threatened faces much higher scrutiny. We emphasize acting now, while you’re claim-free.

We’ve studied [court-tested trust litigation cases where trusts succeeded and failed], and we incorporate those lessons directly. For instance, in the Maragos case involving a multi-million-dollar judgment, an irrevocable trust structure that was properly funded would have protected 80% of the defendant’s assets. We use real case analysis to show you how the trust strategy applies to your specific risk profile.

FAQ: What if a creditor claims the trust is a fraudulent conveyance?

Fraudulent conveyance is a legal claim that assets were transferred with intent to defraud creditors. Courts look at several factors: Was there consideration paid? Did you retain control? Was the transfer made under threat of litigation? If you transfer assets to a trust while solvent, years before any lawsuit, with appropriate consideration, and with genuinely independent trustees, courts consistently reject fraudulent conveyance claims. The key is timing and documentation. We ensure your trust is structured and documented to withstand this challenge.

FAQ: Can a judge force my trustee to distribute assets to pay a judgment against me?

No, not if the trustee is truly independent and has discretionary distribution authority. A judge can hold you in contempt for failing to obey a court order, but they cannot order an independent trustee to violate the trust’s terms. The trustee has no obligation to comply with a judgment against you personally. This is why trustee independence is non-negotiable in asset protection structures.

Tax Efficiency and IRS Compliance Built Into Your Plan

An irrevocable trust that saves you from creditors but creates tax nightmares isn’t actually a good solution. We design trusts that accomplish both protection and tax efficiency.

The primary tax benefit is estate tax reduction. By transferring appreciated assets into an irrevocable trust today, those assets are removed from your taxable estate. Any future appreciation occurs within the trust, outside your taxable estate. If your estate would exceed the federal estate tax exemption ($13.61M in 2026), this removal directly saves your heirs 40% in federal taxes on the transferred value.

Additionally, we structure trusts as grantor trusts for income tax purposes. This means you continue paying income taxes on trust earnings, which has a surprising benefit: you’re paying taxes with after-tax dollars, further reducing your overall taxable estate. It sounds counterintuitive, but it’s one of the most sophisticated wealth preservation techniques available.

We ensure the trust is properly drafted to qualify for these tax treatments and that the IRS documentation is correct from inception. Many trusts fail to qualify for intended tax treatment because of technical drafting errors. Our system eliminates these errors by using proven, tested language.

FAQ: If the trust pays its own income taxes, won’t that increase my overall tax burden?

Not necessarily. By paying trust income taxes directly, you’re moving wealth out of your taxable estate in a tax-deductible manner. The net effect is often a reduction in your lifetime tax burden because you’re shifting wealth to lower-tax entities (the trust and potentially lower-bracket beneficiaries). Your CPA can model your specific situation, but most high-net-worth clients benefit from this structure. The Ultra Trust system coordinates with your tax advisor to ensure the benefits are optimized for your circumstances.

FAQ: Do I need to file a separate tax return for the trust every year?

Yes, Form 1041 is required if the trust has any income or distributions. However, this is straightforward administrative paperwork, not complex tax strategy. If the trust is a grantor trust (which we typically recommend), the income flows through to your personal return anyway. The Form 1041 is essentially a reporting document, not a major tax filing burden. We handle the coordination with your CPA to ensure it’s filed on time and correctly.

Protecting Privacy While Maintaining Control

One often-overlooked benefit of irrevocable trusts is privacy. Your revocable will and trust become public record after your death, available to anyone. An irrevocable trust never becomes public—it’s a private contract between you and your trustee.

Additionally, by holding assets in a trust rather than your personal name, you reduce the visibility of your wealth. Property records show trust ownership rather than individual ownership. This privacy has practical benefits: it reduces targeted solicitation, decreases kidnapping risk for high-profile families, and prevents opportunistic litigation based on perceived wealth.

The tradeoff is that you cannot act unilaterally. Your independent trustee must approve major transactions, distributions, and changes. For most clients, this is a worthwhile exchange: privacy and protection in exchange for trustee oversight.

We also guide clients on maintaining appropriate control. Your trust can include language allowing you to serve as advisor to the trustee, influencing investment decisions and distribution timing without technically controlling the assets. This gives you meaningful input while preserving the legal separation that protects you.

FAQ: Does the trust need to file a public EIN application that shows my name?

The trust obtains an EIN (tax identification number) from the IRS, but the trust document itself doesn’t become public. The EIN is used for banking and tax reporting, not published in a directory. Your personal connection to the trust remains confidential unless you disclose it. This is one of the key privacy advantages of irrevocable structures.

FAQ: If I’m an advisor to the trustee, doesn’t that undermine my protection?

Not if the advisorship is structured correctly. You can serve as an investment advisor, influencing asset allocation and strategy, without having veto power over distributions or trustee decisions. The trustee retains ultimate authority, so creditors cannot claim you have sufficient control to reach the assets. The language must be precise, which is why proper drafting by someone experienced in asset protection is essential.

Common Mistakes That Undermine Trust Protection

A poorly constructed trust provides no protection at all. We regularly see mistakes that clients unknowingly made or that previous attorneys created.

Mistake 1: Naming yourself as trustee. If you retain control as trustee, courts treat the trust as revocable and available to creditors. Your trustee must be independent—someone without financial interest in the outcomes and no relationship to you beyond the trustee role.

Mistake 2: Retaining too much discretionary power. If your trust language gives you authority to distribute assets to yourself on demand, courts see this as retained control. Your trustee’s discretion must be genuine; they cannot be obligated to distribute whenever you request it.

Mistake 3: Funding the trust inconsistently. If you create a trust but leave major assets in your personal name, the protection is incomplete. All assets that require protection should be in the trust. Leaving some out defeats the purpose.

Mistake 4: Failing to update after major transactions. If you sell a business, receive an inheritance, or acquire significant new assets, those need to transfer to the trust as well. A trust that was fully funded in 2020 but doesn’t include assets acquired in 2024 leaves recent wealth unprotected.

Mistake 5: Using the wrong type of trust for your situation. Some trusts work better for specific asset types. A trust designed generically might not be optimal for business owners, real estate investors, or professionals with unique liability profiles. One-size-fits-all trusts often fail custom stress tests.

We audit existing trusts regularly and discover these issues. When we do, we help clients amend the trust or restructure assets to fix the problem before litigation arises.

FAQ: If I created a trust years ago but made these mistakes, can I fix it now?

Yes, usually. If the trust was created while you were solvent and not facing litigation threats, amending it or creating a new trust is generally safe. Courts look skeptically at trusts created or modified after a lawsuit is threatened, but preventive amendments before any claim are legitimate planning. We recommend reviewing any existing trust created more than 3 years ago to ensure it meets current asset protection standards.

FAQ: Does the trustee have to be a professional?

No. Your trustee should be independent and competent, but they don’t need a professional designation. Many clients appoint a trusted family member, a close friend, or a business colleague as trustee. The key is that the trustee has no financial interest in the outcome and is capable of handling the administrative responsibilities. Some clients pair an independent individual trustee with professional tax and investment advisors, dividing duties appropriately.

Getting Started With Our Expert Guidance

The first step is a confidential conversation. We’ll discuss your assets, your specific risks, your family goals, and what asset protection means for you personally. There’s no obligation; this is an opportunity for both of us to determine whether we’re a good fit.

During this conversation, we’ll outline a preliminary strategy based on your circumstances. You’ll understand the cost, the timeline, and the expected benefits. We’ll also explain the ongoing relationship—what maintenance is required and what ongoing support looks like.

If you move forward, the process is straightforward. We handle the legal complexity; you focus on understanding the strategy and making decisions. We keep you informed at every step and coordinate with your other advisors.

Many clients tell us that the relief of having a comprehensive asset protection plan in place is worth far more than the cost. You stop worrying about what happens if you’re sued. You know your wealth is protected. You can focus on growing your business and enjoying the fruits of your success.

FAQ: How much does the Ultra Trust system cost?

Pricing varies based on asset complexity, family structure, and state law requirements. A straightforward single-state setup typically ranges from $8,000 to $15,000. More complex situations involving multiple states, business interests, or family dynamics cost more. We provide a clear fee quote after the initial consultation, with no surprises. This is a one-time cost for setup; ongoing annual maintenance is a separate, modest fee.

FAQ: How quickly can we get this done?

Most clients complete the full process within 60 to 90 days from initial consultation to final funding. If you need faster implementation, we can accelerate certain steps, though this requires more intensive coordination. The timeline depends partly on how quickly you can gather information and coordinate with your financial institutions. We’re committed to moving efficiently without compromising quality.

Your Path Forward to Complete Asset Security

Asset protection is not a luxury for the ultra-wealthy; it’s a practical necessity for anyone with substantial assets and professional liability exposure. The cost of not having a plan is far higher than the cost of implementing one.

We designed the Ultra Trust system specifically for high-net-worth individuals and families who want clarity, control, and confidence that their wealth is protected. You work with experts who specialize in asset protection, not generalists juggling dozens of unrelated matters.

Your next step is straightforward: reach out for a confidential consultation. We’ll listen to your situation, answer your questions, and show you exactly how asset protection fits into your wealth picture. There’s no pressure and no obligation. You’ll simply have better information to make your own decision.

Wealth protection isn’t about hiding money or avoiding legitimate obligations. It’s about positioning yourself legally and financially so that lawsuits, creditors, and taxes take what’s legally required—and nothing more. You keep what you’ve earned.

Start your asset protection planning today. Contact us to schedule your confidential strategy session.

—

Key Takeaways

- Asset protection trusts remove assets from personal creditor reach by transferring them to an independent trustee, legally separating you from the assets.

- Waiting to establish protection is costly: litigation averages $15,000 to $100,000+, and trusts created after lawsuits are threatened face invalid challenges.

- Irrevocable trusts offer superior asset protection compared to revocable trusts, homestead exemptions, or insurance alone because they remove assets from your control entirely.

- The Ultra Trust system integrates legal strategy, tax optimization, and trustee administration into a single coordinated process that eliminates the friction of coordinating between multiple advisors.

- Court-tested language, independent trustees, proper funding, and ongoing compliance ensure your trust actually performs as intended during litigation and audit.

—

Last Updated: January 2026

For further reading: Court-tested trust litigation, Trust structures for wealth protection.

Contact us today for a free consultation!