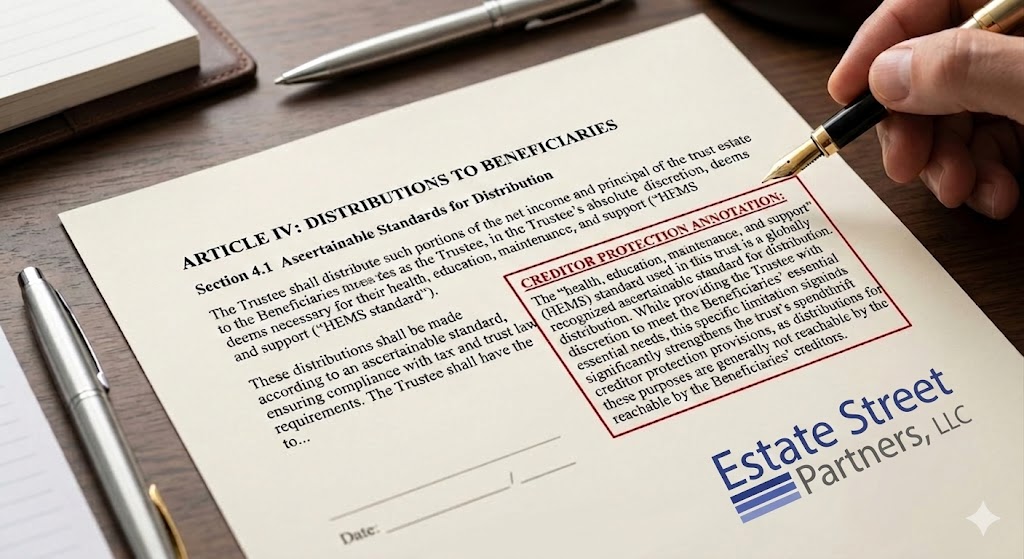

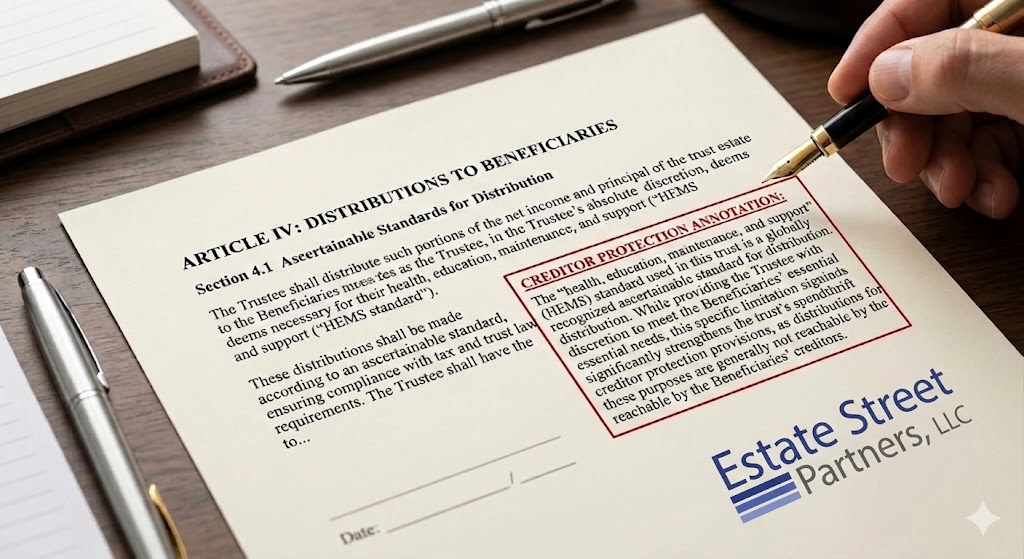

An ascertainable standard in a trust is a legal provision that limits a trustee’s discretion to make distributions to beneficiaries to specific, defined purposes — typically related to health, education, maintenance, or support (commonly called HEMS). This phrase — “health, education, maintenance, and support” — appears in the Internal Revenue Code and in trust law across the country as the defining example of an ascertainable standard. When a trust contains an ascertainable standard, the trustee can only distribute assets for those specific purposes. This seemingly technical drafting choice has enormous consequences for estate taxes, creditor protection, and the overall effectiveness of an asset protection trust — consequences that most trust beneficiaries never understand until a creditor attacks.

Why Ascertainable Standards Exist

The ascertainable standard concept originated primarily from federal estate and gift tax law. Under IRC Section 2041, if a beneficiary has a “general power of appointment” over trust assets — the power to demand distribution for any reason — those trust assets are included in the beneficiary’s taxable estate when they die. If that same power is limited to an ascertainable standard (health, education, maintenance, support), the power is not a “general” power, and the assets are not included in the beneficiary’s taxable estate.

This is the core estate tax rationale for ascertainable standards. But the impact on creditor protection is equally significant and far less commonly understood.

The Creditor Protection Dimension

Here is the core tension: ascertainable standards create a legally enforceable right to distributions for qualifying purposes. If a beneficiary needs money for medical care, and the trust provides for distributions for “health,” the beneficiary has a legally enforceable right to demand that distribution. A right to demand distribution is something that a creditor can potentially attach.

Fully discretionary trusts, by contrast, give the trustee complete and unreviewable discretion to distribute — or not distribute — with no obligation to distribute for any particular reason. Because the beneficiary has no legally enforceable right to any distribution, a creditor has nothing to attach.

This is why the most creditor-resistant irrevocable trusts use fully discretionary distribution standards, not ascertainable standards. When the trustee can say “I have complete discretion and I’m choosing not to distribute today,” the beneficiary’s creditor is left with nothing to seize.

HEMS vs. Full Discretion: The Asset Protection Trade-Off

The choice between HEMS (ascertainable standard) and full discretion is one of the most consequential structural decisions in trust drafting, and it reflects a genuine tension between estate tax planning and asset protection.

HEMS Distribution Standard (Ascertainable):

- Estate tax benefit: Assets not included in beneficiary’s taxable estate

- Creditor exposure: Beneficiary can be compelled to demand distributions for qualifying purposes; creditor can potentially attach that right

- Control: Predictable, measurable standard that beneficiaries can rely on

- Court oversight: Courts can compel distribution if qualifying needs are not met

Fully Discretionary Distribution Standard:

- Estate tax treatment: Assets may be included in beneficiary’s estate if beneficiary is also trustee (separate issue)

- Creditor protection: Maximum protection — no enforceable distribution right for creditors to attach

- Control: Entirely dependent on trustee’s judgment — less predictability for beneficiaries

- Court oversight: Courts give maximum deference to trustee’s discretion

The strongest asset protection trusts use fully discretionary standards. The trade-off is that beneficiaries have less certainty about receiving distributions, which can be uncomfortable for beneficiaries who need predictable access.

How Creditors Attack Ascertainable Standard Trusts

When a creditor knows that a judgment debtor is a beneficiary of a trust with an ascertainable standard, they can attempt to:

Force the beneficiary to demand distributions. If the trust requires distributions upon demand for HEMS purposes, and the beneficiary has qualifying HEMS needs, a court may compel the beneficiary to demand a distribution — which then becomes an asset the creditor can seize.

Attach the right to future distributions. Some courts have held that a beneficiary’s right to demand HEMS distributions is a property right that can be attached by a creditor — meaning the creditor gets the next HEMS distribution rather than the beneficiary.

Petition the court to compel trustee distributions. If the trustee has an obligation to distribute for HEMS purposes and is refusing, a creditor can petition the court to compel that distribution on the beneficiary’s behalf.

None of these attacks work against a fully discretionary trust. If the trustee has no obligation to distribute, there is no right to attach, no distribution to compel, and no predictable stream of assets for a creditor to intercept.

Historical Context: The Case Law Background

The asset protection significance of ascertainable standards versus full discretion has been litigated extensively. The leading scholarly analysis — including the research that UltraTrust has built upon — shows that trusts surviving creditor attacks in contested litigation consistently share a structural pattern: specific distribution standards that the trustee must apply, clear guidelines, explicit exclusions for creditor claims, and documented trustee decision-making.

Conversely, trusts that fail tend to be those where the distribution standard is not clearly defined, where the trustee and beneficiary are the same person, or where distributions were made on a pattern that suggested the beneficiary effectively controlled the trust.

The Trustee’s Role Under an Ascertainable Standard

When a trust contains an ascertainable standard, the trustee bears significant responsibility for applying it correctly. This involves:

Determining whether a requested distribution qualifies. A distribution for a luxury vacation does not qualify under “health, education, maintenance, and support.” A distribution for medical treatment that insurance won’t cover does qualify under “health.” The trustee must make these determinations in good faith.

Documenting distribution decisions. Every distribution decision — whether made or declined — should be documented in writing. This creates a record of proper trust administration that can be presented in court if the trust is ever challenged.

Maintaining independence from the beneficiary. An ascertainable standard trustee must not simply rubber-stamp every distribution request. Genuine analysis of whether the request qualifies is required. Automatic approval of every request undermines both the protective purpose and the administrative legitimacy of the trust.

The Grantor as Trustee Problem

One of the most common structural errors in irrevocable trusts is allowing the grantor — the person who created and funded the trust — to also serve as trustee. This creates two serious problems under ascertainable standard analysis:

Estate tax inclusion. Under IRC Section 2036, if the grantor retains the power to distribute trust income or principal for the grantor’s own benefit — including under an ascertainable standard — the trust assets may be included in the grantor’s taxable estate. The estate tax protection that the irrevocable structure was designed to achieve is lost.

Creditor exposure. If the grantor is also a beneficiary of a trust subject to an ascertainable standard, and also serves as trustee with power to distribute to themselves, a court may find that the grantor effectively controls the assets — treating them as still owned by the grantor for creditor purposes.

The solution is clear: the grantor should never serve as trustee of an irrevocable trust from which they are entitled to receive distributions. An independent, professional trustee is essential for both estate tax and asset protection purposes.

When Ascertainable Standards Still Make Sense

Despite the asset protection advantages of fully discretionary trusts, there are situations where ascertainable standards remain appropriate:

For third-party beneficiaries (not the grantor). When an irrevocable trust is created for the grantor’s children or grandchildren — not the grantor — an ascertainable standard limits what the trustee can distribute while still providing meaningful estate tax benefits. The children are not being sued for the grantor’s debts; they have their own potential creditor issues, which may warrant separate planning.

When beneficiary certainty matters. If the beneficiary genuinely needs reliable access to trust assets for specific qualifying purposes — ongoing medical treatment, education funding — the certainty of an ascertainable standard may outweigh the pure asset protection benefit of full discretion.

In combination with other protections. A trust with an ascertainable standard, combined with a strong spendthrift clause and a truly independent trustee, provides meaningful protection even if it is not maximally protection-oriented.

Drafting the Standard Correctly

For trusts where asset protection is the primary goal, the distribution standard must be drafted with precision. The most protective language:

Gives the trustee complete and unreviewable discretion to distribute or withhold without being required to justify the decision to any beneficiary or court. Explicitly states that distributions shall not be made to satisfy creditors of any beneficiary. Includes a clear anti-alienation provision preventing any beneficiary from assigning their interest. Specifies that the trustee’s decision not to distribute shall not create any right of action in any beneficiary. Requires any trustee decision to be made in writing and maintained in trust records.

This level of specificity is not found in online trust templates. It requires drafting by an attorney who understands both the estate tax implications of ascertainable standards and the creditor protection implications of distribution discretion.

Frequently Asked Questions

What does HEMS stand for in a trust? HEMS stands for health, education, maintenance, and support. It is the standard example of an ascertainable standard under the Internal Revenue Code and is commonly used in trust distribution provisions.

Is a HEMS trust better or worse for asset protection than a discretionary trust? Worse. A fully discretionary trust — where the trustee has complete and unreviewable discretion to distribute or not — provides stronger asset protection than a HEMS trust, because beneficiaries have no legally enforceable right to demand distributions.

Can a creditor force a trustee to distribute under a HEMS standard? In some states, yes. If the beneficiary has qualifying HEMS needs and the trust requires distributions for those needs, a creditor may be able to compel a distribution. This is the primary creditor vulnerability of ascertainable standard trusts.

Should my irrevocable trust use HEMS or full discretion? For maximum asset protection, full discretion is preferable. For estate tax planning for trusts benefiting your children or grandchildren, HEMS may still be appropriate depending on your goals.

Conclusion

An ascertainable standard in a trust is far more than a technicality — it is a structural choice that determines both the estate tax treatment of trust assets and the degree of creditor protection those assets receive. For grantors seeking maximum protection from creditor attack, a fully discretionary trust administered by a genuinely independent trustee provides the strongest protection. For beneficiary trusts where estate tax planning matters, an ascertainable standard may be appropriate — but it must be paired with a strong spendthrift clause and independent trustee to minimize creditor exposure. Understanding this distinction is essential for anyone building a serious asset protection strategy.

Helpful resources: Readers often continue with Asset Protection Trust, Revocable vs Irrevocable Trust, and official IRS estate and gift tax guidance when comparing planning options.

What often changes the answer

After reviewing What Is an Ascertainable Standard in a Trust and Why It Matters?, many people want a clearer sense of how the answer changes once real life timing, funding, and control are added to the discussion.

What usually shapes the next step

- Timing matters because planning choices usually become narrower once a problem is already close.

- Control matters because the answer often depends on how much access or authority the owner wants to keep.

- Funding matters because a trust or entity has to be set up and maintained correctly to matter.

Where readers often continue

A practical next reading path is Asset Protection Trust, Irrevocable Trust, and How It Works. When the question turns from reading to implementation, many readers move from these guides to a direct planning conversation.