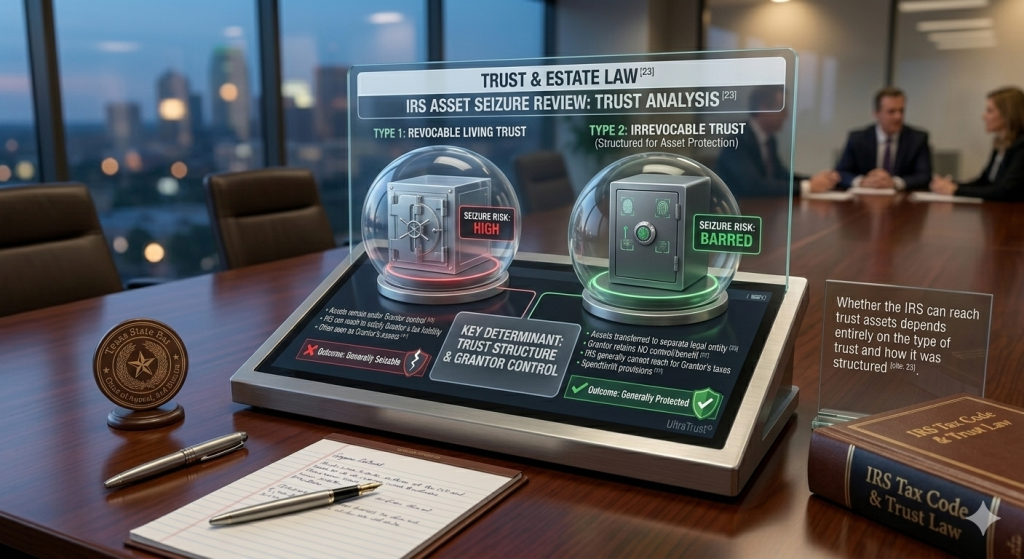

- A properly structured irrevocable trust can protect assets from IRS collection — but only when funded before any tax liability exists, with no retained grantor interest and a genuinely independent trustee.

- The IRS has broader collection powers than civil creditors — it can file liens and issue levies without a court judgment — but it cannot seize assets the taxpayer does not legally own.

- Retained interest is the most common failure point: if you live in a trust-held property, receive distributions on demand, or serve as your own trustee, the IRS will argue those assets are still yours.

- Distributions received from the trust become personal property immediately and are fully reachable by the IRS the moment they leave the trust.

- The UltraTrust® system eliminates retained interest, installs a genuinely independent trustee, and maintains full IRS reporting compliance — the three non-negotiable requirements for legally defensible IRS protection.

A properly structured irrevocable trust can protect assets from IRS collection actions — but not completely, not automatically, and not in every circumstance. The IRS holds collection powers that exceed those of most civil judgment creditors: it can file federal tax liens, issue levies, and seize assets without first obtaining a court judgment under the Internal Revenue Code. Despite these broad powers, the IRS remains bound by the fundamental legal reality of ownership. If assets were legitimately and irrevocably transferred to a properly structured trust — with no retained grantor interest, genuine independent trustee control, and the transfer occurring before any tax liability existed — the IRS must treat those assets as belonging to the trust, not the individual taxpayer. The IRS’s central question in every trust collection case is the same: did the taxpayer actually give up ownership and control? When the answer is yes, and the transfer was not a fraudulent conveyance, those assets are generally beyond the IRS’s standard collection reach. Estate Street Partners structures every UltraTrust® engagement to answer that question with an unambiguous yes — backed by contemporaneous documentation that withstands IRS audit scrutiny.

How Does the IRS Approach Irrevocable Trusts in Tax Collection?

The IRS is not a typical creditor. It operates under the Internal Revenue Code — a separate body of federal law that gives it collection powers most civil judgment creditors do not possess. The IRS can file a federal tax lien under IRC § 6321 that attaches to all property and rights to property belonging to the taxpayer. It can issue levies under IRC § 6331 and seize assets without a court judgment. It can garnish wages, freeze bank accounts, and pursue collection across state lines without the procedural limitations that bind civil creditors.

Beyond standard collection tools, the IRS can also pursue alter ego and nominee theories against trusts it believes are shams. Under an alter ego theory, the IRS argues the trust is not a genuinely separate legal entity — it is simply the taxpayer operating under a different name. Under a nominee theory, the IRS argues the trust holds assets that are functionally owned by the taxpayer even though legal title was transferred. If either theory succeeds, the IRS treats the trust assets as the taxpayer’s personal property and proceeds with standard collection.

Despite all of these powers, the IRS cannot reach assets that were genuinely and irrevocably transferred to a separate legal entity before any tax liability arose. The legal principle is straightforward: you cannot be compelled to pay debts from assets you do not own. When the trust is real — independently administered, properly funded, with no retained grantor access — the IRS must respect the transfer.

❓ Q: Can the IRS seize assets inside an irrevocable trust to pay the grantor’s income taxes?

A: Generally no — provided the grantor retained no beneficial interest in the trust assets and the transfer was not a fraudulent conveyance. The IRS’s federal tax lien under IRC § 6321 attaches to all property and rights to property belonging to the taxpayer. If assets were genuinely transferred to an irrevocable trust before any tax liability existed, with an independent trustee and no retained grantor interest, those assets belong to the trust — not the taxpayer. The IRS must treat them accordingly. However, the specific facts of each case determine the outcome. If the grantor retained any right to income, principal, or control — or if the transfer occurred after a tax liability arose — the IRS will argue those assets are still functionally the taxpayer’s and pursue collection aggressively. Estate Street Partners structures every UltraTrust® to eliminate each of these vulnerabilities by design, not as an afterthought.

❓ Q: What is the difference between the IRS’s alter ego theory and a nominee theory against a trust?

A: The IRS uses both theories to pierce trust structures it believes are shams. Under the alter ego theory, the IRS argues the trust and the grantor are legally indistinguishable — the grantor controls the trust completely, uses trust assets as personal property, and the trust exists solely to create the appearance of a separate entity. Under the nominee theory, the IRS argues the trust holds assets as a nominee — a mere title holder — for the grantor, who retains all the functional benefits of ownership. Both theories, if accepted by a court, allow the IRS to treat trust assets as the grantor’s personal property for collection purposes. The UltraTrust® system defeats both theories through the same mechanism: genuine independent trustee administration with documented decision-making, no grantor access to trust assets, and a complete contemporaneous record showing the transfer was a real relinquishment of ownership — not a paper arrangement designed to deceive.

What Retained Interests Cause an Irrevocable Trust to Fail Against the IRS?

Retained interest is the single most common reason an irrevocable trust fails to protect assets from IRS collection. Courts and the IRS both examine what the grantor actually gave up — and what they kept. Four categories of retained interest consistently undermine trust protection:

The power to revoke or amend. If the grantor retains any power that effectively allows reclaiming trust assets — even if the document is labeled “irrevocable” — the IRS and courts treat the assets as still belonging to the grantor. Under IRC § 2038, retained amendment or revocation powers cause the assets to be included in the taxable estate for the same reason they create IRS collection exposure during life.

Beneficial enjoyment of the assets. If the grantor continues to live in a home held by the trust, uses trust property for personal purposes, or receives distributions effectively on demand, the IRS treats those assets as constructively belonging to the grantor. IRC § 2036 pulls assets back into the taxable estate — and into IRS collection reach — when the grantor retains the right to possession or enjoyment of transferred property.

Control over distributions. A grantor who serves as their own trustee with unlimited discretionary power to distribute trust assets to themselves has not genuinely relinquished control. The IRS will characterize the trust as a sham and treat the assets as personally owned. This is why genuine independent trustee authority — with documented discretionary analysis, not rubber-stamp approval of grantor requests — is the structural cornerstone of every UltraTrust® engagement.

Retained income rights. Some trust structures allow the grantor to receive income while claiming principal is protected from creditors. Whether the principal is actually protected from the IRS depends on the specific structure and applicable state law. For maximum IRS protection, the safest design retains absolutely nothing — no right to income, no right to principal, and no ability to direct the trustee.

❓ Q: What happens if I live in a house that is owned by my irrevocable trust?

A: If you continue to occupy a home that has been transferred to an irrevocable trust — without paying fair market rent to the trust — the IRS will likely argue that you retained a beneficial interest in the property under IRC § 2036. This retained life estate causes the property to be included in your taxable estate for estate tax purposes and makes the property potentially reachable by the IRS for collection purposes during your lifetime. The IRS treats your continued occupancy as evidence that you never genuinely relinquished ownership — making the transfer vulnerable to fraudulent conveyance challenge or alter ego characterization. Estate Street Partners addresses this risk in every UltraTrust® real property transfer by structuring the arrangement so the grantor either pays documented fair market rent, vacates the property, or the property is held for the benefit of family members without any retained grantor occupancy rights.

❓ Q: If I am the trustee of my own irrevocable trust, can the IRS reach the trust assets?

A: Yes — this is one of the most dangerous structural mistakes in irrevocable trust planning. A grantor who serves as their own trustee with discretionary power to distribute assets to themselves has not genuinely relinquished control in the eyes of the IRS or the courts. The IRS will characterize the arrangement as a nominee structure — the trust holds the assets in name only, while the grantor retains all functional control — and proceed to levy on the trust assets as if they were personal property. Courts have consistently supported this position when the grantor-trustee had unrestricted distribution authority. The UltraTrust® system requires a genuinely independent professional trustee as a non-negotiable structural element. The trustee must have no familial or financial relationship with the grantor, must exercise genuine fiduciary judgment documented in writing, and must not distribute assets simply because the grantor requests it.

What Can the IRS Still Reach Even in a Properly Structured Irrevocable Trust?

Even a perfectly structured irrevocable trust does not eliminate every avenue of IRS collection. Four specific vulnerabilities remain regardless of trust quality:

Income distributions received by the grantor. The moment a trust distribution reaches the grantor’s personal account, it becomes the grantor’s personal property — immediately reachable by a federal tax lien. The trust protects assets held inside it. It provides no protection for assets that flow out of it to a taxpayer with an outstanding IRS liability. During periods of active IRS collection, Estate Street Partners coordinates with clients and independent trustees to minimize distributions and document the trustee’s independent decision-making regarding distribution timing.

Fraudulent transfer claims on post-liability transfers. If assets were transferred to an irrevocable trust after a tax liability arose — or after the IRS had issued an audit notice, assessment, or deficiency letter — the IRS can bring a fraudulent transfer action to unwind the transfer. The IRS has a longer look-back window than most civil creditors and is aggressive in pursuing these claims. This is the decisive argument for funding a trust before any tax issues emerge, not in response to them.

Federal tax liens on after-acquired assets. A federal tax lien under IRC § 6321 attaches to all property and rights to property the taxpayer owns at the time the lien is filed — and to property acquired afterward. Assets properly transferred to an irrevocable trust before the lien arose are generally protected. Every asset acquired and held in personal name after the lien is filed is immediately encumbered.

Grantor trust income tax liability. Many irrevocable trusts are structured as grantor trusts for income tax purposes — meaning the grantor continues to pay income tax on trust earnings even though they no longer own the assets. This is typically a feature, not a defect: the grantor’s tax payments effectively constitute additional tax-free gifts to the trust, allowing trust assets to grow without income tax diminishment. However, this arrangement creates a specific IRS exposure: if the trust generates income the grantor is obligated to pay taxes on but cannot access to make those payments, the IRS may levy on trust assets to satisfy the resulting income tax liability.

❓ Q: What is grantor trust status and does it create IRS collection exposure?

A: Grantor trust status is an income tax classification under IRC §§ 671–679 under which an irrevocable trust is treated as owned by the grantor for income tax purposes — even though it is irrevocable for asset protection and estate tax purposes. The grantor reports and pays income tax on all trust income on their personal return, even though the assets legally belong to the trust. This is intentional in sophisticated planning: it allows trust assets to grow income-tax-free at the trust level, effectively passing additional wealth to trust beneficiaries without gift tax consequence. The IRS exposure this creates is specific and limited: if the trust generates taxable income and the grantor cannot pay the resulting income tax, the IRS may argue it can levy on trust assets to satisfy the income tax obligation that the trust’s own income generated. Estate Street Partners structures UltraTrust® grantor trust provisions carefully to manage this exposure while preserving the income tax efficiency benefits.

❓ Q: Can the IRS pursue criminal charges related to an irrevocable trust?

A: Yes — if the trust is used to hide assets, conceal income, or evade tax reporting obligations rather than to legitimately restructure ownership. An irrevocable trust used for genuine asset protection planning involves complete transparency: all trust income is reported, all required IRS forms are filed, and the trust’s existence is never concealed from the IRS. A trust used to hide assets or evade taxes is not asset protection — it is tax evasion, which carries criminal penalties under IRC § 7201 including fines and imprisonment. The distinction is clear in practice: legitimate irrevocable trust planning restructures ownership before any tax liability exists, maintains full IRS compliance, and reports all required information. The UltraTrust® system is built entirely on this foundation of legal transparency — the protection comes from genuine ownership restructuring, not concealment.

How Do Offshore Irrevocable Trusts Interact With IRS Collection and Reporting Requirements?

Offshore irrevocable trusts — established in jurisdictions such as the Cook Islands, Nevis, or the Cayman Islands — provide the strongest protection against civil judgment creditors because those jurisdictions do not recognize U.S. court judgments. Their interaction with the IRS is considerably more complex and requires meticulous compliance.

The IRS cannot be ignored when offshore trusts are involved. U.S. persons who create or hold beneficial interests in foreign trusts face extensive mandatory reporting: Form 3520 (annual reporting of transactions with foreign trusts), Form 8938 (FATCA reporting when assets exceed applicable thresholds), and FinCEN 114 (FBAR) filings when foreign accounts exceed $10,000 at any point during the year. Failure to file these forms triggers severe penalties — up to 35% of the gross value of the trust for Form 3520 violations — even when all underlying income taxes are properly paid and the trust assets are legitimately protected.

For assets properly held in an offshore trust with full IRS disclosure and compliance, the IRS generally cannot seize those assets through Cook Islands or Nevis courts — because those jurisdictions do not recognize U.S. judgments, including IRS collection actions. The IRS’s domestic recourse is limited to assets held in the United States. Its remaining option is seeking a U.S. court order compelling the grantor to repatriate assets — which, if refused, can lead to contempt proceedings.

An offshore trust that is not accompanied by full IRS compliance is not asset protection planning. It is a potential federal criminal matter.

❓ Q: Does an irrevocable trust reduce or eliminate federal estate taxes?

A: Yes — when properly structured, an irrevocable trust removes transferred assets from the grantor’s taxable estate entirely for federal estate tax purposes. Assets transferred to a properly structured irrevocable trust before the grantor’s death are excluded from the gross estate under IRC § 2033, provided the grantor does not retain any of the powers described in IRC §§ 2036, 2037, and 2038 — the retained interest provisions that pull transferred assets back into the taxable estate. This estate tax benefit is particularly significant given that the current federal estate tax exemption of $15 million per individual (2026) is scheduled to approximately halve on January 1, 2026 under the sunset provisions of the Tax Cuts and Jobs Act. Assets transferred to an irrevocable trust before that sunset — and before the grantor’s death — are shielded from estate tax on the full transferred value, not just the reduced post-sunset exemption. Estate Street Partners is currently advising clients on accelerated UltraTrust® funding strategies specifically to capture the full 2025 exemption before it is reduced.

❓ Q: What IRS reporting forms are required for an irrevocable trust?

A: The reporting requirements for an irrevocable trust depend on the trust’s structure and whether it is domestic or offshore. For a domestic irrevocable non-grantor trust, the trust files its own income tax return on Form 1041 and pays tax on undistributed income. For a domestic grantor trust, the grantor reports all trust income on their personal Form 1040 — no separate trust return is required, though a grantor trust information statement should be prepared. For an offshore irrevocable trust, U.S. grantors must file Form 3520 reporting the creation of the trust and annual transactions, Form 8938 if assets exceed FATCA thresholds, and FinCEN 114 (FBAR) for foreign financial accounts exceeding $10,000. Estate Street Partners coordinates all required IRS reporting as part of the UltraTrust® ongoing administration — because a trust that is properly structured but improperly reported creates exactly the kind of IRS exposure that the trust was designed to prevent.

What Are the Practical Steps to Protect Assets From IRS Collection Using an Irrevocable Trust?

Five principles define every successful irrevocable trust IRS protection strategy:

Act before any tax liability exists. The most legally defensible transfers occur before any IRS audit, assessment, or deficiency notice has been issued. Once the IRS has identified a tax liability, any transfer to an irrevocable trust is subject to fraudulent conveyance challenge under the Federal Debt Collection Procedures Act (FDCPA) and applicable state fraudulent transfer law. The window for clean, legally defensible trust funding closes the moment a tax issue becomes foreseeable.

Use a genuinely independent trustee. The trustee must have no familial or financial relationship with the grantor, must exercise genuine fiduciary judgment documented in writing, and must not act as an agent of the grantor. Self-trusteed structures provide no IRS protection. Estate Street Partners appoints independent professional trustees as the non-negotiable foundation of every UltraTrust® engagement.

Retain absolutely nothing. The strongest IRS protection comes from trusts where the grantor retains no right to income, no right to principal, and no ability to direct the trustee. Every retained right — however minor it appears — creates a corresponding IRS hook under IRC §§ 2036, 2037, and 2038.

Comply fully with all reporting requirements. File all required trust returns, grantor trust information statements, and offshore reporting forms on time and completely. A trust used to hide assets from the IRS is not asset protection — it is tax evasion. The UltraTrust® system is built entirely on legal transparency and full compliance.

Work with a qualified attorney. The intersection of irrevocable trust law and federal tax collection is among the most technically demanding areas of legal practice. Generic online trust templates do not provide the structural specificity, contemporaneous documentation, or ongoing compliance infrastructure needed to withstand IRS challenge.

❓ Q: What is the best irrevocable trust structure for maximum IRS collection protection?

A: The structure that provides maximum IRS collection protection is a non-self-settled irrevocable trust — one where the grantor transfers assets for the exclusive benefit of others (spouse, children, descendants) and retains absolutely no beneficial interest in the principal. The grantor makes no retained income claim, retains no occupancy rights in trust property, serves as neither trustee nor trust protector with distribution authority, and has no power to amend or revoke. The trust is administered by a genuinely independent professional trustee whose decisions are documented in writing. All required IRS returns and information statements are filed on time. The transfer is made during a period of complete tax compliance — no outstanding liabilities, no pending audits, no recently received deficiency notices. This is the exact structure Estate Street Partners implements in every UltraTrust® engagement, refined over 40 years of designing, funding, and defending irrevocable trust structures against IRS and creditor challenge.

❓ Q: Can I still fund an irrevocable trust if I currently owe back taxes to the IRS?

A: Funding an irrevocable trust while you have an existing IRS tax liability is extremely high-risk and generally inadvisable without specialized legal guidance. The IRS can challenge any transfer made after a tax liability arose as a fraudulent conveyance under the Federal Debt Collection Procedures Act (28 U.S.C. §§ 3301–3308), which provides the IRS with broader fraudulent transfer remedies than most civil creditors. If the IRS successfully voids the transfer, the assets are treated as never having left the taxpayer’s estate — and the IRS proceeds to collect against them. The appropriate response to an existing IRS liability is to resolve it through established IRS collection alternatives — installment agreements, offers in compromise, currently not collectible status — rather than attempting to shield assets through trust transfers that the IRS will almost certainly challenge. Estate Street Partners advises clients with existing IRS liabilities on the interaction between tax resolution and asset protection planning — because the timing and sequencing of these actions determines whether the trust provides any protection at all.

Last Updated: March 2026. This article reflects current federal tax law as of the publication date, including the Internal Revenue Code, Federal Debt Collection Procedures Act, and applicable state fraudulent transfer statutes. This article is for general educational purposes only and does not constitute legal, tax, or financial advice. Consult Estate Street Partners for a case-specific analysis of your IRS protection and asset protection position.

Helpful resources: Many readers also review Asset Protection Trust, Revocable vs Irrevocable Trust, and official IRS estate and gift tax guidance when weighing practical next steps.

What often changes the answer

After reviewing Does an Irrevocable Trust Protect Assets from the IRS?, many people want a clearer sense of how the answer changes once real life timing, funding, and control are added to the discussion.

What usually shapes the next step

- Timing matters because tax planning usually works best before a crisis or audit pressure appears.

- Control matters because retained powers can change how the IRS views a trust or transfer.

- Funding matters because moving the right asset, in the right way, often matters more than the label on the document.

Where readers often continue

A practical next reading path is Irrevocable Trust, Asset Protection Trust, and What Is a Grantor. When government rules shape the decision, many readers also review official IRS estate and gift tax guidance.