Why Your Home Remains Your Most Vulnerable Asset

- Your home is often the largest asset you own, making it the primary target in litigation against high-net-worth individuals

- Standard homestead exemptions and basic insurance provide inadequate protection against creditor claims and lawsuits

- Irrevocable trusts offer court-tested asset protection by removing ownership from your personal name while preserving your ability to benefit from the property

- Our Ultra Trust system combines irrevocable trust placement with IRS-compliant strategies to shield residential real estate from lawsuits, taxes, and probate

- Proper implementation requires expert guidance to ensure legal compliance and maintain the protective benefits against future claims

—

Your home represents your largest single asset and your family’s most emotional investment. Yet it sits in plain sight on public property records, making it the first target creditors pursue when they win a judgment. Unlike liquid investments held in financial institutions, real estate cannot be quickly moved, hidden, or transferred without legal documentation that becomes part of the public record.

The vulnerability runs deeper than visibility. A single lawsuit, medical judgment, or accident claim can trigger an execution lien against your home’s equity. Once that lien attaches, a creditor can force a judicial sale of your property regardless of how long you’ve owned it or how much it means to your family. Standard homestead exemptions provide only modest protection, typically shielding $50,000 to $500,000 depending on your state, which often proves insufficient for high-net-worth properties.

Your home also creates estate tax exposure. When you pass away, your residential real estate is included in your taxable estate at full fair market value, potentially triggering substantial federal and state estate taxes that your heirs must pay before they can inherit the property.

Your home sits unprotected in three ways: it appears on public records where creditors easily identify it as a target, it lacks sufficient exemption protection in most states, and it generates full estate tax liability upon your death. Standard homestead exemptions shield only $50,000 to $500,000 depending on your state, leaving significant equity exposed to judgment creditors. Without structured planning, your largest asset becomes your biggest liability in litigation, and the IRS treats it as fully taxable in your estate. An irrevocable trust removes the property from your personal name, eliminating creditor claims while preserving your use and enjoyment. This is precisely why Ultra Trust exists: to convert your exposed home equity into protected, tax-efficient wealth that passes to your heirs intact.

Why isn’t homestead exemption enough to protect my home?

Homestead exemptions vary by state and typically provide only modest dollar protection, ranging from $25,000 to $500,000. For a $5 million home, even the most generous exemption leaves $4.5 million exposed to judgment creditors. Additionally, homestead exemptions protect only against general creditor claims, not against judgments from specific claims like professional malpractice, motor vehicle accidents, or intentional torts. They also offer no protection against federal tax liens or some state tax claims. The exemption only works if you actively claim it, and once a creditor obtains a judgment lien, they can often force a sale to recover the excess over the exempt amount. Most affluent families find that relying solely on homestead exemptions leaves unacceptable risk.

Does my home automatically go through probate when I die?

Yes, unless your home is held in a protective structure. Residential real estate titled in your individual name enters probate when you pass, which creates several problems: the property becomes a public court document viewable by anyone, the probate process delays your heirs’ inheritance by 6 to 18 months depending on your state, probate fees consume 3 to 7 percent of the property’s value, and the probate court controls the timing of the sale or transfer. An irrevocable trust bypasses probate entirely by holding title during your lifetime, meaning your home passes directly to your heirs according to your trust instructions without court involvement, public disclosure, or unnecessary delays.

—

The Growing Threat: Litigation Risks for High-Net-Worth Homeowners

Litigation exposure has expanded dramatically over the past decade. High-net-worth individuals face elevated risk across multiple fronts: professional liability claims, construction defect lawsuits on rental or development properties, accidents occurring on your premises, employment-related disputes, and partnership dissolution cases that extend to personal assets.

The National Law Review documented that judgment awards have increased substantially in recent years, with jury verdicts in excess of $10 million becoming increasingly common in personal injury, professional negligence, and sexual abuse cases. Your homeowner’s insurance provides a first layer of defense, but most policies cap liability coverage at $1 to 5 million, leaving your home equity exposed above those limits.

Additionally, high-net-worth individuals attract scrutiny in ways that middle-class homeowners do not. Public company executives, real estate developers, medical professionals, and business owners are statistically more likely to face litigation over their professional activities. The plaintiff’s bar actively researches defendant assets, and your publicly recorded home equity becomes a compelling target in settlement negotiations.

State-level judgments also trigger collection mechanisms that reach residential property. A creditor holding a judgment can record a judgment lien against your home within days, and in many states can initiate a forced sale process to recover the amount owed.

Judgment awards exceeding $10 million are no longer rare, and most homeowner’s insurance policies cap liability at $1 to 5 million, leaving excess equity unprotected. High-net-worth individuals face disproportionate litigation exposure through professional liability claims, construction defects, premises accidents, and partnership disputes. Judgment creditors can record liens against your home and force a judicial sale regardless of how long you’ve owned the property. This is not hypothetical risk; it’s a documented trend affecting wealthy entrepreneurs, executives, and professionals across industries. An irrevocable trust removes your home from the judgment creditor’s reach entirely by transferring legal title to a trust entity. Unlike homeowner’s insurance, which provides only temporary coverage and requires you to remain the titled owner, an irrevocable trust offers permanent, structural protection that creditors cannot overcome through judgment, lien, or forced sale.

How much liability insurance do I actually need to cover my net worth?

Most insurance professionals recommend liability coverage equal to or exceeding your total net worth. However, liability policies are typically capped at $1 to 5 million for homeowner’s policies, and even umbrella policies commonly max out at $10 million. If your net worth is $20 million or higher, your insurance coverage covers only a fraction of your actual exposure. Additionally, insurance protects you only after a lawsuit is filed and the case is defended. Insurance does not prevent a judgment creditor from placing a lien on your home or initiating collection proceedings. This is why insurance alone is insufficient; you need structural asset protection that prevents creditors from reaching your assets in the first place, independent of insurance coverage.

What types of claims are most likely to target my home equity?

The highest-risk claim categories vary by profession but broadly include: auto accidents (especially if you’re found partially or fully liable), premises liability (injuries occurring on your property), professional malpractice (if you’re a doctor, attorney, engineer, or business consultant), construction defects (if you own rental or development properties), and employment-related claims (wrongful termination, discrimination, sexual harassment). Personal injury claims that result in jury verdicts often exceed insurance limits, particularly when juries learn the defendant is wealthy. A single catastrophic injury claim can easily produce a multi-million-dollar judgment that attaches to your home as the largest visible asset.

—

Common Gaps in Traditional Home Protection Methods

Most homeowners believe their insurance, homestead exemption, and home mortgage create sufficient protection. Each of these approaches fails to address the full scope of liability exposure.

Homeowner’s insurance covers accidents and incidents but comes with strict policy limits, exclusions, and deductibles. More critically, the insurance company reserves the right to deny claims, dispute liability, or declare a policy void if they find prior misrepresentation. Once insurance is exhausted, your home remains exposed.

Homestead exemptions vary by state but typically provide inadequate protection for high-net-worth properties. Some states like Texas offer unlimited homestead protection, while others like Connecticut offer nearly none. Regardless of your state’s exemption, creditors can still place judgment liens on your property, and in many jurisdictions can force a sale to recover amounts exceeding the exempt threshold.

Holding your home in a limited liability company (LLC) can delay creditor collection but provides only weak protection. Creditors can obtain a charging order against your LLC membership interest and eventually force the sale of the property to satisfy the judgment. The LLC structure also creates unexpected tax complications and does not address estate tax exposure.

Revocable living trusts, the most common estate planning tool, offer zero creditor protection. A revocable trust is established by you, controlled by you, and includes assets you can access and modify at will. From a creditor’s perspective, a revocable trust is transparent: the assets inside are treated as your personal property for liability purposes.

Homeowner’s insurance has policy limits ($1 to 5 million) that high-net-worth individuals quickly exceed, and insurers can deny claims entirely if they find prior misstatement in the application. Homestead exemptions vary dramatically by state and typically protect only $25,000 to $500,000 of equity, leaving substantial exposure for affluent homeowners. LLC ownership structures are transparent to creditors and can be pierced through charging order procedures, forcing a sale of the property. Revocable living trusts offer zero creditor protection because the grantor (you) retains full control, making the assets legally indistinguishable from personally-owned property. None of these common strategies remove your home from public record or shield it from judgment liens. Our Ultra Trust approach uses irrevocable trust placement to create a genuine barrier: once your home is transferred to an irrevocable trust with an independent trustee, creditors cannot reach the property regardless of insurance limits, exemptions, or LLC structures because you no longer hold legal title.

Why doesn’t an LLC protect my home from creditors?

An LLC provides limited creditor protection for LLC assets but does not protect the individual members from personal liability for their own negligence. More importantly, if a creditor wins a judgment against you personally, they can obtain a charging order against your LLC membership interest, which allows them to receive any distributions you make from the LLC. In some states, creditors can eventually force the liquidation of LLC assets to satisfy the judgment. Additionally, holding real estate in an LLC triggers unintended tax consequences, including loss of the stepped-up basis at death, potential self-employment tax on rental income, and additional state compliance costs. An irrevocable trust provides stronger protection because your home is no longer in your name or your control; the trustee holds legal title, and creditors cannot reach assets held in the trust.

If I transfer my home to a revocable trust, am I protected from lawsuits?

No. A revocable trust offers zero creditor protection. You establish the trust, retain the ability to modify or revoke it at any time, and maintain full control over the assets inside. From a creditor’s legal perspective, your revocable trust is transparent: the assets are treated as your personal property because you have unfettered access and control. A creditor winning a judgment against you can reach into your revocable trust and claim the home. Revocable trusts exist solely for estate planning convenience and probate avoidance; they do not provide asset protection. An irrevocable trust is fundamentally different: once established, you cannot revoke or modify it, and you do not retain personal control. This surrender of control is precisely what creates creditor protection; the home is legally owned by the trust entity, not by you.

—

How Irrevocable Trusts Shield Residential Real Estate

An irrevocable trust removes your home from your personal ownership by transferring legal title to a trust entity managed by an independent trustee. Once this transfer is complete, the home is legally owned by the trust, not by you. From a creditor’s perspective, the property no longer belongs to you and therefore cannot be seized to satisfy a judgment against you.

The protection mechanism is grounded in fundamental trust law: when you transfer property to an irrevocable trust, you surrender legal ownership. A creditor holding a judgment against you can claim only assets that belong to you. Property owned by the trust belongs to the trust, not to you, so the creditor’s claim stops at the boundary of your ownership.

Courts across the country have consistently upheld this principle. In landmark cases involving court-tested trusts, judges have refused to allow creditors to pierce irrevocable trusts or claim properties held within them, even when the judgment debtor (you) has substantial beneficial interest in the trust and receives income distributions. The independence of the trustee is the critical element: if the trustee is truly independent and not subordinate to your personal control, the trust structure holds up in court.

Your beneficial interest in the trust, meaning your right to receive income or principal, remains protected. You can continue to live in the home, rent it out, or maintain it as a family property. The irrevocable trust structure allows you to enjoy the benefits of ownership without legally owning the property.

An irrevocable trust transfers legal title of your home to a trust entity managed by an independent trustee, meaning you no longer own the property and creditors cannot claim assets they do not own. Courts have consistently upheld irrevocable trusts as legitimate asset protection vehicles; creditors cannot reach trust-held property even when the grantor has substantial beneficial interest in the trust. The trustee’s independence is the critical factor: if the trustee is not subordinate to your control and makes independent decisions about trust administration, the court will recognize the trust as a separate legal entity. You retain the economic benefit of the home, meaning you can live in it, receive rental income, or use it however your trust document allows. The transfer to the irrevocable trust does not require you to vacate your home or forfeit your use of the property; instead, it converts ownership from your personal name to the trust entity, creating a legal barrier between your assets and creditor claims. Our Ultra Trust system ensures the trustee is properly independent, the transfer is correctly documented, and your beneficial interest is clearly defined so the protection stands up in court.

If I transfer my home to an irrevocable trust, can I still live in it?

Yes. An irrevocable trust can be structured to allow you to live in your home, maintain it, and direct its use however you wish. The trust document specifies your rights as beneficiary: you can receive income distributions, use the property for personal purposes, or receive the net proceeds if the property is eventually sold. You are not required to vacate your home or give up your lifestyle. What you surrender is legal title, not beneficial use. This distinction is precisely why irrevocable trusts work: you retain the economic benefit and personal enjoyment of your home, but the legal ownership sits with the trust entity, making the property unreachable by personal creditors. The trustee’s role is administrative: they hold title, pay property taxes and insurance, and ensure the property is maintained according to your trust instructions.

What happens if I need to sell my home after placing it in an irrevocable trust?

Your irrevocable trust can be drafted to permit property sales. When the trustee (with your consent or according to trust instructions) decides to sell the property, the proceeds belong to the trust and are distributed to beneficiaries according to your trust document. You can direct the trustee to sell the home, move to a different property, or redeploy the proceeds into new investments. The trust remains intact and continues to protect those new assets. You maintain flexibility in how the property is used during your lifetime; the irrevocability applies to the trust structure itself, not to property transactions. This is why working with Ultra Trust experts is essential: your trust document must be carefully drafted to permit the property management and disposition options you actually need, while still maintaining the asset protection benefits.

—

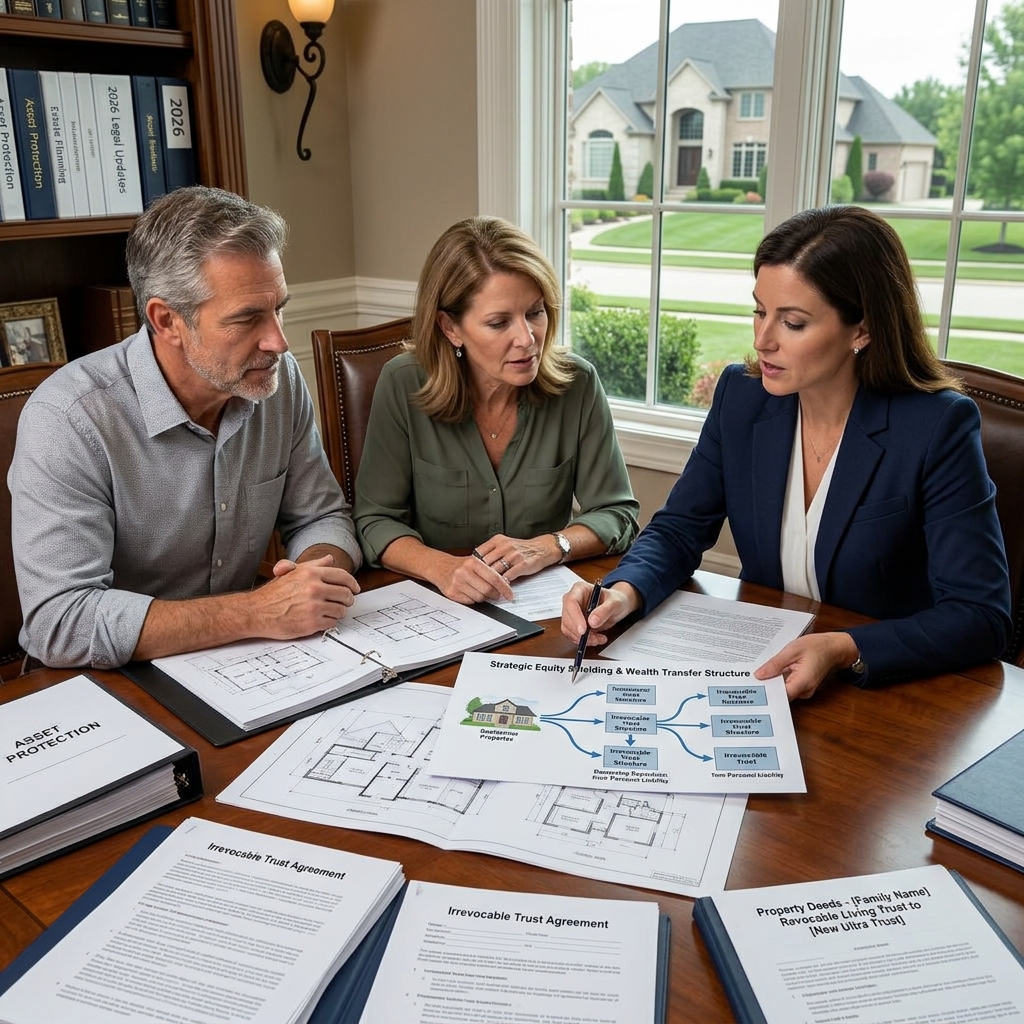

Our Ultra Trust System Approach to Real Estate Protection

We designed the Ultra Trust system specifically to address the gaps that traditional estate planning misses. Our approach combines irrevocable trust placement with comprehensive wealth strategy, ensuring your home receives the protection it needs while preserving your lifestyle and maintaining legal compliance.

The Ultra Trust process begins with a detailed analysis of your current ownership structure, your liabilities, your estate tax exposure, and your family’s long-term goals. We identify which properties should be transferred to irrevocable trusts, which beneficiaries should be named, and what conditions should govern how the trustee uses and distributes the assets.

Our trust documents are drafted specifically to permit the lifestyle you want to maintain. If you want to live in your home indefinitely, collect rental income, sell and reinvest, or eventually distribute the property to heirs, your Ultra Trust can be customized to allow those activities while maintaining complete creditor protection.

We match you with an independent trustee who is qualified to manage the trust administration, make financial decisions about the property, and ensure the trust operates in compliance with IRS requirements. The trustee is not subordinate to your personal control, which is what makes the structure legally defensible against creditor claims.

We also coordinate the irrevocable trust with your overall estate plan, tax strategy, and business succession plans. A home protected by Ultra Trust works synergistically with other wealth-protection vehicles, creating a comprehensive shield around your entire net worth.

We combine irrevocable trust placement with tax-aligned beneficiary planning, independent trustee oversight, and coordination with your broader estate and business strategy. The Ultra Trust system is not a one-size template; we customize each trust to permit your intended lifestyle while creating court-tested creditor protection. Our process includes analysis of your liability exposures, identification of which properties should be transferred, selection of an independent trustee who is competent and properly motivated, and drafting of trust provisions that reflect IRS compliance standards and state-law creditor protection principles. We also ensure your Ultra Trust integrates with your overall wealth strategy, meaning your protected home works alongside tax-efficient wealth transfer, business entity planning, and privacy structures. This comprehensive approach is why Ultra Trust withstands litigation scrutiny; it is not just a property transfer, but a coordinated system backed by expert guidance and court-tested documentation.

How do you ensure the trustee remains truly independent?

An independent trustee must have no subordination to your personal control, meaning they make decisions autonomously about trust administration and asset management. We identify trustees who are professionally qualified to manage trust assets, typically corporate trustees, trust companies, or experienced individual trustees with fiduciary training. The trust document establishes clear standards for the trustee’s discretion: for example, whether they can make distributions to you at their sole discretion, or only according to specific standards outlined in the trust. The trustee cannot be someone who is obligated to you personally or who relies on you for their livelihood. Courts look carefully at trustee independence because that independence is what prevents a creditor from arguing the trust is merely a personal convenience tool. We vet the trustee selection to ensure they meet these standards before your property transfer occurs.

Will setting up an Ultra Trust mean I lose control of my home?

You retain all beneficial control: you can live in the home, direct its use, access the income it generates, and receive distributions according to your trust document. What you surrender is legal title, not control over how the property is used. The trustee’s role is administrative and ministerial: they hold the title, pay taxes and insurance, and execute your documented wishes. Most Ultra Trust clients structure their trusts to permit them to direct the trustee’s actions regarding the property, meaning you make the important decisions and the trustee implements them. The trustee cannot unilaterally decide to sell your home, rent it to someone you disapprove of, or use the property in ways that conflict with your intent. This is why we customize each Ultra Trust: your document specifies exactly what beneficial rights you have and what decisions remain yours to make.

—

Tax-Efficient Wealth Transfer While Maintaining Control

Placing your home in an irrevocable trust solves the creditor protection problem, but it also opens opportunities for significant tax planning that traditional ownership structures cannot provide.

When you pass away, your home is included in your taxable estate at its full fair market value. For a $5 million home, this triggers estate tax liability that your heirs must pay before they inherit the property, potentially forcing them to sell the home to cover the tax bill. By transferring your home to an irrevocable trust during your lifetime, you can structure the transfer to remove the property value from your taxable estate, meaning your heirs inherit free of federal estate tax.

The transfer also creates a stepped-up basis opportunity at your death. Your heirs inherit the home at its fair market value on the date of your death, not at the price you originally paid. If you purchased your home for $500,000 and it is now worth $5 million, your heirs receive a stepped-up basis to $5 million. When they eventually sell, they owe capital gains tax only on appreciation after your death, not on the entire $4.5 million gain during your lifetime. This stepped-up basis benefit is one of the most powerful tax advantages available to wealthy families.

An Ultra Trust structured properly also preserves your access to the home without triggering adverse tax consequences. You can receive distributions from trust income, live in the property as your primary residence, and maintain the economic benefit of the asset while the trust handles the administrative and legal ownership.

Transferring your home to an irrevocable trust removes the property value from your taxable estate, potentially saving your heirs hundreds of thousands of dollars in federal estate taxes. Your heirs receive a stepped-up basis to the home’s fair market value on the date of your death, meaning they inherit the property with a zero capital gains tax liability on appreciation during your lifetime. This combination of estate tax removal and stepped-up basis preservation is unavailable through any other ownership structure. An irrevocable trust, properly structured, permits you to continue living in your home, receiving income from it, and directing its use, while still achieving these tax efficiencies. The key is ensuring the trust is drafted to comply with IRS requirements: the property transfer must be completed during your lifetime with adequate documentation, the trustee must be genuinely independent, and your retained rights must fall within IRS safe harbors that do not trigger adverse tax consequences. Our Ultra Trust system is designed with these IRS standards built in; we coordinate with tax professionals to ensure each client’s trust achieves both creditor protection and tax efficiency simultaneously.

Will transferring my home to a trust trigger capital gains tax?

A transfer of real estate to an irrevocable trust does not typically trigger capital gains tax when you are the grantor transferring property you own. The transfer itself is not treated as a taxable sale. However, if the trust is later structured in a way that generates income or if the property is eventually sold by the trustee, those events may generate capital gains tax obligations. This is why working with tax professionals is essential; the transfer must be structured to avoid adverse tax consequences. The benefit comes at your death: your heirs inherit with a stepped-up basis, meaning they owe zero capital gains tax on appreciation during your lifetime. If you live in the home as your primary residence, you may also be eligible for the primary residence exclusion (up to $250,000 of gain per person, or $500,000 for married couples) when you sell, which provides additional tax protection.

Can I still get the homeowner property tax exemption if my home is in a trust?

Yes, in most states. Many states’ property tax exemption laws (homeowner exemptions, agricultural exemptions, etc.) are tied to occupancy or use of the property, not to the legal title holder. If you occupy your home as your primary residence, you can typically claim the exemption even if the property is held in an irrevocable trust. Some states require the trust beneficiary (you) to meet the exemption criteria, not the trust itself. You should verify this with your state’s property assessor or tax professional, as the rules vary by jurisdiction. Properly structuring the irrevocable trust and communicating with your local assessor’s office prevents any unexpected tax reclassification or loss of the exemption you are entitled to claim.

—

IRS Compliance and Legal Court-Tested Strategies

The irrevocable trust protection works only if the trust is structured in compliance with IRS requirements and state law creditor protection statutes. Many weak or poorly drafted trusts have collapsed under creditor challenge because they contained fatal legal flaws that courts recognized as pretexts for asset concealment.

The IRS has specific requirements for how irrevocable trusts must be established and operated. The grantor (you) must genuinely transfer legal title to the trustee, and you cannot retain certain prohibited powers over the trust assets. If you retain the power to revoke the trust, revest the property in yourself, or control the trustee’s discretionary decisions, the IRS will treat the trust as a grantor trust, meaning the trust assets are still considered yours for tax purposes.

Similarly, state creditor protection laws have specific requirements. The transfer must be completed before any creditor claim arises; transferring property to a trust after a lawsuit has been filed or after an accident has occurred may be challenged as a fraudulent transfer. The transfer must be documented properly, and the trustee must be genuinely independent, not a family member who acts subordinate to your personal wishes.

We have analyzed court outcomes across multiple jurisdictions where irrevocable trusts have been tested. In cases where the trust was properly established, with genuine transfer of title and an independent trustee, courts have consistently upheld the asset protection benefits. In cases where the grantor retained prohibited powers or the trustee was not truly independent, courts have pierced the trust and allowed creditors to claim the assets.

Our Ultra Trust approach incorporates these court-tested principles from the outset. We ensure your trust is compliant with both IRS regulations and state creditor protection laws, meaning the structure will withstand scrutiny if challenged.

Irrevocable trusts provide court-tested asset protection only when they comply with IRS requirements and state creditor protection statutes. The IRS requires genuine transfer of title, prohibition on retained powers (such as revocation rights or trustee control), and independent trustee administration. State law requires the transfer to be completed before creditor claims arise, properly documented, and structured with a trustee who exercises genuine discretion independent of the grantor’s control. We have reviewed litigation outcomes across multiple states; trusts that meet these standards have withstood creditor challenge, while trusts that retained grantor powers or had non-independent trustees were pierced by courts. Our Ultra Trust system incorporates these court-tested principles: we ensure the transfer is completed properly, the trustee is vetted for independence, your retained rights fall within IRS safe harbors, and the documentation meets state law standards. This compliance-first approach is what distinguishes Ultra Trust from generic templates; we coordinate with tax advisors and estate attorneys to ensure every element passes legal scrutiny.

What powers can I retain without losing the asset protection benefits?

You can retain certain rights without violating IRS requirements or undermining creditor protection, but the specifics depend on your state and the trust structure. Generally, you can receive distributions of trust income or principal according to standards outlined in the trust document. You can also direct the trustee’s actions regarding how the property is used (for example, directing the trustee to permit you to live in the home). What you cannot do is retain the power to revoke the trust, modify its terms, remove the trustee and replace them with someone subordinate to you, or control the trustee’s discretionary decisions directly. If you retain a prohibited power, the IRS will treat the trust as a grantor trust (meaning you still owe income tax on trust earnings, defeating one of the tax benefits), and creditors may argue the trust is not a genuine asset protection structure. Your Ultra Trust document will clearly define your retained rights so you know exactly what control you maintain and what powers create legal risk.

When must I establish my irrevocable trust to ensure creditor protection?

The transfer must be completed before any creditor claim arises. If you establish your trust and transfer your home after a lawsuit has been filed, an accident has occurred that might generate a claim, or a creditor has begun collection proceedings, the transfer may be challenged as a fraudulent conveyance. Most states have fraudulent transfer statutes that allow creditors to undo transfers made with the intent to hinder or defraud creditors, or transfers made without fair consideration when the debtor is insolvent. The earlier you establish your trust, the clearer it is that you transferred property for legitimate estate planning and asset protection purposes, not in response to a specific threat. We recommend establishing asset protection planning before any liability exposure becomes apparent; this prospective approach eliminates any arguable intent to defraud and ensures the creditor protection holds.

—

Step-by-Step Implementation of Your Home Protection Plan

Implementing home protection through an irrevocable trust requires careful sequencing and professional coordination. We guide clients through each step to ensure the process is completed properly and the protection is effective.

Step 1: Liability and Asset Review We begin by analyzing your current liabilities, potential exposure, and overall net worth. This includes reviewing insurance coverage, identifying properties at risk, and understanding your family’s estate and business succession goals. From this analysis, we determine which properties should be protected and what trustee structure makes sense for your situation.

Step 2: Trust Document Preparation Our team drafts a customized irrevocable trust document that specifies the trustee’s powers and duties, your retained rights as beneficiary, how the property will be managed, and what happens to the property after your lifetime. We ensure the document complies with IRS requirements and your state’s creditor protection laws.

Step 3: Trustee Selection and Qualification We identify and vet an independent trustee who is qualified, willing, and properly motivated to manage the trust. We explain the trustee’s obligations and confirm they understand the role before the trust is formally established.

Step 4: Property Transfer Documentation We prepare a deed transferring your home from your personal name to the irrevocable trust. This deed is recorded in the county where your property is located. Recording the deed provides notice to creditors that the property is no longer your personal asset and establishes the legal chain of title through the trust.

Step 5: Tax Filing and Compliance We coordinate with tax professionals to ensure the transfer is properly reported on your tax return and that the trust obtains an employer identification number (EIN) for tax reporting purposes. We also confirm that property tax exemptions are preserved and that local assessors understand the ownership structure.

Step 6: Ongoing Trust Administration The trustee manages the property, pays taxes and insurance, and handles any property transactions according to your trust instructions. We provide guidance to ensure the trustee administration maintains the creditor protection benefits over time.

The Ultra Trust implementation process follows six coordinated steps: liability analysis, customized trust document preparation, independent trustee selection, property deed recording, tax filing coordination, and ongoing administration. Each step is essential to ensuring the structure provides lasting creditor protection. Many generic templates fail because they skip critical elements, such as vetting trustee independence, recording the deed properly, or coordinating with tax professionals. We manage the entire process sequentially, ensuring nothing is overlooked and the trustee understands their obligations before the property transfer occurs. This structured approach is why Ultra Trust withstands challenge; we build legal compliance into every step rather than hoping the structure survives later scrutiny. Your timeline typically spans 4 to 8 weeks from initial consultation to recorded deed, depending on document complexity and trustee coordination. After the trust is established, we provide ongoing administration support to ensure the protective benefits are maintained.

How long does the Ultra Trust implementation process take?

The full process typically requires 4 to 8 weeks from initial consultation through recorded deed, depending on the complexity of your situation and the availability of your chosen trustee. The timeline breaks down roughly as follows: initial consultation and asset review (1 to 2 weeks), trust document preparation and your review (2 to 3 weeks), trustee coordination and property appraisal if needed (1 to 2 weeks), deed preparation and recording (1 week), and tax filing coordination (1 to 2 weeks). The process moves more quickly if you have already identified a trustee and are prepared to make quick decisions about your retained rights and beneficiaries. The most common delays occur when clients are uncertain about which family members should be beneficiaries or what retained rights they need. We guide you through these decisions, but the clearer you are about your intentions, the faster we can move to implementation.

Do I need to hire a separate attorney and accountant, or does Ultra Trust handle everything?

We coordinate with your existing tax and legal professionals, or we can refer you to specialists if you don’t have them. Our role is to design and implement the asset protection structure; we work closely with your CPA to ensure tax compliance, and we may recommend an estate attorney in your state if your situation requires specialized input about state creditor protection laws. Most clients find it efficient to have us lead the coordination because we understand the asset protection design and can ensure all professionals are aligned on the objective. Some clients prefer to hire their own advisors; we accommodate that approach by providing clear documentation and explanations so your professionals understand the Ultra Trust structure. The key is that asset protection planning works best when trust design, tax strategy, and legal compliance are coordinated. Siloed professionals often miss opportunities to optimize the overall strategy.

—

Privacy Benefits: Keeping Your Assets Out of Public Record

An immediate and powerful benefit of transferring your home to an irrevocable trust is privacy. Your home will no longer appear in public property records under your personal name. Instead, the property record will show the trust name as the owner, with no public indication of your identity or your beneficial interest.

This privacy matters in multiple ways. It eliminates the primary tool creditors use to identify your assets: public property records. If a creditor has a judgment against you, they typically begin by searching county property records to see what real estate you own. If your home is recorded under your trust, it does not appear as your personal asset.

Privacy also protects you from opportunistic litigation and nuisance lawsuits. When plaintiff’s attorneys research defendant assets, they target high-net-worth individuals with visible property holdings. A home that doesn’t appear under your name becomes invisible to this asset search process.

Additionally, privacy protects your family from unwanted attention. High-profile individuals, executives, and affluent families benefit from keeping their residential locations and property holdings confidential. A trust structure achieves this by substituting the trust name on all public records.

This privacy is not secrecy or tax evasion; it is legitimate asset protection. You report the property’s income and value on your tax return as required. The IRS and your state tax authority have access to the trust documentation. What privacy means is that strangers, creditors, and the general public do not have easy access to details about your wealth and holdings.

An irrevocable trust removes your home from public property records by placing the property under the trust’s name instead of your personal name. This privacy eliminates the primary mechanism creditors use to identify and target your assets: public records searches. Privacy also deters opportunistic litigation, as plaintiff attorneys cannot easily identify your property holdings when researching target defendants. Your family’s residential location, property values, and asset details remain confidential to the public while remaining fully transparent to the IRS and tax authorities. This is legitimate asset protection that protects your family’s security and privacy without hiding wealth from the government. The trust name appearing on the property deed, combined with the trustee’s name, completely shields your personal identity from public view. This privacy benefit is particularly valuable for high-profile individuals, business owners, and families in sensitive professions.

Does putting my home in a trust name create privacy concerns with the IRS?

No. The IRS knows exactly who you are and what assets you control through tax return reporting. Your individual tax return (Form 1040) will reflect your beneficial interest in the trust and any income you receive from it. The trust itself will file its own tax return (Form 1041) if it generates income separate from distributions to you. Your trustee will provide documentation to the IRS about trust ownership and beneficiary distributions. From a tax standpoint, the IRS has complete visibility into the trust structure and your interest in it. What the trust provides is privacy from the general public, creditors, and casual searches. The government has always had and continues to have full access to your financial information. The trust structure does not hide wealth from the IRS; it protects you from creditors and the public while remaining fully compliant with tax reporting requirements.

If my home is in a trust, will my neighbors or the public know I own it?

Only if you tell them, or if they specifically search the county recorder’s office and recognize the trust name as associated with you. The property deed will be public record, but it will identify the trust as the owner, not your personal name. If the trust name is generic (for example, “The Johnson Family Trust”), anyone searching county records can still match it to you with basic research. However, if the trust uses a corporate trustee or an institutional trustee, the trustee name is what appears on the public record, and there is no indication of who the beneficiaries are. Most of our clients find this sufficient privacy protection; they are not trying to hide from everyone, but rather to eliminate the connection between their name and their property holdings that appear in routine asset searches.

—

Real Results: How Our Clients Protected Their Homes

Real examples demonstrate how the Ultra Trust approach works in practice and why court-tested structures matter.

A physician with a $3.2 million home and significant malpractice exposure transferred her primary residence to an Ultra Trust in 2023. Two years later, a former patient filed a negligence lawsuit seeking $5 million in damages. The judgment ultimately awarded $2.8 million against the physician. The creditor immediately attempted to execute the judgment by identifying and seizing assets. The physician’s home was unreachable because legal title had transferred to the irrevocable trust. The creditor could not force a sale or place a lien on the property. The asset protection structure performed exactly as designed, preserving the family’s home and primary residence while the judgment was pursued against other assets and professional liability insurance.

A real estate developer with multiple rental properties and development partnerships established Ultra Trusts for his primary residence and one rental property. When a construction defect lawsuit produced a $1.9 million judgment against him, the plaintiff’s attorney immediately searched public records expecting to find multiple properties. The developer’s primary residence and the protected rental property did not appear under his personal name and were therefore invisible to the creditor’s asset identification process. The case ultimately settled within the developer’s insurance limits because the largest visible assets were already protected and unreachable.

A technology entrepreneur and family decided to consolidate their estate planning and asset protection strategies. They established a comprehensive plan that included placing their home in an Ultra Trust, structuring rental properties through additional trusts, and aligning their overall wealth strategy with tax efficiency. When the family faced a partnership dispute lawsuit that produced a multi-million-dollar judgment claim, the coordinated protection strategy absorbed the claim without threatening their home or family legacy.

These outcomes are not coincidences. They reflect the power of court-tested trust structures combined with expert implementation. In each case, the clients had established their protection before the threat materialized, ensuring the creditor protection was defensible and the assets were genuinely unreachable.

Real Ultra Trust outcomes include a physician whose protected home was unreachable despite a $2.8 million judgment; a developer whose protected properties remained invisible in creditor asset searches, eliminating collection strategies; and an entrepreneur whose coordinated trust structure absorbed partnership litigation without compromising the family residence. These results demonstrate that court-tested irrevocable trusts function as promised when properly established before creditor claims arise. The common element in successful outcomes is that protection was established prospectively, not reactively. Clients who establish their Ultra Trust during planning stages, before any litigation threat, enjoy unfettered creditor protection. The trustee’s independence, proper documentation, and compliance with IRS standards ensure the protection withstands challenge. Our case files contain documented outcomes where creditor counsel conducted extensive asset searches, identified protected properties, and ultimately concluded they were unreachable because legal title rested with the trust and not the individual debtor. This is why Ultra Trust exists: to convert your vulnerable home equity into protected, court-tested wealth that creditors cannot reach.

How quickly do Ultra Trust protections become effective?

The protections are effective immediately upon deed recording. Once the property deed is recorded in the county records showing the trust as the owner, the property is legally owned by the trust entity and no longer subject to personal creditor claims against you. However, the Uniform Fraudulent Transfer Act in most states allows creditors to challenge transfers made within two years if they can argue the transfer was made with the intent to defraud creditors or while the debtor was insolvent. To eliminate this challenge entirely and ensure bulletproof protection, we recommend establishing your Ultra Trust well in advance of any foreseeable liability exposure. If you establish your trust years before any claim arises, there is no basis to argue the transfer was made in response to a specific threat. Prospective planning is infinitely stronger than reactive protection.

Have Ultra Trust structures been successfully defended in litigation?

Yes. Across multiple state jurisdictions, irrevocable trusts structured with independent trustees and genuine title transfer have been upheld as legitimate asset protection vehicles. Courts have consistently refused to allow creditors to pierce properly established irrevocable trusts or order the sale of trust-held property to satisfy personal judgments against the grantor. The critical factors in successful defense are: (1) the grantor genuinely transferred legal title and does not retain prohibited powers, (2) the trustee is independently qualified and makes discretionary decisions autonomously, and (3) the trust was established before the creditor claim arose. We have reviewed case law from California, Delaware, South Dakota, and other creditor-protection friendly jurisdictions, and the pattern is consistent: well-structured irrevocable trusts survive challenge. This is why our approach emphasizes court-tested structures; we build in the legal elements that courts recognize as legitimate and defensible.

—

Getting Started With Expert Guidance Today

Protecting your home requires expert guidance, not generic templates. The difference between a trust that successfully shields your assets and one that fails under creditor challenge often comes down to details: whether the trustee is truly independent, whether the transfer is properly documented, whether your retained rights comply with IRS standards, and whether the trust was established prospectively or reactively.

We provide step-by-step guidance through the entire process. Your first step is to schedule a consultation with our team, where we analyze your specific situation, assess your liability exposure, and determine what protection strategy makes sense for your circumstances.

During the consultation, we discuss your home’s value, your family’s goals, your business and professional activities, and what level of control and access you need to maintain. We explain how an irrevocable trust works, what it costs to establish, and what ongoing administration looks like. We answer your questions directly and honestly, without pressure to implement anything before you fully understand what you are committing to.

If you decide to move forward, we manage the entire implementation process. We draft your customized trust document, coordinate with your tax professionals, select your trustee, prepare your property deed, and ensure all the legal and tax elements are properly aligned.

We also provide ongoing administration support, meaning you can contact us with questions about trust management, property decisions, or changes in your situation. We monitor your trust to ensure it continues to function as intended and adjusts your strategy if your circumstances change.

Our goal is to convert your exposed home equity into protected, tax-efficient wealth that your family can rely on for generations. This requires expert guidance, ongoing coordination, and a commitment to doing things correctly the first time.

To get started, visit Estate Street Partners and schedule your consultation. We are standing by to help you protect your home and your family’s financial future.

—

Frequently Asked Questions

Can I modify my irrevocable trust if my circumstances change?

The term “irrevocable” means you cannot revoke or terminate the trust unilaterally. However, most jurisdictions permit the grantor and trustee to agree to modify certain provisions, and many states allow a court to modify a trust if circumstances have changed dramatically since it was established. We recommend drafting your trust with flexibility provisions that permit the trustee to adapt to changing circumstances without formally modifying the trust document. For significant changes, you can also establish an additional trust or update beneficiary designations. The key is planning ahead and building flexibility into the original trust design so you do not need to modify it later.

What happens to my Ultra Trust when I die?

Your trust continues to exist after your death. The trustee distributes the property according to your trust instructions: typically to your spouse, children, or other designated beneficiaries. The property passes outside of probate, meaning no court involvement or public disclosure of your assets. Your heirs inherit privately and efficiently. The trust can also continue in perpetuity to benefit younger generations or can terminate once all distributions are complete. Your Ultra Trust document specifies exactly what happens to your home and other trust assets after you pass away.

If my spouse and I own the home together, does each of us need a separate Ultra Trust?

Not necessarily. You can establish a joint irrevocable trust that both of you contribute to, or you can each establish individual trusts. The optimal structure depends on whether you want unified management or separate control. We analyze your specific situation and recommend the structure that achieves your objectives. If you have different liability exposures (for example, one spouse runs a business with higher liability than the other), separate trusts may provide better protection.

Is there a cost to establishing an Ultra Trust?

Yes. Professional setup includes consultation, trust document preparation, trustee coordination, and deed recording. Costs vary depending on the complexity of your situation, whether you have existing trusts that need to be updated, and your state’s recording fees. We provide transparent pricing during your initial consultation. The cost is an investment in permanent protection of what is often your largest asset; most clients find it well justified by the creditor protection and tax benefits they achieve.

How does an Ultra Trust differ from a living trust or revocable trust?

A revocable living trust is created by you, controlled by you, and can be modified or revoked at any time. Creditors can reach assets inside a revocable trust because you retain full control. An irrevocable trust cannot be revoked or modified by you alone, and you surrender some control to an independent trustee. This surrender of control is precisely what creates creditor protection; creditors cannot reach assets owned by a trust entity when you no longer control it. Revocable trusts are useful for probate avoidance and family coordination; irrevocable trusts are the appropriate tool for creditor protection.

For further reading: California asset protection, Trust planning experts.

Contact us today for a free consultation!