“The ancient Egyptians built elaborate fortresses and tunnels and even posted guards at tombs to stop grave robbers. In today’s America, we call that estate planning.”

“The ancient Egyptians built elaborate fortresses and tunnels and even posted guards at tombs to stop grave robbers. In today’s America, we call that estate planning.”A TRUST is nothing more than a private CONTRACT.

The Medallion Trust®

(Registered Trademark of Estate Street Partners, LLC)

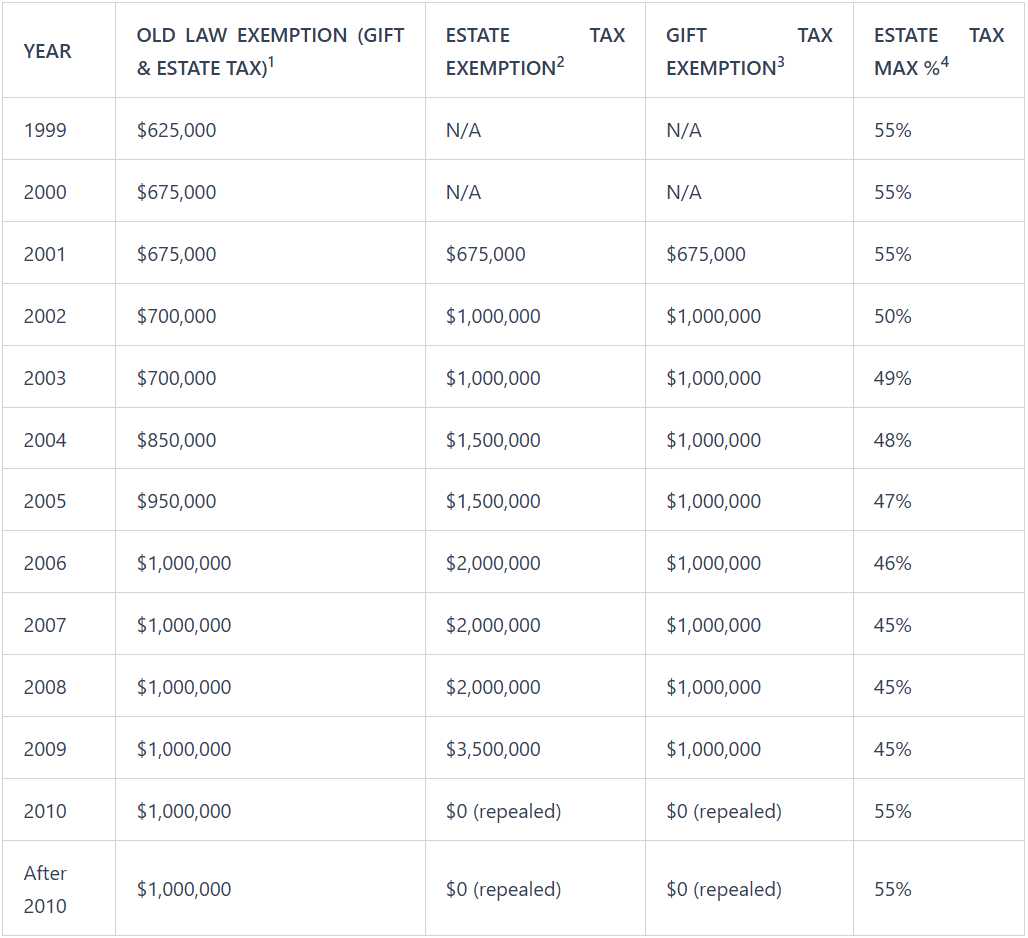

In anticipation of congress making additional changes to the estate tax and gift tax rules, the MEDALLION TRUST® has been financially engineered to take advantage of your “legal exceptions/exemptions loopholes” – by claiming your tax exemptions, now!!! You can give away up to $1,000,000 of your wealth this year ($1,000,000 for the year 2002 to 2009, and back to $675,000 in 2010 (see table below). NOTE: The Dreaded Phase-In of the 2001 Tax Act has increased your need for Estate Tax and Gift Tax Planning.

By “GIFTING” your assets to the MEDALLION TRUST® and by filing IRS Form 709 (United States Gift and Generation-Skipping Transfer Tax Return) you can claim your unified credit against taxes that would normally be paid by your estate. Thus, for the year 2006 you and your spouse each can “GIFT” up to $1,000,000 ($2,000,000 combined) of your wealth without incurring any tax liability. (For the new Tax Act, see below)

Tax Neutral

There’s absolutely no downside risk with the MEDALLION TRUST®. By engineering your assets around “legal exceptions and tax exemptions” you can avoid unwanted taxable results by claiming your loophole, now!

- ESTATE – The Fair Cash Value of anything (in your name) on the date of your death.

- ESTATE TAX – Anything in your estate (in your name) is taxable up to 55% with small reductions under the new Tax Act of 2001. Anything NOT in your name, is NOT taxable.

- PROBATE – Anything in your Trust, avoids probate. Anything NOT in your Trust, goes to probate, with or without a will.

- WILL – A listing of your wishes to be executed on the date of your death. A will does not avoid probate.

- TRUST – An “artificial legal person” created by private contract.

Congress: “Death and Taxes”

Various tax proposals were being bandied about, including House Ways and Means Chairman, Bill Archer, who said that he was “pushing” to “g-r-a-d-u-a-l-l-y phaseout” the death tax within the next 10 years. (The word “gradually” has been emphatically stretched out.) “Death by itself should not trigger a tax” said Chairman Archer. The Dreaded Phase-In of the 2001 Tax Act has increased your need for Estate Tax and Gift Tax Planning. (see table below)

The federal government has done all it can to ensure they become your largest “heir” by collecting estate taxes from 37% to 55% on 100% of your wealth. The 2001 Tax Act stretches out a small reduction but not eliminated. Only Japan has a higher rate of estate taxes at 70%. Germany takes a maximum of 40%, while Australia and Canada, take nothing.

“I believe, we all should pay taxes with a smile. I tried, … but they wanted cash.”

-anonymous, The Penguin Dictionary of Humorous Quotations

Add it all up!!! Federal tax, state tax, probate fees, legal fees, accounting fees, appraisal fees, administrative and executor fees, and etc. fees; it could easily cost you 70 to 80% of you hard earned estate. You can avoid these unwanted results.

Some statistics on death & transfer taxes:

- 13 times in 25 years, congress has changed the rules. Congress is always tinkering with the “Death Transfer Tax.” They believe, they know better than you, how they should spend your money; before and after your death.

- 43% federal death tax rate or $2,170,250 owed by a California resident who died with a $5,000,000 estate, plus an additional 10% payable to the state of California. (source: CA-Probate.com)

- 70% – percentage of Americans who die without a will. (source: Wealthcare.com)

- 35% – the percentage of widows aware of the 55% federal estate tax.

- 60% to 85% – the percentage of gross household income that you will need for your retirement to sustain your current lifestyle. (source: Wall Street Journal)

- $23,500,000,000 – the amount of tax dollars collected from 1998 estate tax returns filed. (source: US Treasury Department)

The MEDALLION TRUST® was meticulously crafted and specifically engineered to take advantage of your “Gift” and “Estate Unified Tax Credit.” This legal exception/exemption (LOOPHOLE) is presented in the table below.

The New 2001 Tax Act:

1 – OLD LAW – this is the old law where the exemption amount that could have been gifted per person and not subject to a gift tax or estate tax.

2 – ESTATE TAX – in effect 2002 and thereafter. This estate tax exemption is the amount that may be exempted if you die in that year.

3 – GIFT TAX – in effect 2002 and thereafter. This gift tax exemption is limited to an individual’s lifetime total of $1 million.

4 – ESTATE TAX MAX – the maximum percentage of estate tax

- If your exclusion goes up you merely add additional assets to your MEDALLION TRUST®

- If your exclusion is reduced or eliminated, you have LOCKED IN your LOOPHOLE.

Additional benefits of the MEDALLION TRUST®:

- Income Tax Neutral – absolutely no downside to all “income tax” benefits from underlying asset(s), i.e. you receive deductible real estate tax, mortgage interest on your form 1040.

- Defers Capital Gains Taxes on Real Estate (under certain conditions). Contact us for more information.

- Eliminates the expensive, time consuming “Probate Process” that could take years and consume your wealth.

- Eliminates Estate Taxes and Legal Fees in settlement of your hard earned estate

HOW DO I GET A MEDALLION TRUST®?

1.Your TRUSTEE which could be your best friend, lawyer, accountant, … any individual you select will set up:”The —Name— MEDALLION TRUST® under the laws of your state.

2.You “GIFT” your private residence or any other valuable assets(s) at Fair Market Value, to:your MEDALLION TRUST®Note: your Non- Taxable gift(s) are subject to your legal loophole amounts (see above).

3.You and your spouse each will file a “Gift Tax Return IRS Form 709” for the value of the asset(s) gifted to:your MEDALLION TRUST®

4.A checking account is established in the name of your trust with power of attorney granted to you or your spouse (as the attorney in fact). All your expenses are paid through your MEDALLION TRUST®

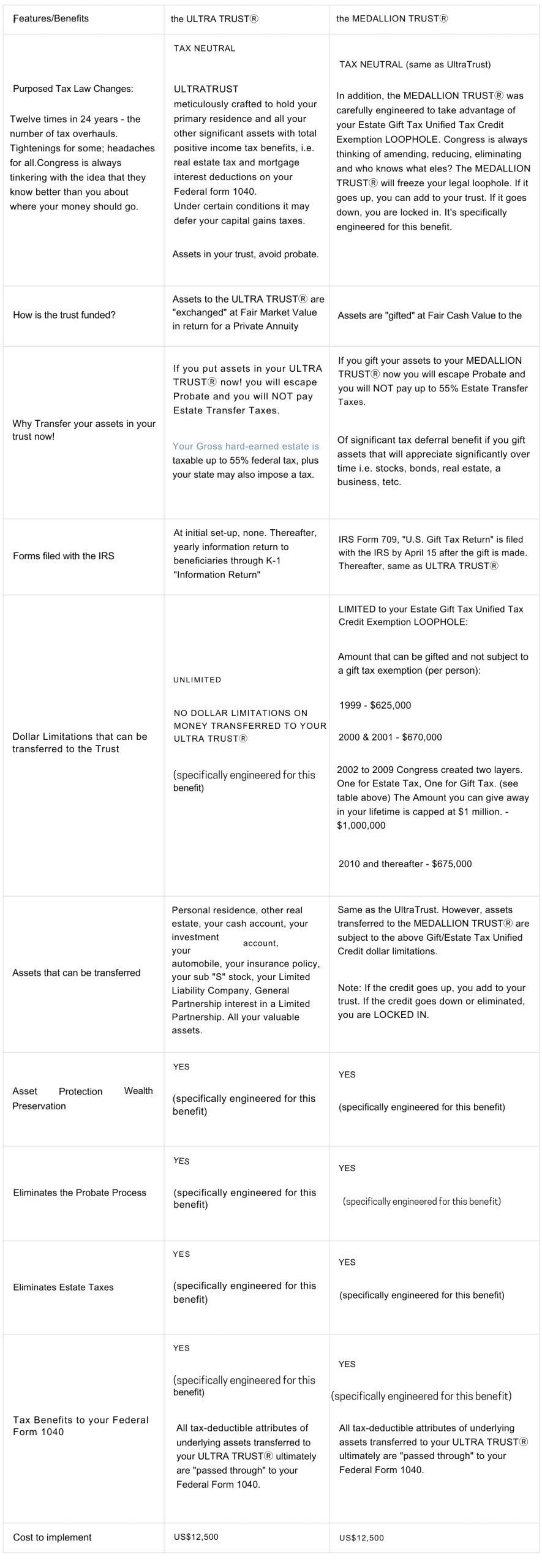

What’s the difference between an UltraTrust® and a Medallion Trust®?

Helpful resources: For added perspective, readers often compare Medicaid Irrevocable Trust, , and official Medicaid eligibility guidance for broader context on the planning choices involved.

Where the next decision becomes clearer

Once Medallion Trust: Irrevocable Trust Asset Protection is on the table, the next questions usually center on risk, flexibility, and which planning step deserves attention first.

Points readers weigh before moving forward

- Timing matters because transfers and look-back rules can change what is possible.

- Funding matters because a trust has to hold the right assets in the right way to work as planned.

- Control matters because Medicaid planning works best when the structure matches the family’s actual care goals.

Practical reading path

To keep the next step practical rather than abstract, readers often move to Medicaid Irrevocable Trust, Irrevocable Trust, and FAQ. When government rules shape the decision, many readers also review official Medicaid eligibility guidance.