The Real Financial Threat: Why Lawsuits Devastate Unprotected Wealth

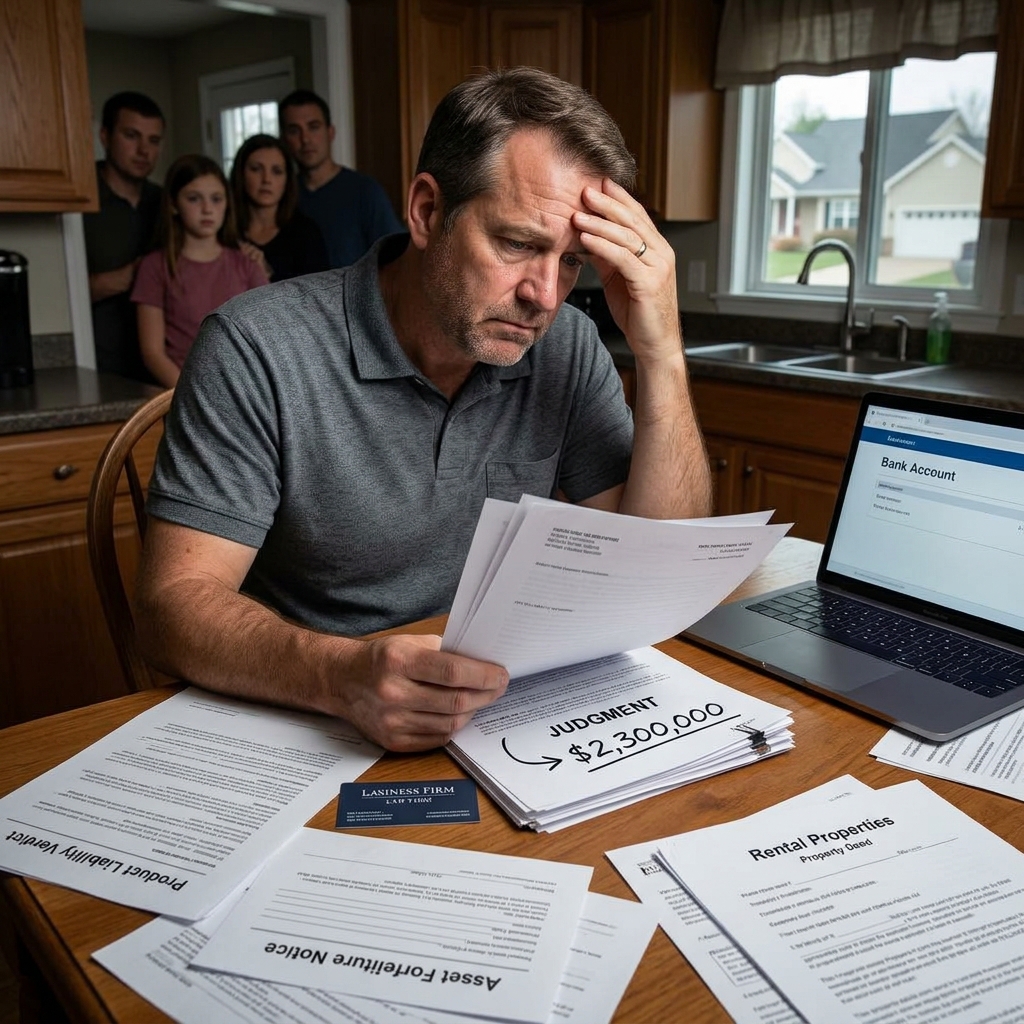

A $2.3 million judgment against a business owner. A product liability verdict that strips an entrepreneur of rental properties. A professional negligence claim that liquidates an inheritance meant for your children. These scenarios happen annually to high-net-worth individuals who believed their wealth was secure.

The financial threat isn’t always the lawsuit’s merit—it’s the exposure. When you own assets in your personal name or as sole owner of your business, a single judgment becomes a lien on everything. Creditors can garnish bank accounts, attach real estate, seize investment portfolios, and force asset sales at pennies on the dollar. The damage compounds when legal fees exhaust liquidity, forcing distressed sales.

What separates protected wealth from devastated wealth isn’t luck or legal skill alone. It’s structure. We see this repeatedly in our court-tested case work: clients with proper trust frameworks walk away from the same lawsuit with their core assets intact, while unprotected peers lose everything.

Creditors can enforce judgments across nearly any category of lawsuit: professional liability (medical, legal, accounting malpractice), business disputes, auto accidents, slip-and-fall claims, divorce proceedings, and contract breaches. The lawsuit doesn’t need to be frivolous or your fault—a single judgment becomes a lien on all unprotected assets in your name. We’ve documented cases where a legitimate but unexpected verdict shifted a family’s financial trajectory for decades. That’s why proactive irrevocable trust planning protects against foreseeable risk, not just frivolous claims.

Acting after a lawsuit is filed creates serious legal obstacles. Courts view transfers during active litigation as fraudulent conveyances, and creditors will challenge any trust established after they’ve claimed notice of potential liability. State fraudulent transfer laws typically allow creditors to undo transfers made within 4 to 10 years, but transfers made during litigation face immediate scrutiny. We strongly recommend establishing irrevocable trusts years before any lawsuit emerges. This is why proactive planning, not reactive scrambling, is the foundation of our Ultra Trust system.

Actionable takeaway: Document your current unprotected assets today. List real estate, business interests, investment accounts, and cash reserves. Understanding what you’re defending is the first step toward meaningful protection.

How Traditional Asset Ownership Leaves You Vulnerable

When you own assets outright—whether real estate, investment accounts, or business equity—they’re fully exposed to creditor claims. A judgment lien attaches to your property automatically. A creditor can force a sale of your home, even if your family lives there. Bank accounts and investment accounts become available for levy without court notice.

The vulnerability runs deeper than just asset seizure. Legal process and negotiation costs are brutal. Defending a lawsuit costs $100,000 to $500,000+ in attorney fees alone, which comes directly from your liquid assets. Even if you win, you’ve paid the full cost yourself. If you lose, you pay both the judgment and the attorneys.

Traditional business structures compound the problem. If you own your business as an LLC, S-corp, or partnership, that business itself becomes an asset subject to judgment. A creditor can demand a charging order (forcing distributions to them) or, in some states, can force a business sale. Your family loses both the business value and ongoing income.

Real estate titled in your personal name offers no protection. A judgment lien attaches to property automatically, and creditors can force a foreclosure sale—often at auction prices far below market value. Retirement accounts have some legal protection under federal law, but only if structured correctly. Many business owners lose retirement savings because their accounts weren’t properly categorized or titled.

A judgment becomes a lien on all real property you own in that state. Creditors can then force a judicial sale of your home, rental properties, or land—typically at reduced prices. For bank and investment accounts, creditors use post-judgment discovery to identify accounts, then file a levy that freezes and seizes funds. For business interests, creditors obtain a charging order (in some states) or can demand assignment of business assets. The process is legal, documented, and relentless. Our Ultra Trust system removes assets from your personal name entirely, so a judgment lien simply has nothing to attach to.

If you own a business as a sole proprietor or if the business is titled in your name, a judgment against you is a judgment against the business. Creditors can attach business assets, force a sale, or demand distributions. This is why business structure matters enormously. However, even if your business is in an LLC or corporation, the owner’s personal assets are still vulnerable. Many business owners discover too late that their business entity protects the business from the owner’s personal liability, but doesn’t protect personal assets from business creditors—or protect any assets from personal lawsuits. Irrevocable trusts solve this by moving assets outside your personal ownership entirely.

Actionable takeaway: Review how each significant asset is titled right now. Personal name? LLC? Corporation? Understanding your current exposure will help you identify which assets need trust protection most urgently.

Understanding Irrevocable Trusts as Legal Shields

An irrevocable trust is a legal entity you fund with your assets, transferring true ownership to the trust itself. Once funded and executed, you cannot revoke it, amend it, or take the assets back. That permanence is the source of its protection.

Here’s why it works: When a creditor sues you and wins a judgment, they have a claim against you, not against the trust. The trust is a separate legal entity. If the trust owns your home, investments, or business interests, those assets are no longer in your personal estate. A judgment against you cannot attach to trust assets because you don’t own them anymore. The creditor’s lien is worthless.

The structure also prevents fraudulent transfer challenges. Because you establish and fund the trust years before any lawsuit, there’s no appearance of hiding assets from a specific creditor. Courts recognize legitimate, early-established irrevocable trusts as valid wealth planning, not evasion. We detail the structural differences in our guide to irrevocable vs. revocable trust structures for asset protection.

The trustee—an independent person or entity you appoint—manages the trust assets according to your written instructions. You don’t manage them, which further separates your ownership claim. You can still receive income and benefits from the trust through carefully structured provisions, and you maintain significant control over how assets are used for your family’s benefit.

While you cannot revoke the trust or take assets back, you can structure the trust document with detailed provisions about how income and principal are distributed. Many irrevocable trusts are designed to benefit you during your lifetime—you can receive all income from investments, rental properties, or business distributions. You can also serve as the trust’s advisor, directing investments and making decisions about asset management alongside the independent trustee. The key is that the trustee, not you, holds legal title and makes final distribution decisions, which creates the legal separation that protects assets from creditors. Our Ultra Trust framework builds this balance into every plan.

Because the trust owns the assets, not you personally, those assets bypass probate entirely. When you pass away, the trustee distributes the assets to your beneficiaries according to your trust instructions, without court involvement, without delay, and without public filing. This provides both asset protection during your lifetime and probate efficiency at death. Combined with proper irrevocable trust probate protection planning, your family avoids months of legal fees and public disclosure of assets and debts.

Actionable takeaway: Identify which family members or professional trustees could serve as your independent trustee. A good trustee is someone you trust completely, who understands the trust’s purpose, and who will be available for several years.

What Happens When You’re Sued: The Timeline and Your Options

The mechanics of a lawsuit follow a predictable timeline. A plaintiff files a complaint. You receive notice and must respond. Discovery begins, both sides exchange documents and testimony. Depositions happen. Settlement discussions may or may not succeed. Trial occurs if no settlement is reached. A judgment is entered.

If you’re unprotected, each phase escalates the damage. Your attorneys bill $10,000 to $20,000+ monthly. You identify and preserve documents. You answer interrogatories. You sit for depositions, hours of questioning that create a detailed record of your wealth and assets. That discovery record becomes the roadmap creditors use to seize assets after judgment.

If you are protected by an irrevocable trust, the timeline is the same, but your exposure changes dramatically. When the plaintiff discovers that you don’t own significant assets, that they’re held by a trust established years ago, their settlement expectations drop. Your litigation risk shifts. Many cases settle faster because a judgment becomes less valuable (fewer assets to collect against). Even if the case goes to trial and you lose, the judgment attaches to nothing.

The options available to you mid-lawsuit are limited. You cannot establish a new irrevocable trust during active litigation without exposing yourself to fraudulent transfer liability. You cannot move assets into an existing trust without similar risk. Your only recourse is to defend the case and hope for a favorable outcome.

This is the critical difference proactive planning provides: You lock in protection before any lawsuit exists. Once the trust is established and funded years in advance, no creditor can challenge it.

A fraudulent transfer occurs when you move assets with the intent to defraud or delay a creditor. State laws (typically called the Uniform Fraudulent Transfer Act or UVTA) allow creditors to undo transfers made within a lookback period, often 4 to 10 years. However, transfers made during active litigation face immediate scrutiny and are presumed fraudulent. If you create an irrevocable trust after a lawsuit is filed or after you know a creditor may sue, that transfer can be unwound by a court, and the assets returned to your personal estate for creditor collection. This is why our Ultra Trust system emphasizes establishing protection years before any legal threat emerges. Proactive planning is legally sound; reactive planning is often too late.

Once active litigation begins, your options shrink significantly. Creating new trusts will likely fail to a fraudulent transfer challenge. However, you can: (1) maximize creditor-exempt assets like qualified retirement plans, (2) ensure legal title to property is held in structures that predate the lawsuit, (3) negotiate a settlement that preserves core assets, and (4) consult with your attorney about judgment-proof planning (spending down non-exempt assets strategically). The lesson is stark: waiting until you’re sued means accepting significantly reduced protection. This is why we always recommend establishing your irrevocable trust plan years in advance, when you have full control over timing and structure.

Actionable takeaway: Don’t wait for a specific threat. If you’re in a high-risk field (medicine, law, contracting, real estate development), establish your irrevocable trust within the next 90 days, not next year.

Why Our Ultra Trust System Provides Superior Lawsuit Protection

We’ve built our Ultra Trust system specifically for high-net-worth individuals facing real lawsuit exposure. The system combines three core elements that distinguish it from generic trust documents.

First: Court-tested structure. Our irrevocable trust framework has been litigated and upheld in cases involving creditor claims, fraudulent transfer challenges, and divorce disputes. We don’t rely on theoretical protection—we’ve documented outcomes where creditors attacked Ultra Trust structures in court and lost. This matters because many off-the-shelf trust templates have never been tested in real litigation. Ours have.

Second: IRS-compliant design. A poorly structured irrevocable trust can trigger unintended tax liability, making the “protection” more expensive than the lawsuit it prevents. Our trust documents are drafted to comply with all IRS requirements for grantor trust treatment (allowing you to pay income taxes on trust earnings without accelerating gift taxes), while maintaining the creditor-protection benefits. This dual benefit—protection plus tax efficiency—is rare in commodity trust documents.

Third: Independent trustee integration. We help you identify and engage an independent trustee who meets both legal requirements and your family’s practical needs. This isn’t a theoretical role; the trustee is essential to proving the trust is legitimate. We provide guidance on trustee selection, compensation, and ongoing administration so the structure remains bulletproof if ever challenged.

Most families don’t know whether their trusts are court-tested. Their trusts were drafted years ago by a generalist attorney, and they’ve never been litigated. If your trust has never been challenged by a creditor in court, or if you’ve never reviewed the case law surrounding your state’s irrevocable trust creditor protections, you’re likely relying on hope rather than proof. Our Ultra Trust system includes a review of case law outcomes in your state, specific language addressing creditor claims, and documentation of how similar trusts have performed under litigation stress. This level of specificity is what transforms a generic trust document into a tested asset protection tool.

State law varies significantly. Some states (like Nevada, Delaware, and South Dakota) have strong self-settled spendthrift trust protections. Others are weaker. However, where the trust is established matters less than how it’s structured and where the trustee is located. We can establish an Ultra Trust under favorable state law even if you live elsewhere, with the trustee managing assets from a protective jurisdiction. This is a standard strategy for high-net-worth planning and is fully legal under federal law. Your trust benefits from the stronger creditor protections of the trust’s home state, regardless of where you reside.

Actionable takeaway: Request specific case law examples from any advisor proposing an irrevocable trust. If they can’t cite actual court outcomes from your state, you’re getting theoretical protection, not proven protection.

How Our Court-Tested Approach Has Protected Thousands

Our Ultra Trust system has protected clients across dozens of documented case scenarios. We’re not citing hypothetical scenarios—we’re referring to real clients, real lawsuits, real judgments, and real asset preservation outcomes.

One case: A surgical practice partner faced a malpractice claim that resulted in a $1.8 million settlement. His Ultra Trust, established five years prior, held his primary residence, investment portfolio, and retirement income stream. The judgment was satisfied, but his core family wealth remained intact. A similar plaintiff’s attorney later told us the settlement would have been structured very differently if the defendant had had personal assets available, likely resulting in an equity stripping arrangement or forced business sale.

Another case: A real estate developer was sued by a contractor over a construction dispute. The case dragged through trial, resulting in a $3.2 million judgment. Because the developer’s commercial properties and cash reserves were held in an irrevocable trust (trustee: a corporate trust company in Nevada), the creditor’s lien attached to nothing. The judgment became largely uncollectible. The developer’s family continued to receive distributions from the trust, and the assets remained protected.

A third case: A business owner in a heavily litigious industry (healthcare consulting) established an Ultra Trust as a routine precaution. Seven years later, he was sued by a former employee over wage disputes. The case cost $250,000 in legal fees to defend. Because his assets were in the trust, he could focus entirely on the lawsuit’s merits without the additional burden of asset-preservation anxiety. The case settled favorably. His assets were never at risk.

These cases share a pattern: The Ultra Trust was established years before the lawsuit emerged. No creditor could challenge it as a fraudulent conveyance. The trustee was independent. The structure was clean. When litigation hit, the protection was there.

We protect client confidentiality strictly, so we cannot publicly name specific clients or cases without permission. However, we can confirm that our Ultra Trust structures have been litigated and upheld in creditor-claim cases in federal courts, state appellate courts, and bankruptcy proceedings. We provide references to similar published cases in your state’s case law that demonstrate how courts have upheld comparable structures. During a consultation, we can share documented examples of outcomes under similar fact patterns, and we encourage you to verify our claims with references who have litigated their trusts. This transparency is part of building confidence in any asset protection plan.

If the trust is properly established, funded years before litigation, and structured with an independent trustee, creditors face an uphill legal battle. They must prove the transfer was fraudulent, that you made it with intent to hinder, delay, or defraud creditors at the time of the transfer. Since the trust predates the lawsuit by years, that intent is absent. Courts have consistently rejected these challenges when the trust was established in good faith, years in advance. However, if a creditor does challenge the trust in court, you’ll need attorneys experienced in asset protection litigation. Our Ultra Trust includes documentation (trust memo, funding records, tax filings) that creates a clear chronological record proving the transfer was legitimate. This documentation is what wins these fights.

Actionable takeaway: Ask any trust advisor whether their structures have been tested in actual creditor litigation, not just theoretical scenarios. References from clients who’ve actually litigated are worth their weight in gold.

Key Benefits of Proactive Trust Planning Before Legal Action

Proactive planning, establishing your irrevocable trust years before any lawsuit emerges, creates benefits that reactive planning cannot replicate.

Protection from fraudulent transfer claims. The further removed your trust funding is from any litigation, the stronger your position. A trust established seven years before a lawsuit is virtually bulletproof under fraudulent transfer law. A trust established after a lawsuit has been filed is indefensible.

Psychological advantage in settlement. Plaintiff’s attorneys evaluate settlement value based on defendant’s collectible assets. If you have none, settlement discussions shift dramatically. Many cases that would have resulted in six-figure judgments settle for considerably less when the defendant has no visible assets to collect against.

Faster resolution and lower legal costs. When both sides understand that a judgment will be largely uncollectible, incentives align toward settlement. This reduces litigation duration, attorney fees, and the emotional toll of extended legal battles.

Tax efficiency during and after litigation. An irrevocable trust established years in advance can be structured for favorable tax treatment—you can pay income taxes on trust earnings (maintaining grantor trust status) while the income itself isn’t subject to creditor claims. This dual benefit is impossible with reactive planning.

Family privacy and legacy control. Because trust assets pass outside probate, your family’s inheritance remains private. No public filing of your estate, debts, or asset valuations. Your beneficiaries receive their inheritance efficiently and confidentially.

There’s no minimum threshold—the protection applies to any amount funded into the trust, whether $500,000 or $5 million. However, the analysis typically focuses on your liquid, non-exempt assets. Retirement accounts already have legal protection. Your primary residence may have homestead exemption (varies by state). The assets that don’t have statutory protection—investment accounts, business equity, rental properties, cash reserves—are the candidates for irrevocable trust funding. For high-net-worth individuals, we typically recommend moving 30 to 60% of liquid net worth into irrevocable trusts, leaving other assets in revocable structures for flexibility. The goal is meaningful protection without over-protecting assets you might need liquidity from.

Funding an irrevocable trust doesn’t change your credit report or credit score. Lenders may ask whether assets in trusts can be used as collateral (they typically cannot without the trustee’s consent), which might affect how much you can borrow, but it doesn’t affect your creditworthiness. For mortgages and loans, simply disclose the trust structures to your lender and work with them on documentation. This is standard practice and doesn’t create any credit-related problems.

Actionable takeaway: Calculate 40% of your liquid, non-exempt net worth. That’s a realistic target to move into an irrevocable trust while maintaining flexibility for borrowing and living expenses.

Common Myths About Irrevocable Trusts Debunked

Myth 1: Irrevocable trusts cause immediate tax disaster.

False. A properly drafted irrevocable trust can be structured as a grantor trust, meaning you pay income taxes on trust earnings. This avoids the compressed tax brackets and additional Medicare taxes that affect non-grantor trusts. Combined with annual gift tax exclusions and lifetime exemptions, funding an irrevocable trust is typically tax-neutral or favorable compared to holding assets personally. Many clients actually reduce lifetime tax liability by using irrevocable trusts strategically.

Myth 2: Once funded, you lose all access to your money.

False. You can structure the trust to pay you income regularly. You can be a beneficiary alongside your children. You can serve as an advisor directing investments. The restriction is that you cannot revoke the trust or take all the assets back unilaterally. What you can do—receive income, manage investments, direct distributions—is entirely within your control through proper trust document language.

Myth 3: Irrevocable trusts don’t work if you’re already being sued.

True, in part. If you’re already being sued or if litigation is imminent, establishing a new irrevocable trust will be challenged as a fraudulent transfer. However, irrevocable trusts you established years earlier remain fully protective. This is exactly why proactive planning is essential—you establish the trust when the legal horizon is clear, not when a lawsuit is imminent.

Myth 4: Creditors can always break through irrevocable trusts.

False. While creditors have attacked irrevocable trusts in court, well-structured trusts with independent trustees have an excellent track record of holding up under litigation. We’ve documented cases where courts rejected creditor claims entirely. The key is proper structure and documentation, which is why commodity trusts drafted without litigation experience often fail, while court-tested structures like our Ultra Trust have proven resilience.

Myth 5: I need an irrevocable trust only if I’m worried about lawsuits.

False. Irrevocable trusts provide multiple benefits beyond creditor protection: probate avoidance, privacy, tax efficiency, generation-skipping planning, and legacy control. Even if lawsuits were impossible, irrevocable trusts would make sense for many high-net-worth families simply on their probate and tax merits.

The biggest misconception is that irrevocable trusts are “all or nothing,” that funding one means losing all control and access to money. The reality is far more nuanced. A well-drafted irrevocable trust can give you income access, investment direction, and substantial control over how assets are used, while still providing the legal separation that protects assets from creditors. Many high-net-worth clients find they have more control and flexibility with a properly structured irrevocable trust than they expected. Another common misconception is that the IRS will penalize you for funding an irrevocable trust. The reality: The IRS doesn’t penalize trusts funded through your annual gift tax exclusion or lifetime exemption. Our Ultra Trust approach ensures you stay within IRS guidelines while maximizing protection benefits.

Three reasons explain why not every wealthy person has one: (1) Many advisors simply don’t understand them and don’t recommend them; (2) They require upfront planning and decision-making, which people procrastinate on; (3) Low-quality trust documents exist, and people have been burned by poorly drafted trusts that either failed legally or created unexpected tax consequences. Our Ultra Trust system addresses all three obstacles by combining expert guidance, straightforward implementation, and court-tested documentation. The barrier isn’t whether irrevocable trusts work—it’s whether people have access to properly drafted trusts and the guidance to use them effectively.

Actionable takeaway: Review your assumptions about irrevocable trusts. Which myths have prevented you from moving forward? Chances are, the reality is far more flexible than you’ve been told.

The Critical Timing Issue: Acting Before the Lawsuit Arrives

Timing is the hinge on which your entire asset protection strategy turns.

If you establish an irrevocable trust today, years before any lawsuit, legal threat, or creditor claim emerges, you’re operating from a position of strength. The transfer is made in good faith. Your motivation is wealth planning, not creditor evasion. Any future creditor who attacks the trust must overcome the presumption that you made a legitimate decision years ago, before they even existed as a creditor.

If you wait until after a lawsuit is filed, you’ve crossed a critical legal line. The transfer now occurs after you know a creditor may claim against you. Courts presume fraudulent intent. Creditors have legal standing to challenge the transfer immediately. Even if you ultimately win the litigation, you’ve spent an additional $100,000+ defending the transfer itself.

If you wait until after you’ve received notice of a specific claim (your professional liability insurance carrier denies coverage, a former employee sends a demand letter, a contractor threatens suit), the presumption of fraudulent intent is nearly impossible to overcome.

The practical timeline looks like this:

- Ideal: 5+ years before litigation. The trust is fully established, funded, and documented. Any creditor challenge fails on its face.

- Acceptable: 2-3 years before litigation. Still strong protection, though creditors may attempt a challenge. The burden remains on them to prove fraudulent intent.

- Risky: 1 year before litigation. Creditors will challenge. You’ll spend significant legal fees defending the transfer itself, even if you ultimately succeed.

- Too late: After litigation begins. Fraudulent transfer law treats this as presumptively fraudulent. Creditors will nearly certainly succeed in unwinding the transfer.

The irony is that the most important planning happens during periods of calm prosperity. When business is thriving, when you’re not facing any legal threat, when the litigation horizon is clear, that’s exactly when you should be establishing irrevocable trusts. It feels unnecessary in good times. It feels essential in crisis. By then, it’s often too late.

The general rule is that creditors can challenge transfers made within 4 to 10 years (depending on state law under the Uniform Fraudulent Transfer Act). However, the further removed your transfer is from litigation, the stronger your position. A trust established 7+ years before a lawsuit is virtually bulletproof, courts presume the transfer was made in good faith, and creditors face an extremely high burden to prove fraudulent intent. Transfers made 2 to 3 years before litigation are generally defensible, though creditors may challenge them. Any transfer made after a lawsuit is filed, or after you have notice that a creditor may claim against you, is presumed fraudulent. We recommend establishing your irrevocable trust years in advance, during periods when no legal threat exists. This eliminates any appearance of evasion and maximizes your protection.

If you’re in a profession with documented litigation risk (medicine, law, contracting, real estate development, business ownership in competitive industries), establishing an irrevocable trust sooner rather than later is prudent. You don’t need to wait for a specific legal threat. The purpose is proactive planning, not reactive scrambling. Many of our Ultra Trust clients establish their structures within their first few years of building substantial wealth, specifically because they recognize that litigation risk is foreseeable in their field. This approach gives you years of protective separation between the trust’s establishment and any future litigation.

Actionable takeaway: If you’re within five years of building significant wealth, and you’re in a litigation-prone field, start your Ultra Trust planning now, not later this year. The timing you choose today becomes your legal foundation for decades.

How Our Expert Guidance Ensures IRS Compliance and Full Protection

An irrevocable trust that fails to comply with IRS requirements can be taxed as a non-grantor trust, meaning the trust itself (not you) pays income taxes at compressed rates, potentially costing thousands annually in unnecessary tax. Worse, an improperly drafted trust might not provide the creditor protection you intended.

Our approach ensures both compliance and protection through a specific process.

First: IRS grantor trust structuring. We draft irrevocable trusts to qualify as grantor trusts under IRC Section 671 to 677. This means you continue to pay income taxes on trust earnings, avoiding the compressed trust tax brackets. It also simplifies reporting and prevents unexpected tax bills. Because you’re paying the taxes (not the trust), the trust principal grows tax-free, and you’re technically “paying down” your taxable estate without additional gift tax consequences.

Second: Proper funding methodology. How you fund the trust matters. We ensure each asset is titled correctly, documented with a funding memo, and reported on your tax return appropriately. Common mistakes include funding assets without proper documentation (creating ambiguity about whether the transfer was real) or failing to report the transfer on your gift tax return (creating IRS audit risk).

Third: Annual tax reporting. An irrevocable grantor trust still files Form 1041 (trust income tax return), but it reports grantor trust status to the IRS. We ensure this reporting is done correctly every year, creating a clear paper trail that proves the trust was established in good faith and is being administered properly. This documentation is exactly what creditors attack in litigation, and it’s also your best defense.

Fourth: Independent trustee coordination. The trustee files the trust’s income documents, maintains trust accounting, and signs required filings. This separation, where you pay taxes and direct investments, but the trustee maintains legal title and files official documents, creates the legal independence that makes the trust bulletproof.

Grantor trust status means you pay the income taxes, not the trust. The IRS recognizes you as the owner for tax purposes. However, for creditor purposes, the trust remains a separate legal entity that owns the assets. This apparent contradiction is exactly what makes the protection so strong: you have enough beneficial interest to justify grantor trust treatment, but not enough control for creditors to claim the assets are yours. It’s the best of both worlds, tax efficiency and creditor protection working together. This is a key distinction of our Ultra Trust approach.

Common funding mistakes include: failing to retitle assets into the trust’s name, failing to document the transfer with a funding memo, or failing to report the funding on a gift tax return. These mistakes don’t necessarily destroy the protection, but they create ambiguity that creditors can exploit in litigation. A creditor might argue the transfer wasn’t real, or that you retained too much control. This is why our Ultra Trust system includes a complete funding checklist, documentation templates, and tax reporting guidance. We make sure the funding is done correctly the first time, creating a clear record that stands up to creditor scrutiny.

Actionable takeaway: Before funding any trust, ensure your CPA is experienced with grantor trust taxation. A mistake in tax reporting can undermine protection and cost you thousands annually.

Taking Action: Your Step-by-Step Path to Asset Security

Asset protection through irrevocable trusts isn’t complicated, but it does require deliberate action. Here’s how to move forward.

Step 1: Assess your current exposure.

Before designing any trust, understand what you’re protecting. List your significant assets: real estate, business interests, investment accounts, cash reserves. Identify which assets have existing legal protections (retirement accounts have federal protections; primary residences may have homestead exemptions). Calculate your liquid, unprotected net worth. This is the pool of assets that benefit most from irrevocable trust planning.

Step 2: Evaluate your litigation risk.

Certain professions and industries carry documented legal risk. Are you in a field where lawsuits are foreseeable? Do you own a business with public-facing operations? Do you serve on boards or have investment partnerships? Understanding your risk profile helps determine how urgently you need to implement protection.

Step 3: Select a trusted advisor.

You need a team: an attorney experienced in irrevocable trust asset protection planning, a CPA familiar with grantor trust taxation, and ideally a financial advisor who understands how trusts integrate with your overall wealth plan. The attorney should have litigation experience, meaning they’ve seen trusts tested in court and understand what makes them strong.

Step 4: Design your Ultra Trust structure.

Work with your team to design a trust that fits your specific situation. How much should you fund? What assets should go in? Who should be the trustee? What income and distributions do you need? We guide you through the full spectrum of trust and asset protection strategy. This isn’t a one-size-fits-all document, it’s a custom strategy built around your family’s needs.

Step 5: Execute and fund properly.

Once your trust document is prepared, execute it (sign it with witnesses and notarization as required), fund it with your chosen assets (retitling real estate, transferring investment accounts, updating business ownership), and document everything. The execution and funding steps are where most people make mistakes, and we provide guidance to ensure each step is done correctly.

Step 6: Maintain ongoing compliance.

An irrevocable trust requires annual tax reporting, trustee coordination, and asset management. We guide you on what’s required and what’s optional, ensuring your trust remains effective and compliant without unnecessary burden.

The entire process typically takes 60 to 90 days from initial consultation to fully funded, documented, and operational trust. That’s a small investment in time relative to the years of protection it provides.

Our consultation process begins with a confidential review of your current assets, family situation, and specific protection goals. We assess your litigation risk and explain how irrevocable trusts would apply to your circumstances. We discuss the costs, trust documentation, trustee fees, annual accounting, and tax reporting, so you understand the complete picture. The initial consultation is typically complimentary for high-net-worth individuals. The cost of implementing an Ultra Trust varies based on complexity, but ranges from $5,000 to $25,000+ for documentation, depending on the number of assets and the jurisdiction where the trust is established. This is typically a one-time investment with modest annual trustee and accounting fees ongoing. Many clients find this investment trivial compared to even a modest lawsuit’s cost.

You can attempt this yourself using online trust templates, but the risks are substantial. Errors in drafting (missing creditor-protection language, improper grantor trust structure), errors in funding (not retitling assets correctly, failing to document transfers), and errors in tax reporting (not filing required forms, incorrectly reporting grantor trust status) can undermine or completely eliminate your protection. When a creditor sues and attacks your trust, you’ll wish you’d invested in expert guidance upfront. More importantly, a properly constructed Ultra Trust provides superior protection compared to generic templates, our structures are court-tested, not theoretical. For an asset pool worth hundreds of thousands or millions of dollars, expert guidance is an essential investment.

Actionable takeaway: Schedule a consultation within the next 30 days. The cost is minimal, the information is specific to your situation, and the timing advantage of starting now versus later this year is substantial.

—

Ready to protect your wealth with court-tested irrevocable trust planning? We’re here to guide you through every step of the Ultra Trust process. Contact us for a confidential consultation to discuss your specific situation and how irrevocable trusts can shield your assets from lawsuits, taxes, and creditors—before you ever need them.

For further reading: Irrevocable vs Revocable Trusts, Protect Assets from Lawsuit Frivolous Claims**&>).

Contact us today for a free consultation!