Generally, people come together to run a business after forming a general partnership. Even though this structure has a number of advantages, it also exposes the partners to risk, particularly personal liability. Lacking general partnership asset protection, debt and obligation of the business may fall on the partners themselves and their assets. In other words, a business founder’s personal assets, like a home, savings accounts, and investment accounts, could be subject to seizure in all of the above liabilities.

Luckily, strategies and tools exist to safeguard your business and personal assets in a general partnership. In this essay about asset protection for general partnerships, we are going to learn its importance, various asset protection strategies, and ways to reduce risks and protect your wealth.

General partnership asset protection is what?

Strategies that safeguard a partnership’s assets from various risks and the partners themselves fall under the category of general partnership asset protection. In a general partnership, most partners are usually personally liable for the debts and obligations of the business. This means the personal assets of the partners could be at risk if there are legal claims against the partnership or if it faces financial difficulty.

Asset protection typically involves establishing a legal entity like a corporation or limited liability company that limits liability, utilizing insurance, and separating business and personal assets. It is to eliminate my personal financial loss while ensuring the business is protected.

Tips on Protecting General Partnership Assets

Liability Protection: In a general partnership, partners have unlimited liability, which means their personal assets can be seized in order to pay the debts of the business. Strategies for asset protection can reduce the risk.

It’s essential to preserve a clear distinction between personal and business assets to protect your own wealth. Combining the two may give your creditors access to your personal assets to pay for your business debts.

Having enough insurance means your business and personal property are protected from lawsuits. Common types of insurance include general liability, professional liability, and workers’ compensation insurance.

One way to protect your personal assets from losses or damages from your business is to convert your general partnership into a limited partnership, a limited liability entity, or another type of entity that protects the partners from liability. A limited liability company (“LLC”) is one option.

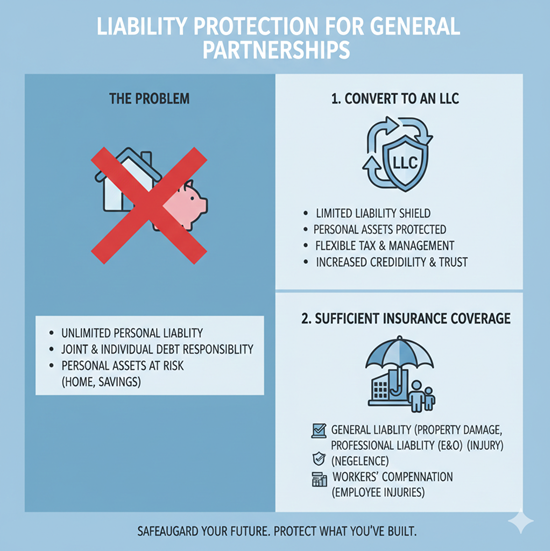

Under a general partnership, protecting personal assets is not possible

Although general partnerships are simple and flexible, they offer limited personal liability protection. With this arrangement, each partner is liable for the actions and debt of the business, meaning their homes and savings could be taken to meet the business’s liabilities. As a result, protecting personal assets is an important issue for general partnerships owners.

You can start an LLC

One of the most common ways to safeguard your personal assets is to convert your general partnership into a limited liability company (LLC). Owners or members of this business LLC do not take on additional liability beyond their investment. The personal assets like homes, cars and savings; are usually shielded against the business’ debts and lawsuits.

An LLC provides a variety of benefits

- LLC members aren’t usually held personally liable for business debts of the LLC.

- The LLC’s structure is flexible. Owners can decide how they wish to be taxed and management options are flexible too.

- Transforming into an LLC can bolster the company’s credibility while additionally assisting it in attracting clients or investors.

Use Sufficient Insurance Coverage

Insurance plays an important role in safeguarding general partnership assets. If you have adequate insurance coverage in place, it can protect your business and personal assets against various lawsuits, property damage and employee injuries. The most common types of insurance include.

- General liability insurance provides protection against claims involving damage to property, bodily injury, or harm to reputation.

- Professional liability insurance – also called errors and omissions (E&O) insurance; safeguards against claims of negligence and malpractice.

- Workers’ compensation insurance protects workers for work-related injuries and illness.

Insurance is not always effective in controlling risks but it definitely helps in managing the financial loss due to an unexpected event or a lawsuit.

Asset Protection Trusts

Another way to protect personal assets from creditors and lawsuits is with an asset protection trust. The trusts enable you to put assets in the control of a trustee which makes the assets somewhat lawsuit-proof. Asset protection trusts work best in jurisdictions with strong trust laws, which can make it difficult for creditors to invade trust assets.

Asset Protection through General Partnership as Compared to Other Business Structures

When it comes to picking the right business structure, it helps to understand the difference between a general partnership and other structures like LLCs and corporations. Notably, choice of structure affects one’s liability and whether personal assets are at risk. A general partnership is contrasted with other popular types of business entities.

| Business Structure | Liability Protection | Taxation | Flexibility |

| General Partnership | Unlimited personal liability | Pass-through taxation (partners report income on personal returns) | High flexibility in management and operations |

| Limited Liability Company (LLC) | Limited liability for owners | Pass-through taxation or corporate taxation options | Flexible management and ownership structures |

| Corporation | Limited liability for shareholders | Corporate taxation, or S-corp pass-through taxation | More complex structure with stricter regulations |

| Sole Proprietorship | Unlimited personal liability | Pass-through taxation (owner reports income on personal return) | Simple, but lacks the flexibility of partnerships and LLCs |

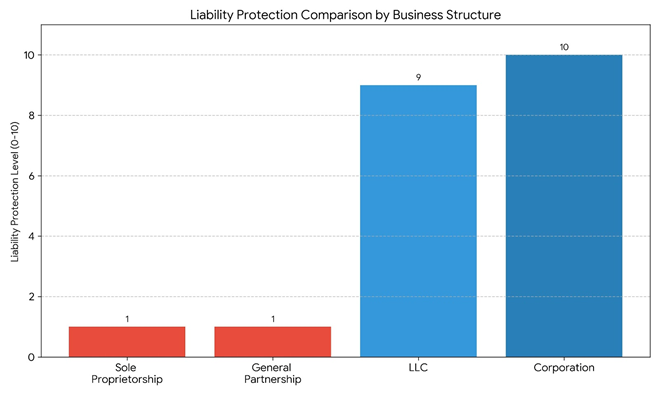

Liability Protection Comparison in Different Business Structures

- A corporation provides the strongest corporate veil, which is the level of protection it provides to its owners against lawsuits.

- LLCs have high shielding as it shields the members of the company for its dbts and other obligations.

- Solo proprietorship owners are the most at risk as they are not legally distinct from their business. Thus, their personal assets like home and savings are fully exposed to business claims.

As seen from the graph and table, general partnership does not offer any protection for personal assets as they have unlimited liability to the business. On the other hand, both LLCs and corporations offer much greater protection for owners’ assets. LLCs are particularly advantageous for individuals seeking a combination of liability protection and management flexibility.

How to Protect Assets in a General Partnership

There are a number of practical things you can do if you run a general partnership that may help protect its assets – as well as your own.

Separate Your Personal Finances from Your Business Finances: Have two separate bank accounts and two separate credit cards and do not use your business credit card for your personal expenses or vice versa. This will act as a shield for your individual assets against creditors in case business snags up.

If your business is still organized as a general partnership, consider converting to an LLC. This is one of the best ways to shield your personal assets. The limited liability of an LLC can protect your personal wealth from the liabilities of business.

Make sure that you have an adequate insurance policy in place such as general liability, professional liability, and workers’ compensation among others. Review your insurance on a regular basis to help with your business’ risks.

If your business is facing a high level of risk, consulting with an asset protection attorney can help you develop a personalized plan to protect your personal wealth. Lawyers can help establish legal structures like trusts or LLCs to minimize exposure to lawsuits and creditor claims, and they can provide advice on how to do so.

Safeguard your business and personal assets

To conclude the discussion, the protection of assets against liability of general partnerships is necessary. Ultra trust If the business gets sued or does not have enough money to pay creditors, your personal assets might be at risk. By identifying the risk and using the right strategies such as proper business insurance, LLC conversion, Liens, and Asset Protection trusts you can keep the money you make.

If you’re in the early stages of starting a business or are operating one as a general partnership, asset protection is essential. When you take the right steps to reduce your risks, you will have peace of mind and focus on growing your business without fear of losing your private wealth.