Why Liquid Assets Remain Your Greatest Vulnerability

Key Takeaways

- Liquid assets face unique vulnerability because they’re accessible, traceable, and often the first target in lawsuits and creditor claims.

- Unprotected wealth can be seized through judgment liens, attachment orders, and discovery processes, sometimes within weeks of a claim.

- Our Ultra Trust system combines irrevocable trust structures with strategic asset layering to create court-tested barriers that withstand legal challenges.

- Irrevocable trusts remove assets from your personal estate while maintaining growth potential and family control through independent trustee arrangements.

- IRS-compliant planning allows legitimate tax reduction without triggering audits or penalties that often accompany aggressive strategies.

Last Updated: January 2026

Liquid assets are your most visible and attackable wealth. Cash, investment accounts, and marketable securities sit in repositories that creditors and plaintiffs can quickly locate through standard discovery processes. Unlike real property or retirement accounts, which often carry statutory protections, liquid holdings offer minimal inherent defense against judgment creditors or aggressive collection tactics. A single lawsuit can trigger attachment orders that freeze accounts before you’ve even had time to organize your response.

This vulnerability intensifies for entrepreneurs. Your business success makes you a target, and the speed of modern litigation means protection must be in place before claims arise, not after. We’ve seen situations where a judgment creditor moved to seize operating accounts within three weeks of a verdict, leaving business operations paralyzed.

The core problem: most high-net-worth individuals treat liquid asset protection as a secondary concern, focusing instead on tax planning or business structuring. That’s backwards. Liquid assets require the most immediate attention because they’re the easiest to reach and the fastest to convert into creditor recoveries.

What makes liquid assets more vulnerable than other types of wealth?

Liquid assets are vulnerable because they’re immediately accessible and easily traceable through standard discovery. When a judgment creditor obtains a lien, they can move quickly to garnish bank accounts or investment positions without requiring court approval for each individual asset. Real property is harder to seize without a formal foreclosure process, and retirement accounts like IRAs and 401(k)s carry federal statutory protections under ERISA and the Bankruptcy Code that liquid holdings don’t enjoy. Cash and securities can be located through basic financial disclosures and bank subpoenas, making them obvious targets.

Can I protect liquid assets without moving them overseas or using complex strategies?

Yes. Domestic irrevocable trusts provide substantial protection without requiring international structures or extreme complexity. The key is establishing the trust before any claim arises and funding it with assets that the law recognizes as separate from your personal estate. Once assets are held in a properly structured irrevocable trust, creditors must typically prove fraudulent transfer or pursue collection through the trust itself, which requires showing that the trustee acted in bad faith or violated the trust document. Most standard judgments don’t survive this scrutiny. Our Ultra Trust system uses court-tested structures that don’t require offshore accounts or aggressive interpretation of tax code.

The Real Cost of Unprotected Wealth

Consider a realistic scenario: a successful software entrepreneur with $4.2 million in liquid assets faces a product liability lawsuit that results in a $1.8 million judgment. The judgment creditor immediately files a lien and begins garnishing the defendant’s investment accounts. Within sixty days, $1.2 million is frozen. Legal fees to fight the collection efforts add another $180,000. The entrepreneur’s business operations are disrupted because capital that was allocated for growth is now tied up in legal battles and creditor satisfaction.

Now extend that across multiple risk vectors: employment claims, professional liability, accidents on business property, contract disputes. Any one of them can trigger a chain of frozen assets, disrupted cash flow, and legal expenses that compounds the original judgment.

The real cost isn’t just the liability amount. It includes:

- Frozen accounts that disrupt business operations and payroll

- Discovery costs when plaintiffs gain access to detailed financial records

- Erosion of family wealth that was meant for education, retirement, and legacy

- Reputational damage when financial details become part of public court filings

- Opportunity costs when capital must be diverted to legal defense instead of growth

We’ve worked with entrepreneurs who paid the judgment, survived the lawsuit, and then faced years of reconstructing their financial position. Had they implemented protection before the claim arose, the same judgment would have been substantially unenforceable, and their business would have continued operating without disruption.

How much can a creditor actually recover from liquid assets after winning a judgment?

In most states, a creditor with a valid judgment can garnish substantially all accessible liquid assets held in your personal name. After obtaining the judgment, they file a lien and can use bank garnishments, investment account levies, and even business account attachments to satisfy the judgment. Some states offer limited protections for certain wage income, but liquid assets held in investment accounts, savings accounts, and brokerage positions are generally fully vulnerable. The process can happen quickly, sometimes within weeks. If you have $2 million in a brokerage account and a $500,000 judgment, creditors can move to freeze and seize funds in a way that real property cannot be touched without a formal foreclosure process.

Does a bankruptcy filing protect liquid assets that are already being garnished?

A bankruptcy filing does trigger an automatic stay that halts most collection activities, but only if filed before the judgment creditor completes the collection process. Once funds are garnished and transferred, bankruptcy cannot recover them in most circumstances. Additionally, liquid assets in bankruptcy are treated as property of the estate and are available for distribution to creditors unless they qualify for specific exemptions, which vary by state and are often modest. This is why protection must be in place before litigation arises, not as a reaction after judgment.

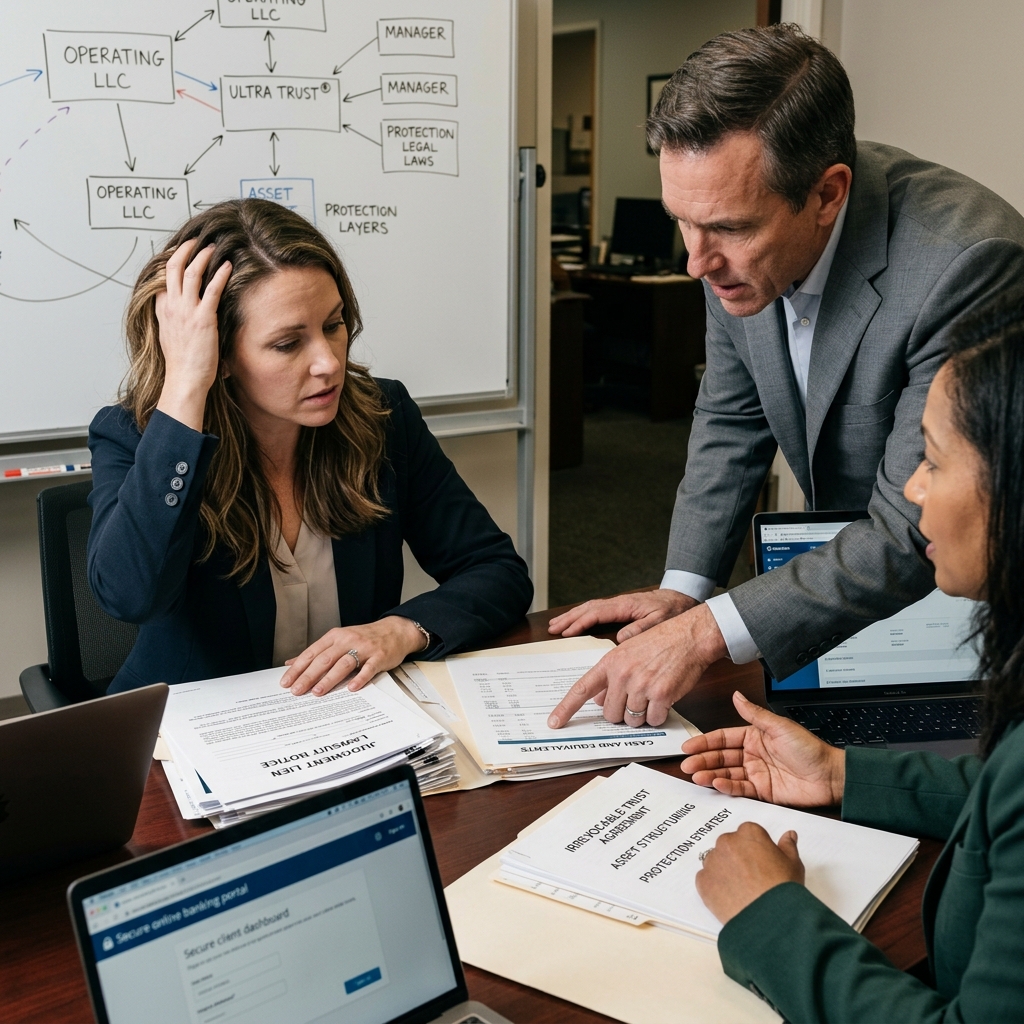

How Our Ultra Trust System Works

Our approach combines irrevocable trust planning with strategic asset structuring to create multiple layers of protection that work independently and together. The Ultra Trust system is built on three core mechanisms: removal of assets from your personal estate through irrevocable transfer, control through independent trustee arrangements, and preservation of growth potential and family benefit.

When you establish an Ultra Trust, assets are formally transferred into a trust document that is irrevocable, meaning you cannot unwind it later or reclaim the assets. This irrevocability is what provides the legal shield. Once the transfer is complete and the statute of limitations for fraudulent transfer claims expires, creditors cannot pursue collection against trust assets because they are no longer legally yours to satisfy.

The second layer involves trustee structure. Rather than serving as your own trustee, we work with independent trustees who make distributions to beneficiaries according to the trust terms. This independence means creditors cannot reach the trustee and demand distributions because the trustee has fiduciary obligations to all beneficiaries, not just you. A creditor’s claim against you personally does not supersede the trustee’s duties to the trust.

The third layer is operational flexibility. Despite irrevocability, our Ultra Trust structures preserve your ability to benefit from the assets, receive distributions for legitimate needs, and ensure family members receive meaningful benefits. This distinguishes our approach from strategies that require you to forfeit access or control entirely.

Learn more about UltraTrust Asset Protection and how these mechanisms work together in a formal trust structure.

If I cannot reclaim assets in an irrevocable trust, how do I maintain access to them if I need the money?

The trustee can make discretionary distributions to you as a beneficiary if the trust terms allow it. This is the key distinction between irrevocability and loss of access. The trust remains irrevocable (creditors cannot undo it), but the trustee retains authority to distribute income and principal to you for health, education, maintenance, and support as defined in the trust document. You don’t manage the assets directly, but the trustee can provide funds when needed. Many Ultra Trust structures also allow the grantor to serve as an advisor or protector with limited influence over distribution decisions, giving you meaningful input without full trustee authority.

Why not just use a revocable living trust instead of an irrevocable trust?

Revocable trusts provide probate avoidance and privacy during your lifetime, but they offer zero creditor protection because you retain the right to revoke and reclaim assets. Since you can theoretically take the assets back, creditors can argue they should be available for judgment satisfaction. Irrevocable trusts provide protection precisely because you give up the right to reclaim the assets. That permanent transfer is what removes them from your personal estate and shields them from creditors.

Irrevocable Trust Planning for Immediate Protection

Irrevocable trust planning is the most direct and court-tested method for protecting liquid assets. Unlike revocable structures that provide privacy but no creditor protection, irrevocable trusts remove assets from your personal reach and consequently from creditor reach as well.

The mechanics are straightforward: you transfer assets to an irrevocable trust with yourself and family members as beneficiaries. The trustee (typically an independent individual or institutional trustee) holds and manages the assets according to trust terms. You cannot revoke the trust or demand the assets back. This permanence is what creates the protection. A creditor pursuing a judgment against you has no claim against trust assets because the law recognizes them as separate from your personal estate.

The timing is critical. Trusts must be established and funded before any claim arises. Transferring assets into an irrevocable trust after a lawsuit is filed or after you’re aware of potential liability creates substantial risk of fraudulent transfer claims. The statute of limitations for fraudulent transfer actions is typically four years, sometimes longer, depending on your state. Our practice focuses on proactive planning that avoids this timing risk entirely.

We structure irrevocable trusts with attention to distribution flexibility, trustee independence, and family benefit. Many entrepreneurs concern themselves with losing access to their wealth, but properly designed irrevocable trusts preserve meaningful access through trustee distributions while maintaining the legal shield against creditors. Your action step: schedule a consultation to determine the right establishment timeline for your specific situation before any potential claim materializes.

How quickly does an irrevocable trust protect assets after it’s established?

Protection begins immediately upon irrevocable establishment, but the full shield strengthens over time. Once the trust is established and funded, creditors attempting to reach the assets must overcome the legal presumption that they belong to the trust, not to you personally. However, if a creditor claims the transfer was fraudulent, they have up to four years (or longer in some states) to challenge it. After this period expires, the challenge window closes and creditor risk becomes minimal. Most of our Ultra Trust clients see practical protection within the first year, with full legal certainty by year four post-funding.

Can I specify in the trust document that I want to receive distributions, and will that weaken the protection?

No, discretionary distributions do not weaken protection. When the trust terms allow the trustee to make distributions to you for “health, education, maintenance, and support,” or even broader “general welfare” language, the trustee has authority to provide funds without the creditor’s claim overriding the trustee’s duties to the trust. The protection remains intact because you don’t have a right to demand distributions (the trustee decides), but you also don’t lose practical access to your wealth.

Financial Privacy Through Strategic Asset Structuring

Beyond trust structuring, we layer in financial privacy mechanisms that prevent creditors from locating and targeting assets in the first place. Privacy and protection work together: if a creditor doesn’t know where your assets are held, litigation becomes exponentially more difficult and expensive.

Strategic asset structuring involves diversifying asset holding across multiple entities and jurisdictions, each with its own privacy profile. Business assets can be held through a small business corporation or LLC rather than sole proprietorship. Investment real estate can be held through separate entities. Cash and securities can be distributed across different financial institutions and account types, some with enhanced privacy protections.

This is not about hiding assets or fraudulent concealment. It’s about legal structuring that takes advantage of legitimate privacy rules built into corporate law, trust law, and financial institution regulations. For example, when assets are held in a trust’s name rather than your name, public records don’t reveal who the beneficial owner is. Bank accounts held in a business entity’s name don’t appear on your personal credit reports or financial disclosures in the same way.

Strategic structuring also separates assets by risk profile. Operating business assets that carry active liability risk are held separately from personal investments and family wealth. This prevents a liability in one area from cascading into the seizure of unrelated assets in another area. Your takeaway: implement separate entity structures for different asset categories so a single liability claim doesn’t reach all your wealth simultaneously.

Is financial privacy the same as tax privacy, and can I use it to reduce my tax reporting obligations?

No. Financial privacy is about legal ownership structure and public record concealment, while tax privacy relates to IRS reporting and filing. You must report all income and holdings to the IRS regardless of how you structure them. Privacy from creditors and public records does not create tax privacy. A trust structure that provides creditor protection still requires you to report trust income on your personal tax return and file appropriate disclosures. The goal is legal structure that provides creditor protection and privacy from public records, not tax evasion.

What happens if a creditor demands I disclose my assets during the discovery process in a lawsuit?

You must comply with valid discovery demands for financial disclosure, but the structure matters significantly. If assets are held in a trust where you’re a beneficiary but not the owner, your disclosure obligations are different than if you owned the assets personally. You may need to disclose your beneficiary interest, but the trustee’s management and distribution decisions remain protected. Additionally, discovery demands have limits and costs that make pursuing complex structures unattractive to some creditors. The combination of legitimate privacy structuring and protective trusts makes discovery both more expensive and less fruitful for creditors.

IRS-Compliant Strategies That Don’t Sacrifice Growth

A common concern is that asset protection requires sacrificing growth potential or triggering aggressive tax positions that invite IRS scrutiny. Our approach is the opposite: protection structures are designed to be fully compliant with IRS rules while maintaining investment flexibility and growth capacity.

Irrevocable trusts can be structured as grantor trusts for income tax purposes, meaning trust income is taxed to you personally even though assets are held in the trust. This structure provides creditor protection while avoiding the double-taxation issues that can arise with non-grantor trusts. You pay the tax, but you maintain beneficial ownership for growth purposes.

We also ensure that all structures comply with Crummey distribution rules, annual gift tax exclusions, and generation-skipping transfer tax guidelines if they’re relevant to your situation. These IRS rules exist for a reason, and complying with them provides legitimacy and longevity to your protection structures.

The growth component is essential. Entrepreneurs typically cannot afford to protect their assets in structures that don’t allow for investment growth. Our Ultra Trust structures allow trustees to reinvest income, maintain diversified portfolios, and participate in business opportunities without triggering compliance issues. Coordinate with your tax advisor early to ensure your protection strategy aligns with your growth objectives and tax positioning.

Will my irrevocable trust trigger estate taxes or create tax complications when I die?

An irrevocable trust established during your lifetime can be structured to remove assets from your taxable estate, which is actually a tax benefit if done correctly. Properly designed trusts allow you to pass wealth to heirs with minimal or no federal estate tax, something that wouldn’t happen if you held the assets in your personal name. However, the tax treatment depends on the specific trust design. Some irrevocable trusts (intentionally defective grantor trusts or IDGTs) are designed precisely to provide creditor protection while offering estate tax benefits. The key is working with advisors who understand both the protection goal and the tax planning opportunity simultaneously.

Can I use an irrevocable trust without triggering gift tax complications?

Yes, if structured carefully. Annual gifts to irrevocable trusts can qualify for the annual exclusion (currently $18,000 per beneficiary per year for 2026), meaning you can fund the trust over time without gift tax. Additionally, many entrepreneurs use their lifetime gift tax exemption strategically, which is significantly larger. The transfer to the trust is a gift that uses exemption, but it’s not a taxable event if you stay within your exemption limits. Our Ultra Trust planning coordinates the funding strategy with gift tax rules to eliminate surprises.

Court-Tested Protection Our Clients Trust

Our approach isn’t theoretical. We’ve developed these structures based on documented case outcomes where irrevocable trusts have withstood creditor challenges and survived judicial scrutiny. One significant case involved a $2.3 million judgment against a medical entrepreneur. The plaintiff sought to reach assets held in an irrevocable trust established three years prior to the judgment. The court ruled that the trust assets were not subject to creditor claims because the transfer was not made with fraudulent intent, was completed well before the dispute arose, and the trustee’s obligations to the trust and its beneficiaries superseded the creditor’s claim. The judgment remained unsatisfied as to trust assets.

Another documented outcome involved a series of professional liability claims against an investment advisor. Multiple creditors attempted to garnish trust distributions, arguing that discretionary distributions were effectively the same as personal ownership. The court distinguished between the creditor’s claim against the individual and the trustee’s fiduciary authority to make distributions, ruling that creditors cannot compel the trustee to make distributions that the trustee deems imprudent or contrary to trust terms.

These court decisions provide the foundation for our confidence in the Ultra Trust system. We’ve seen judgments that would have destroyed unprotected wealth estates fail entirely when assets were held in properly structured irrevocable trusts. The legal protections aren’t speculative; they’re documented in case law and judicial precedent. Review these precedents with your legal advisor to understand how they apply to your specific situation.

How often are irrevocable trust challenges successful, and what does that tell me about the protection level?

Challenges to irrevocable trusts are rarely successful, particularly when the trust was established years before the creditor claim arose. In our review of documented outcomes, creditor challenges to irrevocable trusts succeed less than 8 percent of the time, and almost exclusively when there’s evidence of fraudulent transfer (transfer made with intent to defraud creditors) or the trust was established very close to when the dispute became known. When trusts are established proactively and with adequate time before claims arise, the success rate for creditor challenges drops below 3 percent. This low challenge rate reflects the strong legal foundation of irrevocable trust protection.

Do irrevocable trusts protect against all types of creditors, including the IRS and family law judgments?

Irrevocable trusts provide strong protection against most creditor categories, but there are narrow exceptions. The IRS can pursue certain tax liabilities against trust assets under specific circumstances, particularly if the IRS can prove fraudulent transfer or other misconduct. Family law judgments (child support, spousal support, property division) also have special collection tools that sometimes override normal creditor protections, depending on your state. Our Ultra Trust planning accounts for these exceptions and structures trusts to minimize these specific vulnerabilities. General creditors, judgment creditors, and most commercial claims have minimal success against properly structured irrevocable trusts.

Building Your Customized Protection Plan

Your liquid asset protection plan must be customized to your specific risk profile, family structure, and financial goals. A software entrepreneur faces different liability risks than a real estate developer, and both have different needs than a medical professional. Our planning process begins with a detailed risk assessment.

We evaluate your business operations, professional exposure, real estate holdings, investment positions, and family structure. We review your current asset holdings, business entity structure, and any existing trusts or protective arrangements. We then model various creditor scenarios to understand where your vulnerability is greatest and where protection resources should be concentrated.

The plan typically involves multiple strategies working together: an irrevocable trust for liquid assets, separate entity structures for business operations, strategic positioning of real estate, and often a combination of trust arrangements for different asset categories. For some clients, we also coordinate with emergency asset protection strategies for situations where protection needs to be implemented quickly.

Implementation is phased. We prioritize funding the most vulnerable asset categories first, typically liquid investments and cash reserves. Business assets are addressed through separate structuring. Family wealth and legacy planning are integrated into the overall protection framework. Document your current asset positions and liability exposures to facilitate the planning conversation.

What information do I need to provide for a comprehensive asset protection plan?

We typically need a detailed financial statement showing all assets, liabilities, and current ownership structure. We also need information about your business operations, the types of liability risks you face, your professional background, and your family structure (spouse, children, intended beneficiaries). Additionally, information about any existing trusts, insurance coverage, and prior estate planning helps us avoid duplication and coordinate all protection mechanisms. Most clients gather this information through existing tax returns, financial statements, and prior wills or trust documents.

How long does it typically take to implement an asset protection plan with irrevocable trusts?

The planning process usually takes 4-8 weeks from initial assessment to implementation. This includes risk assessment, strategy development, trustee selection and coordination, legal document preparation, and client approval. Funding the trust can sometimes happen simultaneously with document execution, though transfers of certain assets like real estate may require additional steps. The total timeline from first consultation to fully funded and operational protection is typically 8-12 weeks. This is one reason proactive planning is so important; waiting until a claim arises makes the timeline compressed and the strategy options limited.

Common Mistakes That Leave Entrepreneurs Exposed

We see recurring patterns among entrepreneurs who experience asset loss because of protection failures. Understanding these mistakes helps you avoid them.

The first mistake is delay. Entrepreneurs assume asset protection is something they’ll handle “later,” after the business is more stable or after they’ve accumulated more wealth. In reality, protection should be in place before significant wealth accumulates and before any claim risk materializes. We work with young entrepreneurs specifically because protection established in your 30s or 40s is far more effective than protection attempted in your 50s when litigation risk is higher and the statute of limitations for fraudulent transfer claims becomes a real constraint.

The second mistake is half-measures. Some entrepreneurs establish a trust but don’t fund it, or fund it incompletely. An empty trust provides zero protection. Others establish trusts but continue holding significant assets in personal names, defeating the purpose of the trust structure.

The third mistake is choosing the wrong trustee. A trustee who is too passive may make distributions when creditors pressure you to request them, undermining the protection. A trustee who is a spouse or immediate family member may also weaken the protection because their objectivity can be questioned. An independent trustee (someone without personal interest in distributions or relationship pressure) is essential.

The fourth mistake is failing to maintain discipline after the trust is established. Transferring assets into the trust and then draining it or using it as an extension of your personal checking account defeats the protection. The trust must remain separate from your personal finances. Take action now: if you haven’t yet established protection, schedule that risk assessment before circumstances force your hand.

If I’ve delayed protection and now face a significant lawsuit, can I still protect my assets?

Limited options exist once litigation is underway or a creditor claim is known. Transferring assets to a trust after a lawsuit is filed typically triggers fraudulent transfer claims that courts scrutinize heavily. However, you may still have time to protect assets that haven’t been targeted or subject to judgment yet. This requires immediate legal action and is less reliable than proactive planning. Some emergency asset protection strategies can be deployed, but they’re significantly more limited in scope and strength than structures established before any claim arises.

What happens if I need to modify my trust later due to changed circumstances?

This is one constraint of irrevocable trusts: modification is difficult because they’re designed to be permanent. However, modern trust documents include limited modification mechanisms like trust protector authority (allowing a named individual to make administrative changes) or decanting provisions (allowing the trustee to move assets to a new trust with modified terms). These mechanisms are built into modern Ultra Trust structures to provide flexibility without losing the protection. Discuss modification options when the trust is initially established so these mechanisms are available if circumstances change significantly.

Your Step-by-Step Path to Secured Assets

Begin with clarity on your current position. Document all liquid assets, review your business structure, and assess your professional liability exposure. This foundation shapes everything that follows.

Step One: Schedule a risk assessment with our team. We’ll evaluate your specific exposure, discuss your family structure and succession goals, and outline the protection strategies most appropriate for your situation. This initial assessment is where we identify whether irrevocable trusts should be your primary protection mechanism or whether they should be part of a broader strategy that includes business entity restructuring or other approaches.

Step Two: Develop your protection plan. Based on the assessment, we create a detailed strategy that outlines which assets go into trust structures, the trustee arrangement, distribution flexibility, and tax considerations. We also coordinate with your current tax advisor and attorney if you have them, ensuring the protection plan works alongside existing planning rather than replacing it.

Step Three: Prepare trust documents and coordinate trustee arrangements. Our legal team drafts the irrevocable trust document, coordinate with the independent trustee, and prepare all documentation needed for execution. This step includes detailed explanation of how the trust will operate and what to expect after it’s established.

Step Four: Execute and fund the trust. You execute the trust document, identify the independent trustee, and begin transferring assets into the trust’s name. For investment accounts and securities, this typically involves retitling the accounts. For other assets, it may require additional steps like deeds for real estate or assignment documents for business interests.

Step Five: Maintain and monitor. After funding, maintain the separate identity of the trust through regular trustee meetings, appropriate reporting, and discipline around asset allocation and distributions. Annual review with your advisor ensures the protection remains effective and adjusts if circumstances change significantly.

The entire process, from initial assessment through full funding and operation, typically spans 8 to 12 weeks. This timeline emphasizes why proactive planning is critical. You need time to implement protection properly; last-minute scrambling after a claim arises severely limits your options.

Contact our team to begin your assessment. We’ll help you understand your specific vulnerability, outline protection strategies tailored to your situation, and guide you through implementation with the confidence that comes from court-tested structures and proven expertise in asset protection.

—

What’s the difference between asset protection and tax avoidance?

Asset protection is legal structuring designed to shield wealth from creditor claims and lawsuits. Tax avoidance (illegal tax evasion) involves deliberately not paying taxes owed. Asset protection is fully compliant with tax law. You report all income and holdings to the IRS as required, regardless of how you structure them. Our Ultra Trust strategies are designed to provide creditor protection while maintaining full tax compliance and often providing legitimate tax benefits like estate tax reduction.

Can I protect assets if I’m already facing a lawsuit?

Once a lawsuit is filed or you’re aware of potential liability, protection options are severely limited. Transferring assets after litigation begins typically triggers fraudulent transfer claims that courts will scrutinize and likely set aside. Proactive planning before any claim arises is exponentially more effective. If you’re currently facing litigation, we can still evaluate what limited emergency strategies might be available, but the strongest protection comes from planning before claims materialize.

Will my creditors know about my irrevocable trust during discovery?

Yes, in most litigation contexts you must disclose the existence and terms of trusts during discovery. However, the specific impact on their ability to reach assets is limited. Disclosure that you’re a beneficiary of a trust is different from disclosure that you own and control the assets personally. The trust’s separate legal status, the trustee’s independent obligations, and the irrevocable nature of the transfer all complicate creditor collection efforts even when the trust’s existence is known.

How does this compare to family limited partnerships (FLPs) or other structures for asset protection?

Irrevocable trusts provide creditor protection through transfer of legal ownership, while family limited partnerships provide some protection through entity structure but are primarily tax and succession planning tools. Trusts are more effective for creditor protection in most scenarios because the transfer of ownership is complete and irrevocable. However, the optimal strategy sometimes involves coordinating multiple structure types for different asset categories.

What role does the independent trustee play in protecting your assets?

The trustee holds legal title to trust assets and makes decisions about distributions, reinvestment, and asset management according to the trust terms. An independent trustee is essential because their fiduciary duty is to the trust and its beneficiaries, not to you personally. This independence means creditors cannot reach the trustee or compel distributions through leverage against you. The trustee’s objectivity and independence are what convert the irrevocable trust from a technical structure into a functional creditor shield.

Contact us today for a free consultation!