The Growing Threat: Why High-Net-Worth Individuals Face Creditor Lawsuits

- High-net-worth individuals face elevated creditor risk from business disputes, professional liability, and personal lawsuits; standard insurance alone cannot fully protect concentrated assets.

- Irrevocable trusts legally remove assets from your personal estate, making them inaccessible to creditors since you no longer own them in your individual name.

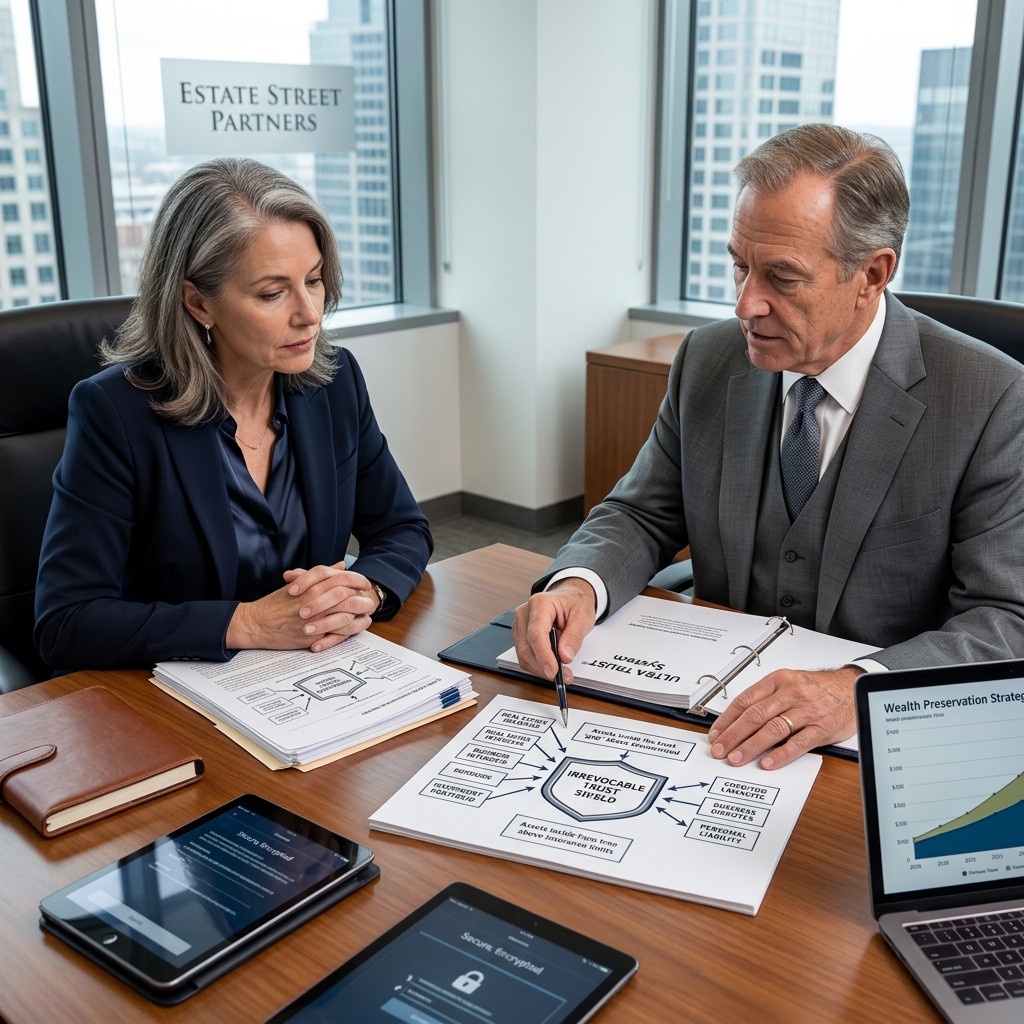

- Our Ultra Trust system combines irrevocable trust structures with tax optimization and privacy layers, designed for court-tested protection across multiple litigation scenarios.

- Multi-layer strategies that coordinate trusts, entity structures, and titling create redundancy that creditors cannot pierce through standard legal action.

- Improper trust setup, delayed planning, and inadequate independence between trustee and grantor remain the most common vulnerabilities that courts have exploited.

Last Updated: January 2026

Wealthy entrepreneurs and families face a creditor risk profile that most middle-class households never encounter. A successful business owner, medical professional, or investor becomes a target not only for legitimate disputes but for opportunistic litigation seeking deep pockets. One employment lawsuit, a contract disagreement with a former partner, or even a personal auto accident can trigger a six or seven-figure judgment against someone with visible assets.

The courts report that judgments against high-net-worth defendants have grown substantially in recent years. Business disputes, professional liability claims, and personal injury settlements increasingly target personal wealth when business insurance caps are exceeded. Unlike a typical employee with limited liquid assets, a business founder or real estate investor holds obvious targets for plaintiffs’ attorneys working on contingency.

The traditional response—hoping insurance will cover everything—leaves significant gaps. Most commercial liability policies have caps well below total net worth. Umbrella policies add another layer but are not bulletproof and typically exclude certain business exposures.

Question: What types of creditors pose the biggest threat to high-net-worth individuals?

Creditor risk varies by profession and business structure, but the most common threats are judgment creditors (from lawsuits), IRS liens (from tax disputes), business creditors (from company guarantees), and personal loan lenders. For business owners, a single jury verdict or settlement in a product liability or employment case can reach millions. Professional liability claims against doctors, lawyers, and accountants follow similar patterns. The IRS holds unique power because it can place liens on all assets and income without a civil judgment. Unlike a consumer debtor, a high-net-worth individual typically has co-signed loans, personal guarantees on business debt, and cross-collateralized real estate—each creating a separate avenue for creditor attachment.

Question: How does a creditor actually access assets during a lawsuit?

Once a judgment is entered, the creditor initiates post-judgment discovery and asset execution. They file a judgment lien against real property, which clouds title and forces a sale. They garnish bank accounts, demand disclosure of investment accounts, and pursue turnover orders if assets are hidden. The creditor’s attorney will depose you regarding your assets and income under oath. This is why visible ownership matters: if your real estate, investments, and liquid accounts are titled in your personal name, they are immediately subject to levy. An irrevocable trust removes that accessibility because the trust, not you, is the owner of record. A creditor cannot force a trustee to liquidate trust assets to satisfy a judgment against a former owner who transferred the assets years before the lawsuit arose.

Why Traditional Insurance and Banking Strategies Fall Short

Insurance coverage is essential but incomplete. A $2 million umbrella policy sounds substantial until a jury returns a $5 million verdict. That gap is your personal liability. Even within policy limits, most insurance requires the insured (you) to remain a named defendant, creating legal fees and reputational damage that no policy reimburses.

Bank account diversification and offshore accounts create operational headaches without legal protection. Once a creditor knows an account exists, they can pursue it through court orders. Hiding assets or lying under oath transforms a civil dispute into a criminal matter. The legal protection must come from a transparent, court-tested strategy that removes assets from your personal ownership before creditor claims arise, not from secrecy.

Entity formation (LLCs, corporations) provides some liability separation but is easily penetrated if you personally guarantee loans, own real estate individually, or commingle personal and business funds. Courts have consistently pierced entity structures when they appear to exist primarily for tax avoidance or fraud.

An independent trustee holding title to assets on your behalf creates a structural barrier that courts recognize as legitimate. Unlike an LLC you control, an irrevocable trust transfers legal ownership to a neutral party bound by fiduciary duty and state law, not personal preference.

Question: Why doesn’t an LLC or corporation fully protect my personal assets?

LLCs provide liability separation for business operations but do not protect the LLC itself or its assets from creditors of the owner. If you are personally sued for something unrelated to the business, a judgment creditor can obtain a charging order against your LLC membership interest and force distributions. If you personally guarantee a business loan, the lender becomes a creditor of you, not just the LLC. More critically, personal real estate, investment accounts, and liquid savings held outside the LLC remain fully exposed. Many business owners mistakenly believe entity formation alone solves creditor protection. You need layered strategies that address both business liability and personal asset separation.

Question: Can I use multiple bank accounts or move money to protect it?

Moving assets after a creditor claim or lawsuit has begun is fraudulent transfer, which can void the transaction and expose you to criminal liability. Creditors have strong tools to unwind transfers made within a lookback period, typically two to four years depending on state law. The timing is critical: you must implement asset protection strategies during calm times when no creditor or lawsuit is visible on the horizon. This is why advance planning with a specialized advisor is essential. Our Ultra Trust system is designed to be implemented well before any creditor threat emerges, ensuring the strategy is not viewed as a fraudulent response to an existing claim.

Understanding Irrevocable Trusts as a Legal Shield

An irrevocable trust is a legal entity that holds title to assets and is managed by an independent trustee for the benefit of designated beneficiaries. Once you transfer assets into an irrevocable trust and sign the deed, you no longer own those assets personally. This is the key: creditors sue you, not the trust. The judgment creditor has no claim against property the trust owns because you have no legal interest in it.

The term “irrevocable” means you cannot unwind the trust or reclaim the assets later. This permanence is exactly what makes it creditor-proof. If a trust could be revoked on demand, a court would treat it as still belonging to you and pierce it to satisfy a creditor. The irreversibility, while limiting, is the source of the protection.

Our approach differs from generic trust templates. We design irrevocable trusts specifically for asset protection, meaning the trust document, trustee selection, and asset titling all work together to withstand judicial scrutiny. The trustee must be truly independent, not a spouse, adult child, or business partner, to pass court review. We coordinate multiple assets and entities to create redundancy, so if one layer is challenged, others remain intact.

Question: If I cannot access the trust assets, what is the point of owning them?

The point is that assets in an irrevocable trust are still yours economically, they benefit you and your heirs, but are not yours legally. You can receive distributions from the trustee if the trust permits, and the trustee can be instructed (through the trust document) to use trust funds for your healthcare, housing, and other needs. The trust is not a complete loss of access; it is a loss of personal control and a legal transfer of title. You also retain the ability to name the trustee and control who benefits and when. Many clients also keep assets outside the trust for immediate liquidity and direct access, using the irrevocable trust as a strategic layer for significant holdings. The balance depends on your specific situation, income needs, and goals.

Question: How is an irrevocable trust different from a will or revocable trust?

A revocable trust (also called a living trust) allows you to change beneficiaries, reclaim assets, or dissolve the trust at any time. This flexibility is useful for probate avoidance and privacy, but it offers zero creditor protection because a court views it as still your property. A will is a document that directs asset distribution after death, but it does nothing to protect assets during your lifetime. An irrevocable trust is the only structure that legally removes assets from your ownership and creditor reach while you are living. The drawback is inflexibility; you cannot change it without the trustee’s agreement or a court order. Our guidance focuses on identifying which assets benefit most from irrevocable structure and which should remain in revocable trusts or direct ownership for liquidity and control.

How Our Ultra Trust System Provides Court-Tested Protection

We have designed the Ultra Trust system around documented court outcomes, not theoretical frameworks. Our approach combines several elements: irrevocable trust structure, independent trustee selection, multi-state titling coordination, and integration with other protective entities.

The trustee is critical. We identify and coordinate with an independent trustee, often a corporate fiduciary, trust company, or qualified attorney, who is genuinely separate from you and your family. Courts examine trustee independence closely. If the trustee is your adult child who lives with you and follows your instructions without question, a judge may disregard the trust as a sham. A truly independent trustee has discretion to deny distributions and is governed by a fiduciary duty to the trust and beneficiaries, not to you personally.

Asset titling matters equally. Every deed, account registration, and ownership document must clearly reflect the trust as the owner. Partial titling or sloppy documentation creates vulnerability. We handle the operational complexity so the trust is not just a legal structure on paper but a functioning, integrated part of your wealth management.

Our system also coordinates across multiple trusts and entities rather than relying on a single strategy. This redundancy is what distinguishes court-tested protection from single-layer approaches. If one layer is challenged in litigation, others remain in place.

Question: What makes Ultra Trust different from a standard irrevocable trust?

A standard irrevocable trust, created using a template or drafted by a general practitioner, often lacks the operational rigor and multi-layer coordination that creditors can exploit. Ultra Trust incorporates our proprietary framework for trustee vetting, asset titling coordination, distribution flexibility, and integration with complementary entities. We design each trust with specific court precedents in mind; we review how similar trusts have fared in litigation and build protection accordingly. The difference is comparable to the gap between a generic NDA and one drafted by a litigator who knows how courts actually interpret trust language. Additionally, we provide ongoing trustee coordination and annual reviews to ensure the trust continues to function as intended and that asset titling remains current. A one-time trust document is not enough; the strategy must be managed actively.

Question: Can a creditor challenge my irrevocable trust and force a court to pierce it?

A creditor can file a legal challenge, but the burden is on them to prove either that the trust is a sham (meaning you never actually transferred assets) or that the trust was created fraudulently to avoid a known creditor. If the trust is genuine, assets were properly transferred, the trustee is independent, and the transfer occurred years before any creditor claim, courts across most jurisdictions uphold the trust and deny the creditor access. However, timing matters: if you create the trust the day before a lawsuit is filed, courts view this as suspicious and may undo it as a fraudulent transfer. Our approach includes advance planning with proper documentation and a lookback period that ensures the trust is well established before any creditor emerges. The strength of Ultra Trust lies in this advance positioning combined with proper trustee independence and asset titling.

The Tax Benefits of Structuring Assets Correctly

Asset protection and tax efficiency are not separate goals, they are interdependent. A poorly structured irrevocable trust may shield assets from creditors but create unexpected tax liability or lost deductions. Conversely, a tax-optimized strategy that ignores creditor exposure leaves your wealth vulnerable.

Irrevocable trusts offer several tax advantages when structured correctly. If the trust is a grantor trust for income tax purposes, you pay the income taxes on trust earnings, which allows the trust to accumulate assets tax-free and removes that growth from your taxable estate. This is a sophisticated planning tool: you reduce your estate tax exposure while maintaining indirect access to trust earnings.

For estate tax purposes, assets in an irrevocable trust are removed from your taxable estate, reducing federal estate tax liability. For a high-net-worth individual with substantial appreciating assets, this can save hundreds of thousands in estate taxes.

We also coordinate trust funding with charitable giving, tax-loss harvesting, and income timing strategies. The irrevocable structure gives us flexibility that revocable trusts cannot offer. A grantor-retained annuity trust or a spousal lifetime access trust can achieve additional layers of tax and creditor protection simultaneously.

Question: Will my irrevocable trust increase my income taxes?

Not necessarily, and this is where trust structure matters. If the trust is drafted as a grantor trust, you remain the owner for income tax purposes and pay taxes on trust income at your personal rate. This is often favorable because it prevents the trust from accumulating income at higher trust tax rates (which are steep in 2026). However, some clients prefer non-grantor trust structures for different reasons. The key is that your advisor must understand both creditor law and tax law and align the trust design with both goals. We review your full tax situation and structure the trust accordingly. A poorly designed trust might save you from creditors but cost you in taxes; that is not our approach.

Question: How does irrevocable trust planning affect my IRS exposure?

An irrevocable trust has no special relationship with the IRS unless the trust itself engages in unreported income or the transfer to the trust was fraudulent. If you transfer assets properly and the trust reports income correctly, IRS exposure is typically lower than keeping assets in your personal name. The trust also limits the ability of the IRS to place a lien on all your assets; they can only lien trust assets if the trust itself owes taxes. For high-net-worth individuals who face IRS audit risk, this separation is valuable. However, our irrevocable trust planning approach includes full IRS compliance; we ensure the trust files returns, maintains documentation, and reports all income and distributions correctly. This transparency is what allows courts to recognize the trust as legitimate rather than a tax evasion vehicle.

Multi-Layer Protection: Combining Strategies for Maximum Security

A single asset protection strategy is rarely sufficient for a truly high-net-worth individual. Creditors are sophisticated; they hire aggressive attorneys who will challenge every layer they encounter. Multi-layer protection means that if one strategy is overcome, others remain in place.

Our approach coordinates irrevocable trusts with:

- Titling strategies that separate real estate, investment accounts, and liquid assets across multiple ownership structures

- Entity structures (corporations and LLCs) that segregate business operations and real estate by use and liability profile

- Interstate trust placement, using trusts governed by asset protection-friendly state laws such as Nevada or South Dakota

- Distribution timing strategies that limit liquid assets held in highly exposed accounts at any given time

For example, a business owner might hold the operating business in an LLC, place the business building in a separate LLC held by an irrevocable trust, keep personal residence in another entity, invest liquid capital in a trust-held account, and retain only modest amounts in a personal bank account. A creditor pursuing a judgment against the business owner must navigate multiple entities and trusts, each with different ownership structures and legal barriers. This is dramatically harder and more expensive than pursuing a single target.

The key is intentionality. Haphazard structures create confusion and legal vulnerability. We design the full strategy as an integrated system.

Question: What is the advantage of using multiple entities versus one irrevocable trust?

Multiple entities (LLCs, corporations) separate liability by function and jurisdiction, limiting the damage if one entity is sued. An irrevocable trust removes assets from your personal ownership, which addresses creditor claims against you individually. The combination is powerful: the entity limits operational liability, and the trust shields assets from personal judgments. However, adding more structures increases complexity, compliance burden, and cost. We balance protection against practicality. Some clients benefit from three or four coordinated structures; others are better served by one robust irrevocable trust combined with solid insurance. The strategy is customized to your specific risk profile and assets.

Question: Can a creditor pursue assets across multiple trusts or entities if they are related?

A creditor can attempt to “pierce the veil” and claim that multiple trusts or entities are actually controlled by you and should be treated as one for liability purposes. This is why independence and separation are critical. If you are the trustee of multiple trusts, make distributions between them at will, or treat them as a unified fund, a court may combine them and allow creditor access. Our design includes separate trustees, independent decision-making, and clear separation of funds to prevent veil piercing. We also ensure that each trust or entity serves a legitimate purpose beyond liability avoidance; a court is much less skeptical if the structures have business, tax, or family planning rationales in addition to creditor protection.

Financial Privacy: Keeping Your Wealth Confidential

Asset protection and privacy are related but distinct. Protection prevents creditors from accessing assets legally; privacy prevents them from discovering assets exist in the first place.

Irrevocable trusts provide privacy because the trust is the owner of record. Deeds, account registrations, and investment records show the trust name, not your personal name. A curious creditor or litigant cannot simply search property records or investment disclosures and find the assets. This is not secrecy or tax evasion; it is legal privacy, commonly used by high-profile individuals, business owners, and families who prefer that their assets and net worth remain confidential.

Privacy also reduces your visibility as a litigation target. If you own commercial real estate, investment accounts, and business interests all in your personal name, you become an obvious target for opportunistic litigation. A trustee holding those assets on your behalf is far less visible.

The privacy layer coordinates with the creditor protection layer. A creditor cannot garnish what they cannot find. Combined with proper document maintenance and trustee independence, privacy becomes part of the overall protection strategy.

Question: Is privacy through a trust legal, or is it a form of tax evasion?

Privacy is legal as long as assets are properly titled, income is reported, and the trust is genuine. The IRS does not require you to disclose all your assets publicly, and trusts are standard legal vehicles recognized in all fifty states. The distinction between legal privacy and fraudulent concealment is clear: if you report income correctly, file trust tax returns, and respond truthfully to discovery in litigation, you are using legal privacy. If you hide assets, lie under oath about ownership, or fail to report trust income, you have crossed into fraud. Our approach maintains the legal line carefully. We design trusts for privacy and protection, but we ensure that all reporting and disclosure obligations are met.

Question: How does privacy in a trust affect my personal credit or borrowing?

If you personally guarantee a loan (as most business owners do), your credit profile and net worth disclosure still apply; the lender will require you to pledge personal assets or provide a financial statement. The privacy benefit of a trust applies to the public record and to creditors who do not have contractual rights to your information. For borrowing purposes, you will still need to disclose trust assets if you are serving as trustee or beneficiary with distribution rights. The privacy is selective: it prevents random litigation searches and reduces public visibility without preventing legitimate lenders or creditors (with proper legal authority) from discovering assets. The protection lies in legal structure and firewall, not in hiding assets from everyone.

Common Mistakes That Leave Your Assets Vulnerable

We have reviewed hundreds of irrevocable trusts, and patterns of failure are clear. These mistakes undermine protection even when the trust document appears sound.

Insufficient trustee independence: The most common vulnerability is a trustee who is too close to you. A spouse, adult child, or business partner serving as trustee who routinely takes direction from you erodes the independent status the court requires. A creditor will argue the trustee is your puppet, and courts have agreed in many cases.

Delayed planning: Creating a trust after a lawsuit is filed or while a creditor is known creates a fraudulent transfer risk. Creditors can unwind the transfer, and prosecutors can pursue fraud charges. All protection must be in place before crisis.

Incomplete asset titling: A trust that exists on paper but does not actually own assets is not protection. Every piece of real estate, investment account, and title document must be transferred to the trust. Sloppy titling creates gaps creditors can exploit.

Commingling funds: If you treat the trust account as your personal account, withdrawing and depositing at will, the creditor will argue the trust is just a formality and should be disregarded.

Failure to file trust tax returns: A trust must file a 1041 return and issue K-1s to beneficiaries if applicable. Failure to file creates an IRS problem and weakens the argument that the trust is legitimate.

Question: What happens if I create a trust but do not transfer all my assets into it?

Assets not transferred to the trust remain in your personal name and are fully exposed to creditors. The trust protects only what it owns. Many clients fund the trust at creation and then purchase new assets later; those new assets may be held in personal name by habit or oversight. We conduct asset audits and retitling to ensure the strategy is complete. A partial trust is only partial protection.

Question: Can I serve as my own trustee and still get creditor protection?

If you are the trustee, the trust is likely deemed your own property, and creditors can access it as if you held the assets personally. Courts consistently view grantor-trustees (where you are both the grantor and the trustee) with skepticism for creditor protection purposes. An independent trustee is the standard requirement. Some advanced planning tools like grantor retained annuity trusts can be grantor-trustee trusts for specific purposes, but general asset protection trusts must have independent trustees. This is a fundamental rule in irrevocable trust planning that cannot be bypassed.

Step-by-Step Implementation with Expert Guidance

Asset protection planning is not a DIY endeavor. The tax implications, state law variations, and creditor litigation strategies are too complex for generic templates.

Our process begins with a comprehensive financial and legal audit. We map all your assets, liabilities, and risk exposures. We review your business operations, personal life insurance coverage, and existing trusts or entities. This gives us the full picture needed to design a coordinated strategy.

Next, we identify which assets are most exposed and would benefit most from irrevocable trust protection. Not every asset requires this level of protection; some are adequately insured, and others are low-risk. We prioritize based on creditor exposure and tax efficiency.

We then design the specific trust structure, including trustee selection, distribution provisions, and tax classification. The trustee must be interviewed and must agree to the role. We prepare all documentation and coordinate the transfer of assets into the trust.

The final step is implementation: retitling assets, funding accounts, filing trust tax returns, and establishing ongoing management. This is where many plans fail; the documents are drafted but the assets are never properly transferred. We oversee the full implementation to ensure the strategy actually works.

Question: How long does it take to set up a complete asset protection plan?

Initial consultation to final implementation typically takes three to six months, depending on the complexity of your assets and the number of entities involved. The front-end work is thorough, but the timeline is manageable. Most delays occur when clients take time to decide on trustee selection or when asset transfers require third-party approvals (such as refinancing a mortgaged property into a trust). We coordinate with your other advisors, accountant, financial advisor, and insurance broker, to align the strategy across all areas. The key is to begin early, well before any creditor risk emerges.

Question: What ongoing maintenance is required after the trust is funded?

Annual trustee coordination, tax return filing, and periodic audits of asset titling ensure the trust continues to function as designed. If you acquire new assets or substantial wealth, we review whether those should also be held in trust. We also monitor changes in asset protection law across states and adjust the strategy if needed. This is why we provide step-by-step expert guidance rather than one-time documents. The strategy must be actively managed, not abandoned after creation.

Real Results: How Our Clients Successfully Protected Their Wealth

Our case work demonstrates that advance planning with proper structure produces measurable outcomes. One commercial real estate investor with approximately $12 million in rental properties and liquid investments transferred his portfolio into an irrevocable trust with an independent trustee in early 2023. In 2024, a contractor filed a $2.3 million lawsuit alleging property defects and seeking to attach the investor’s assets. The creditor conducted extensive discovery, including depositions about his financial situation and asset location. The investor, now without personal ownership of the properties, was not personally liable for the judgment. The lawsuit was settled based on insurance coverage alone. Had the assets been in his personal name, the full judgment would have exposed him to significant personal liability.

A second example involves a medical practice owner with two partners. The practice partnership agreement exposed her to unlimited liability for partner malpractice. She transferred substantial personal assets and her residence into an irrevocable trust before a malpractice claim against a co-partner materialized. When the co-partner was sued for a $4.5 million judgment, creditors pursued the partnership assets and attempted to reach the individual partners’ personal assets. Her trust-held assets remained protected because she no longer owned them individually. The partnership and one partner faced significant liability, but she did not.

These outcomes illustrate the power of advance positioning. The trusts worked not because of legal trickery but because the structure was in place, legally sound, and properly funded before any creditor claim arose. Courts recognize legitimate, advance planning; they reject after-the-fact transfers.

Question: Are there any cases where irrevocable trusts have failed to protect assets?

Yes, trusts have been pierced or set aside when they were created fraudulently (with known intent to avoid a specific creditor), when the trustee was not genuinely independent, or when assets were never actually transferred. We have also seen trusts challenged when the grantor continued to exercise substantial control over distributions or investment decisions. The failure rate is low for trusts that meet the core requirements: legitimate independent trustee, actual asset transfer, proper documentation, and no fraudulent intent. The cases that fail typically involved shortcut planning or one of the common mistakes outlined above.

Question: How do I know if my current trust structure is strong enough?

A professional creditor risk analysis should examine your trustee independence, asset titling completeness, trustee discretion and control, applicable state law, and the absence of any fraudulent transfer appearance. If your current trust has a non-independent trustee, incomplete asset titling, or was created recently in response to a known creditor, it has vulnerabilities. We conduct no-cost preliminary reviews to identify gaps and recommend updates.

Getting Started with Your Asset Protection Plan Today

Creditor litigation targeting high-net-worth individuals is not a theoretical risk; it is a practical reality that requires advance planning. The good news is that a court-tested strategy implemented well before any crisis emerges provides genuine, lasting protection.

The first step is to schedule a consultation with our team. We review your current situation, identify your specific creditor exposures, and explain what an irrevocable trust strategy would look like for your circumstances. There is no obligation, and this consultation is designed to give you clear guidance regardless of whether you work with us.

If you decide to move forward, we provide step-by-step expert guidance through asset audit, trust design, trustee coordination, and implementation. Our goal is to ensure your assets are legally protected, your tax situation is optimized, and your strategy is actively managed to adapt as your life and wealth evolve.

The cost of advance planning is far lower than the cost of litigation or judgment recovery. We work with clients to build a sustainable, comprehensive strategy that aligns creditor protection with your broader wealth and family goals. The time to begin is now, while you have the opportunity to plan intentionally rather than react to crisis.

Contact our team to discuss your specific situation and learn how our Ultra Trust system can provide the court-tested protection your wealth deserves.

For further reading: Irrevocable vs Revocable Trusts, Irrevocable trust planning.

Contact us today for a free consultation!